Mortgage protection life insurance is designed to help your household keep the home if you die while a mortgage is still in place.

It is a life insurance purpose built around a loan balance, with benefits and limits that differ from many traditional policies.

What Mortgage Protection Life Insurance Is?

Mortgage protection life insurance is coverage that pays a death benefit intended to reduce or pay off a mortgage. The goal is to prevent the surviving borrower, spouse, or family from facing unaffordable payments.

Some policies pay directly to the lender, while others pay the beneficiary who then pays the mortgage. The structure depends on the carrier and the product type.

What It Covers?

At its core, it covers the risk of death during the mortgage term. When the insured person dies, the policy pays a benefit that can match the remaining principal, a fixed amount, or a declining amount.

Coverage is often limited to the mortgage amount and may be tied to a specific property loan. Many plans are simple to buy, but simplicity can come with tradeoffs in flexibility.

- Mortgage Payoff Or Reduction. The benefit can be used to pay down the loan balance so the monthly payment becomes manageable or disappears.

- Payment Continuity. If the benefit is paid to a beneficiary, funds may also support temporary housing costs, escrow shortages, or other home related bills.

- Peace Of Mind For Co Borrowers. It can protect a spouse or partner who could qualify for the mortgage but struggle on one income.

Those core protections help clarify whether the product fits your goals or whether a broader policy makes more sense.

