When it comes to saving money on healthcare, two of the most powerful tools are Health Savings Accounts (HSAs) and Flexible Spending Accounts (FSAs). Understanding health insurance HSAs vs FSAs can help you reduce medical costs, save on taxes, and plan smarter for future healthcare expenses.

Although they sound similar, they work very differently—and choosing the right one can significantly impact your financial health.

To explore more insurance structure guides, visit:

Quotemaestro Insurance Guides

[cta_alert id=”3100″]

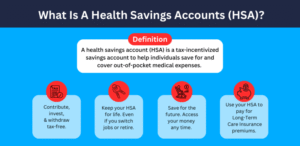

What Is an HSA (Health Savings Account)?

An HSA is a tax-advantaged savings account designed for people with high-deductible health plans.

In health insurance HSAs vs FSAs, HSAs stand out because:

- Contributions are tax-free

- Money grows tax-free

- Withdrawals for medical expenses are tax-free

👉 The biggest advantage: the money rolls over every year and stays with you forever

What Is an FSA (Flexible Spending Account)?

An FSA is also a tax-advantaged account, but it works differently.

In health insurance HSAs vs FSAs, FSAs are typically:

- Funded by your employer

- Used for healthcare expenses

- “Use it or lose it” annually (in most cases)

👉 If you don’t spend the money within the plan year, you may lose it.

Key Differences Between HSAs and FSAs

Understanding health insurance HSAs vs FSAs becomes easier when you compare them directly:

| Feature | HSA | FSA |

|---|---|---|

| Ownership | You own it | Employer controls it |

| Rollover | Yes | Usually no |

| Eligibility | High-deductible plans only | Most employees |

| Contribution limit | Higher | Lower |

| Investment option | Yes | No |

Why HSAs Are So Powerful

One of the biggest advantages in health insurance HSAs vs FSAs is long-term growth.

HSAs allow you to:

- Invest unused funds

- Build tax-free retirement healthcare savings

- Use money anytime for qualified medical expenses

- Keep funds even if you change jobs

This makes HSAs both a healthcare tool and a retirement strategy.

Why FSAs Still Matter

Even though HSAs are more flexible, FSAs still offer value in health insurance HSAs vs FSAs:

- Immediate access to full annual funds

- No need for high-deductible plan

- Good for predictable yearly medical costs

- Helpful for families with regular expenses

Internal Insurance Insight

Understanding employer insurance structure helps clarify account usage.

To learn how plan design affects savings accounts, visit:

First-Year Self-Funded Health Plan Guide

This explains why health insurance HSAs vs FSAs may differ depending on how your employer funds healthcare benefits.

You can also revisit it here:

First-Year Self-Funded Health Plan Guide

Which One Should You Choose?

When comparing health insurance HSAs vs FSAs, your choice depends on your situation:

Choose HSA if:

- You have a high-deductible plan

- You want long-term savings

- You want tax advantages + investment options

Choose FSA if:

- You expect regular medical expenses

- Your employer offers it

- You want immediate access to funds

Common Mistakes People Make

Many people misunderstand health insurance HSAs vs FSAs, leading to lost money:

- Forgetting FSA deadlines

- Not investing HSA funds

- Overestimating yearly medical expenses

- Not tracking contributions

- Missing employer matching benefits

Hidden Advantage Most People Don’t Know

With HSAs in health insurance HSAs vs FSAs, you can:

- Pay old medical bills years later tax-free

- Save receipts and reimburse yourself anytime

- Build a tax-free healthcare retirement fund

This makes HSAs one of the most underrated financial tools available.

[cta_alert id=”3103″]

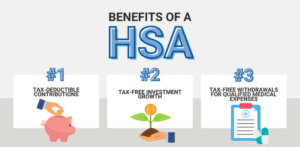

Advanced Insight: Tax Benefits Explained

In health insurance HSAs vs FSAs, tax advantages differ:

HSA Tax Benefits:

- Triple tax advantage

- Tax-free contributions

- Tax-free growth

- Tax-free withdrawals

FSA Tax Benefits:

- Tax-free contributions only

- No investment growth

Real-Life Example

Let’s say you contribute $2,000:

HSA:

- Grows over time

- Can become $10,000+ with investment

- Remains yours forever

FSA:

- Must be used within the year

- Unused funds may be lost

This shows why health insurance HSAs vs FSAs is not just about saving—it’s about strategy.

Internal Resource for Better Understanding

To understand how employer-funded health plans influence savings accounts, read here:

First-Year Self-Funded Health Plan Guide

This helps explain how health insurance HSAs vs FSAs choices are shaped by employer plan design.

FAQs About HSAs vs FSAs

1. Can I have both an HSA and FSA?

Usually no, unless it is a limited-purpose FSA.

2. Which is better for long-term savings?

HSAs are better due to rollover and investment options.

3. Do FSAs expire?

Yes, most FSA funds expire at the end of the year.

4. Can I invest HSA money?

Yes, many HSAs allow investment growth.

5. What happens to my HSA if I change jobs?

It stays with you permanently.

Final Thoughts

Understanding health insurance HSAs vs FSAs is essential for making smarter healthcare financial decisions. While both accounts offer tax savings, HSAs provide long-term flexibility and growth, while FSAs offer short-term convenience.

Choosing the right one depends on your health needs, financial goals, and insurance plan structure.

For more insurance insights, visit:

Quotemaestro Insurance Guides

And explore employer plan structures here:

First-Year Self-Funded Health Plan Guide

First-Year Self-Funded Health Plan Guide

[cta_alert id=”3105″]