Understanding health insurance becomes much easier when you clearly understand one of the most important comparisons: premiums vs deductibles.

These two terms determine how much you pay every month and how much you pay when you actually need medical care. Many people focus only on monthly premiums, but deductibles often have a bigger impact on total yearly healthcare spending.

In this guide, we’ll break down premiums vs deductibles, how they work together, and how to choose the right balance for your health and budget in 2026.

[cta_alert id=”3100″]

What Are Health Insurance Premiums?

To understand premiums vs deductibles, we first need to understand premiums.

A premium is the fixed monthly amount you pay to keep your health insurance active.

Key points:

- Paid every month

- Required even if you don’t use healthcare

- Keeps your insurance active

- Varies based on plan type

Think of premiums as a subscription fee for medical coverage.

What Is a Deductible?

A deductible is the amount you must pay before your insurance starts sharing healthcare costs.

This is a core part of understanding premiums vs deductibles.

Example:

- Deductible = $2,500

- You pay the first $2,500 of covered services

- After that, insurance starts sharing costs

Not all services require a deductible first, especially preventive care.

How Premiums vs Deductibles Work Together

The relationship between premiums vs deductibles is a trade-off.

Low Premium Plans:

- Higher deductibles

- Lower monthly payments

- Higher cost when you need care

High Premium Plans:

- Lower deductibles

- Higher monthly payments

- Lower costs during medical visits

Choosing the right balance depends on how often you use healthcare.

Why This Balance Matters

Many people choose plans based only on premiums, but that can lead to higher costs later.

Understanding premiums vs deductibles helps you realize:

- Cheap monthly plans can cost more during illness

- Higher premiums may save money if you need frequent care

Your health situation plays a major role in decision-making.

What Is an Out-of-Pocket Maximum?

Another important concept linked to premiums vs deductibles is the out-of-pocket maximum.

This is the most you will pay in a year for covered healthcare services.

After reaching it:

- Insurance pays 100% of covered costs

This protects you from extremely high medical bills.

Copays vs Deductibles

These terms are often confused.

Copay:

- Fixed fee per visit (e.g., $30 doctor visit)

- Paid even before deductible in many plans

Deductible:

- Total amount you must pay before insurance shares costs

Understanding both is important when comparing premiums vs deductibles.

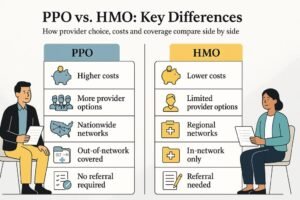

When PPO Plans Matter Most

People with ongoing medical conditions often need more frequent care, making plan selection very important.

If you want to understand how PPO plans help with long-term care, read more here: PPO for Chronic Conditions.

This is especially useful when evaluating premiums vs deductibles for chronic healthcare needs.

Choosing the Right Plan Type

Here’s a simple way to decide based on premiums vs deductibles:

Choose Low Deductible Plans If:

- You visit doctors often

- You take regular medication

- You have ongoing health conditions

Choose High Deductible Plans If:

- You are generally healthy

- You want lower monthly premiums

- You rarely use medical care

[cta_alert id=”3103″]

Why PPO Plans Help with Cost Stability

PPO plans are popular because they balance flexibility and predictable care access.

When analyzing premiums vs deductibles, PPO plans often offer:

- Wider provider access

- Easier specialist visits

- Moderate cost balance

If you have ongoing health needs, PPO coverage can help reduce long-term financial stress.

Learn more here: PPO for Chronic Conditions.

Real Cost Impact of Deductibles

A key insight in premiums vs deductibles is understanding real-world spending.

Example:

- Low premium plan → high deductible → higher upfront costs

- High premium plan → low deductible → more predictable expenses

Total yearly cost matters more than monthly payment alone.

Preventive Care Is Usually Covered

Most insurance plans include preventive services like:

- Annual checkups

- Vaccinations

- Screenings

These are often covered before meeting your deductible, helping reduce long-term costs.

Why PPO Plans Are Preferred for Ongoing Care

For chronic conditions, PPO plans are often preferred because they:

- Allow specialist access without referrals

- Provide broader provider networks

- Reduce treatment delays

This makes them an important factor when evaluating premiums vs deductibles.

Read more here: PPO for Chronic Conditions.

Avoiding Cost Surprises

To avoid unexpected expenses, always check:

- Monthly premium amount

- Deductible size

- Copay rules

- Out-of-pocket maximum

- Network coverage

These factors help you fully understand premiums vs deductibles before choosing a plan.

Final Thoughts

Understanding premiums vs deductibles is one of the most important steps in choosing the right health insurance plan.

Premiums affect your monthly budget, while deductibles determine how much you pay when you need care.

The best choice depends on your health needs, financial situation, and how often you use medical services.

A well-balanced plan helps you avoid surprises and manage healthcare costs more effectively in 2026.

For more healthcare insights, visit PPO for Chronic Conditions or explore resources at Quote Maestro.

[cta_alert id=”3105″]

FAQs About Premiums vs Deductibles

What are premiums in health insurance?

Premiums are monthly payments you make to keep your insurance active.

What is a deductible?

A deductible is the amount you pay before insurance starts sharing costs.

Which is better: high premium or low premium plan?

It depends on how often you use healthcare services.

Do all medical services require deductible payment?

No, preventive care is often covered before the deductible is met.

Why are PPO plans important?

They offer flexibility, better specialist access, and wider provider networks.

What is the most important factor when choosing a plan?

Total yearly healthcare cost, not just monthly premiums.