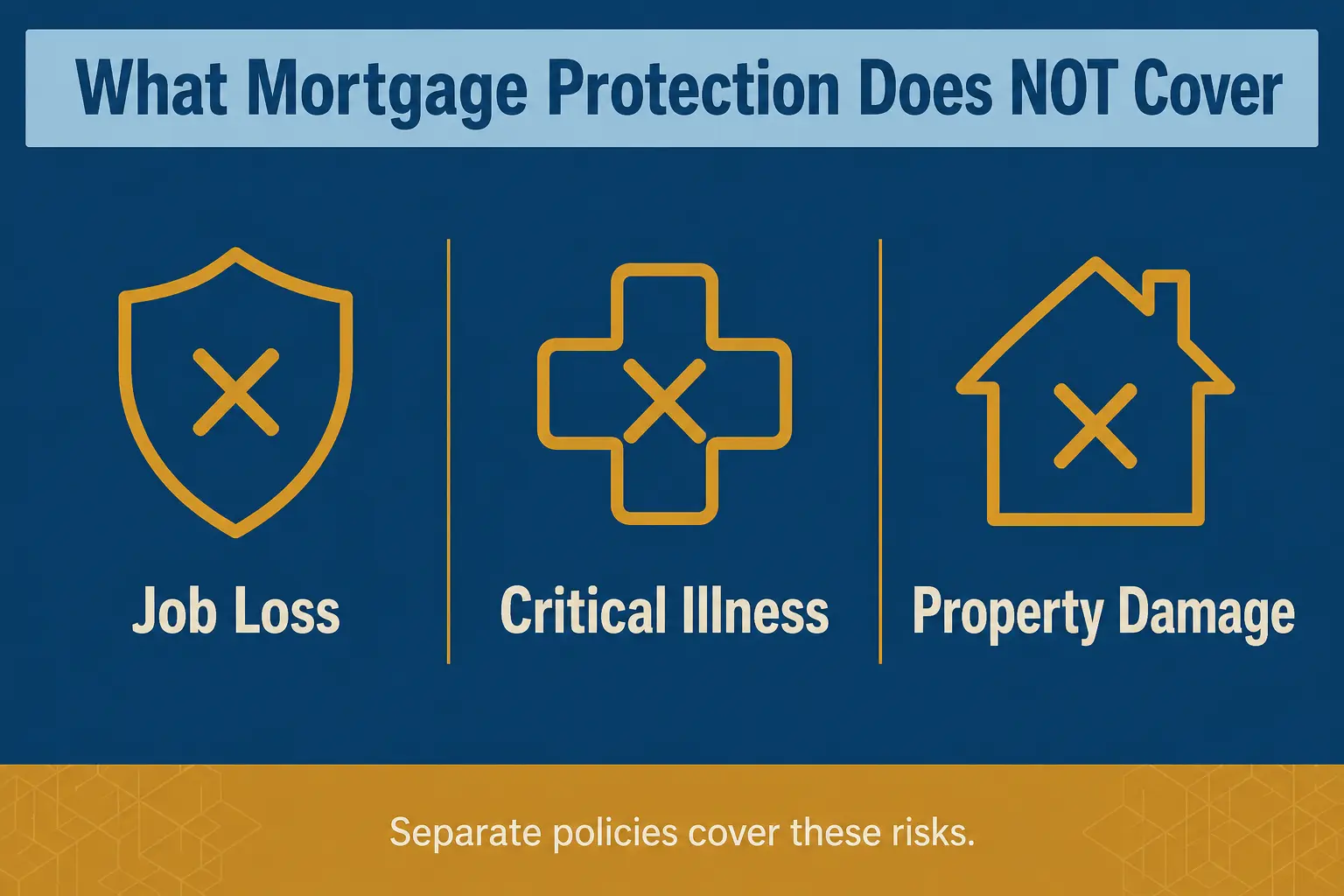

What It Usually Does Not Cover?

Mortgage protection life insurance does not typically cover job loss, routine payment hardship, or home value declines. It is not a replacement for emergency savings, disability insurance, or homeowners insurance.

It also does not guarantee approval for everyone, even when underwriting is simplified. Health history, age and maximum benefit limits can still apply.

- Disability Or Injury. Unless you add a rider that addresses disability, a death only policy will not pay when you cannot work.

- Critical Illness Costs. Hospital bills and long term care expenses are not the core purpose of mortgage protection life insurance.

- Property Damage. Fire, storms, theft and liability are handled by homeowners insurance, not life insurance.

Knowing the boundaries keeps expectations realistic and prevents overreliance on one policy.

How Benefits Are Paid?

Benefits can be structured as level or declining coverage. A level benefit stays the same, while a declining benefit typically falls over time as the mortgage balance is expected to fall.

Payment direction also matters. A lender paid benefit can be convenient, while a beneficiary paid benefit offers more control over whether to pay off, refinance, or keep cash reserves.

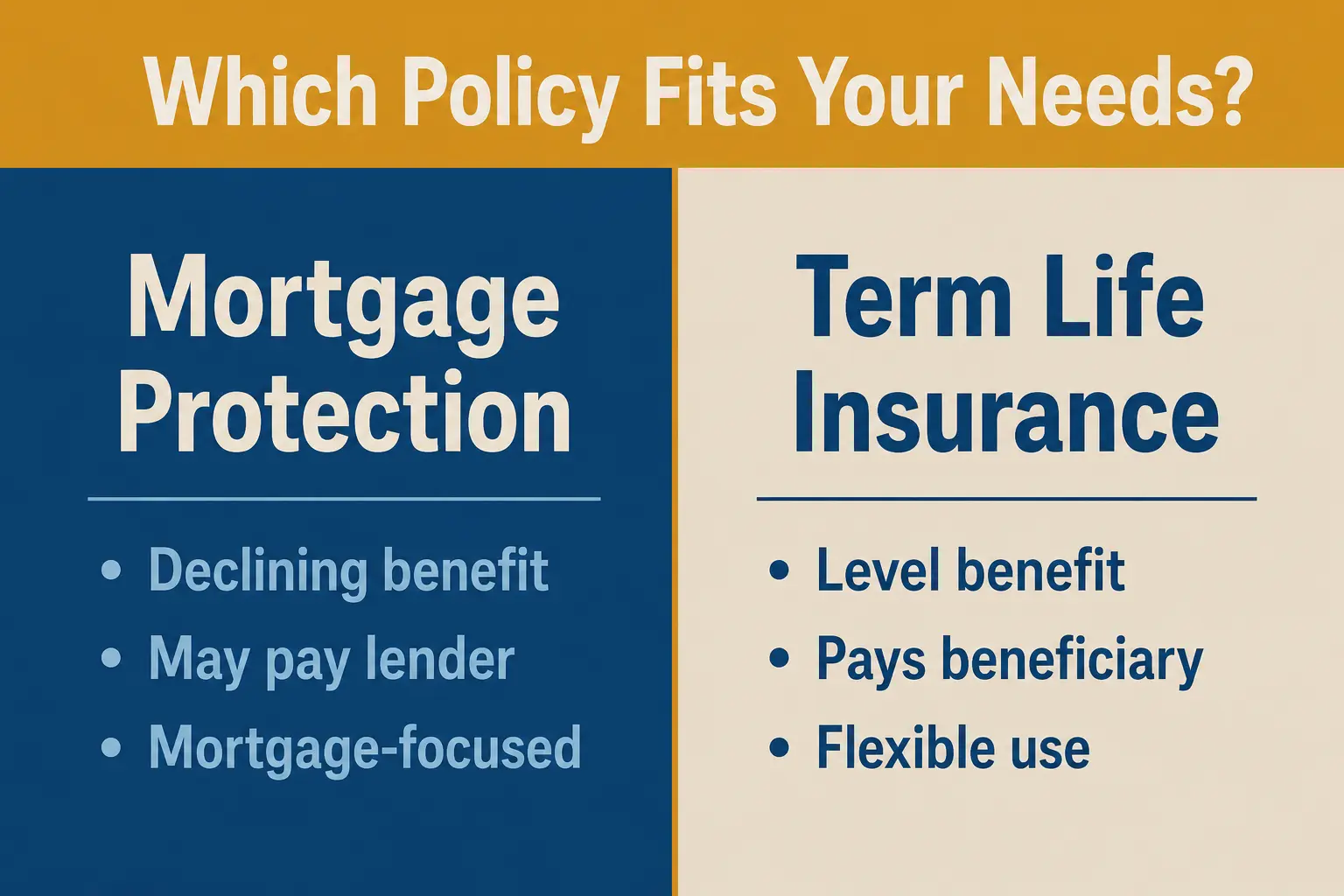

Mortgage Protection Compared With Term Life Insurance

Many households compare mortgage protection life insurance to term life because both can provide large coverage for a set period. The right choice depends on flexibility, pricing and how broadly you want to protect income.

Term life can be set to cover the mortgage and other needs, while mortgage protection can be more narrowly tailored to the home loan. Underwriting, costs and payout options vary by carrier.

| Feature | Mortgage Protection Life Insurance | Term Life Insurance |

|---|---|---|

| Benefit Pattern | Often declining or tied to mortgage | Usually level for the term |

| Who Gets Paid | May pay lender or beneficiary | Typically pays beneficiary |

| Flexibility Of Use | Primarily intended for mortgage | Can cover mortgage, income, or other needs |

| Underwriting | Often simplified but not guaranteed | Can be fully underwritten or simplified |

This comparison makes it easier to decide whether a mortgage focused product is enough or whether broader income protection is needed.

Who Needs Mortgage Protection Life Insurance?

Mortgage protection life insurance can be a good fit when a home is a top priority and a death would create an immediate affordability problem. It is also useful when coverage needs are straightforward and you want a policy aligned with the loan timeline.

It can be especially relevant when one person pays most of the mortgage or when a co borrower depends on that income. The more your budget relies on a single paycheck, the more valuable a dedicated plan may feel.

- New Homeowners With Limited Savings. When reserves are thin, a death benefit can prevent forced sale during a stressful time.

- Single Income Households. If one income supports the payment, protection can help keep the mortgage current.

- Co Borrowers With Uneven Earnings. A benefit can reduce the balance so the remaining borrower can refinance or keep payments affordable.

- Borrowers With Shorter Term Goals. If the priority is to protect the home until the loan balance is smaller, a declining benefit may align well.

These profiles highlight when the policy matches a specific risk, not when it is simply available.

When It May Not Be The Best Fit?

It may be less appealing if you want coverage that stays level and can support multiple goals such as income replacement, child care, or education costs. It can also be less efficient when the premium is high relative to the benefit and alternatives are available.

If your household already has adequate term life coverage that fully protects the mortgage and living costs, adding a mortgage specific policy can be redundant. If you plan to move soon, a lender tied policy can also be restrictive.

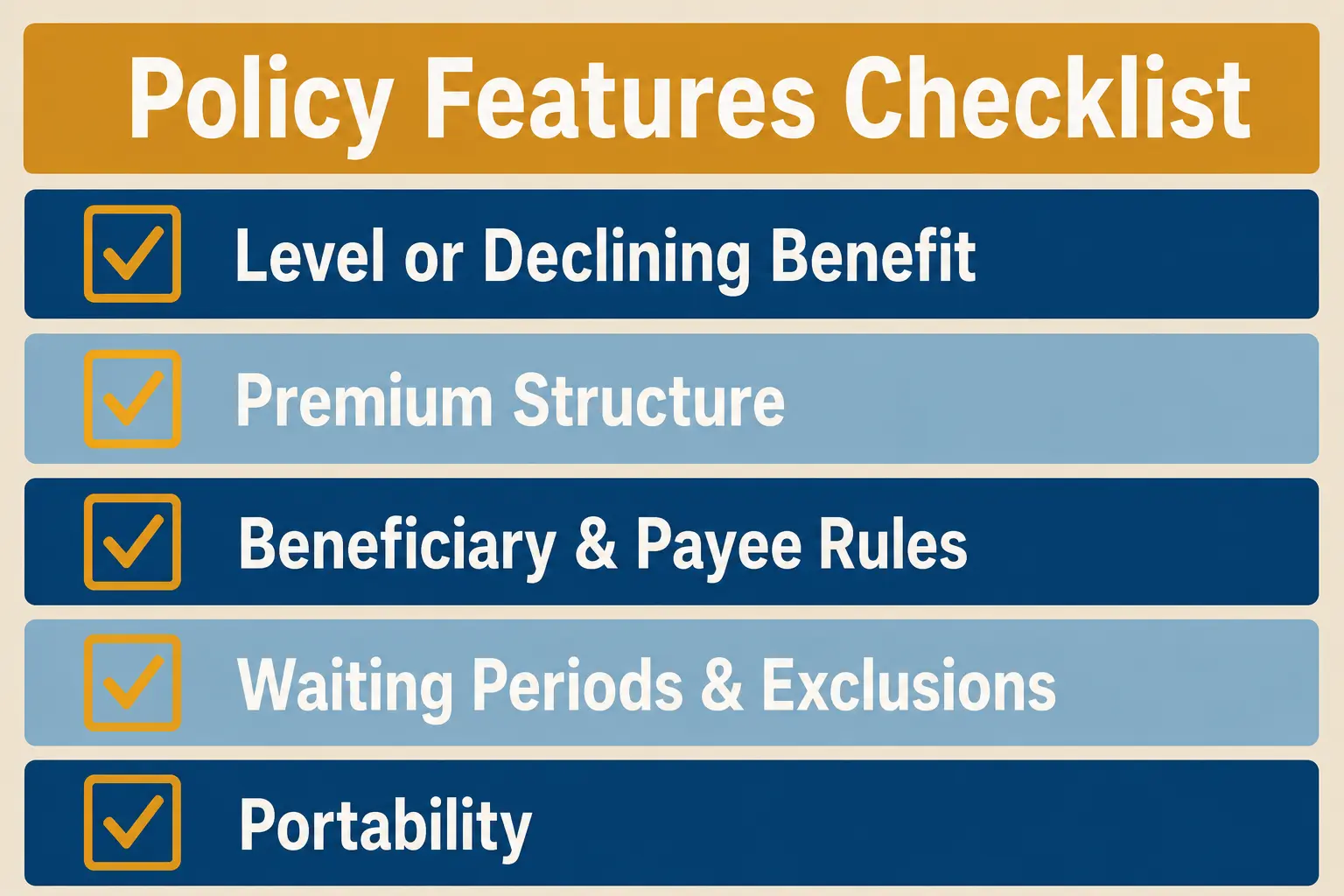

Key Policy Features To Review Before Buying

Mortgage protection life insurance varies widely by insurer, so reading the policy details matters. A quick application can be convenient, but you still want clarity on benefit type, exclusions and what happens if your mortgage changes.

Ask for the full outline of coverage and confirm which mortgage is being protected. Pay attention to how the benefit reduces over time and whether premiums stay level.

- Level Or Declining Benefit. Confirm whether the death benefit stays constant or decreases and how the schedule is calculated.

- Premium Structure. Check whether premiums are level, increase by age bands, or can change after an initial period.

- Beneficiary And Payee Rules. Verify if the lender is the beneficiary, whether you can change it and how funds are disbursed.

- Waiting Periods And Exclusions. Look for contestability provisions, suicide clauses and any graded benefit period for simplified plans.

- Portability. Confirm what happens if you refinance, move, or pay off the mortgage early.

These checkpoints help you compare policies on substance, not just on the monthly price.

How To Choose The Right Coverage Amount and Term?

Start with the mortgage balance you want protected and the time horizon you care about most. Many borrowers choose a term that matches the loan length or the years until the payment becomes comfortable on one income.

Then decide whether you want to protect only the loan or also create a buffer for taxes, insurance and household expenses. A small cushion can reduce pressure to sell quickly even if the mortgage is paid down.

- Confirm The Mortgage Details. Note the current principal balance, interest rate and remaining years so coverage matches real obligations.

- Decide Your Protection Goal. Choose whether you want a full payoff, a partial payoff, or a fixed cash amount that makes refinancing feasible.

- Select Level Or Declining Coverage. Use level coverage for stable protection and declining coverage when the goal is to mirror a shrinking balance.

- Align The Term With Your Timeline. Match the policy term to the years you need the protection, not necessarily the full mortgage length.

- Stress Test The Budget. Ensure the premium fits alongside savings and other insurance so the policy stays in force.

Once those choices are made, comparing quotes becomes simpler and less emotional.

How It Works With Other Insurance?

Mortgage protection life insurance is most effective when it complements a broader safety net. Term life, disability coverage and emergency savings each cover different risks that can threaten homeownership.

Homeowners insurance protects the property, while life insurance protects the people who pay for it. Coordinating limits and beneficiaries reduces gaps and avoids duplicated premiums.

Conclusion

Mortgage protection life insurance can be a practical way to keep a home secure when a death would make the mortgage unmanageable. The main value is its focus on protecting the loan, especially for households with limited savings or uneven income.

Before buying, confirm how the benefit is calculated, who receives the payout and whether the coverage stays useful if you refinance or move. A policy that matches your mortgage plan and overall budget can provide clear, targeted peace of mind.

FAQ’s

1: Can you buy mortgage protection life insurance after getting a mortgage?

Yes. In many cases, you can buy mortgage protection life insurance after your mortgage has already been approved. Eligibility depends on factors such as your age, health and the insurer’s underwriting requirements. Buying coverage sooner may provide more options and potentially lower premiums than waiting until later.

2: Does mortgage protection life insurance end when the mortgage is paid off?

Generally, yes. Mortgage protection life insurance is designed to protect a specific home loan, so coverage typically ends once the mortgage is fully repaid or when the policy term expires. If you refinance or move to a new home, review your policy to understand whether the coverage can continue or needs to be replaced.

3: Is mortgage protection life insurance worth it for first-time homebuyers?

It can be worthwhile for first-time homebuyers who have limited savings or rely on one income to make mortgage payments. The policy can help protect loved ones from the financial burden of the remaining loan balance. However, comparing it with term life insurance is important to determine which option better fits your overall financial goals.