Life insurance pricing changes as you get older, but age is only one piece of the premium. Insurers price risk using health, lifestyle, coverage amount and how long the policy is meant to last.

This guide breaks down how life insurance cost by age typically works, what factors matter most at each stage and how to shop without overpaying. The goal is to help you choose coverage that fits your budget and your responsibilities.

How Age Affects Life Insurance Premiums?

Age is strongly tied to mortality risk, so premiums generally rise over time. Insurers usually set rates by age band and a birthday can move you into a higher-priced bracket.

Buying earlier often lowers the base rate and can let you lock in pricing for a long term. Waiting can still make sense if you have temporary needs or are improving health, but it usually increases cost.

What Insurers Look at Besides Age?

Age sets the starting point, then underwriting adjusts it. Underwriting is the process insurers use to estimate risk and place you in a rate class.

Common pricing inputs include medical history, family history, tobacco use, build and medications. Occupation, driving record and risky hobbies can also matter, depending on the carrier.

- Health profile: Blood pressure, cholesterol, A1C and past diagnoses often affect rate class more than people expect.

- Tobacco and nicotine: Cigarettes, vaping and nicotine replacement can trigger higher premiums until you qualify as nicotine-free.

- Build and labs: Height and weight ranges and lab results can shift you between preferred and standard pricing.

- Prescription history: What you take and how often can influence both eligibility and pricing.

- Risk exposure: Aviation, climbing, or hazardous jobs may add surcharges or exclusions.

Once you understand these levers, it becomes easier to see why two people the same age can receive very different quotes.

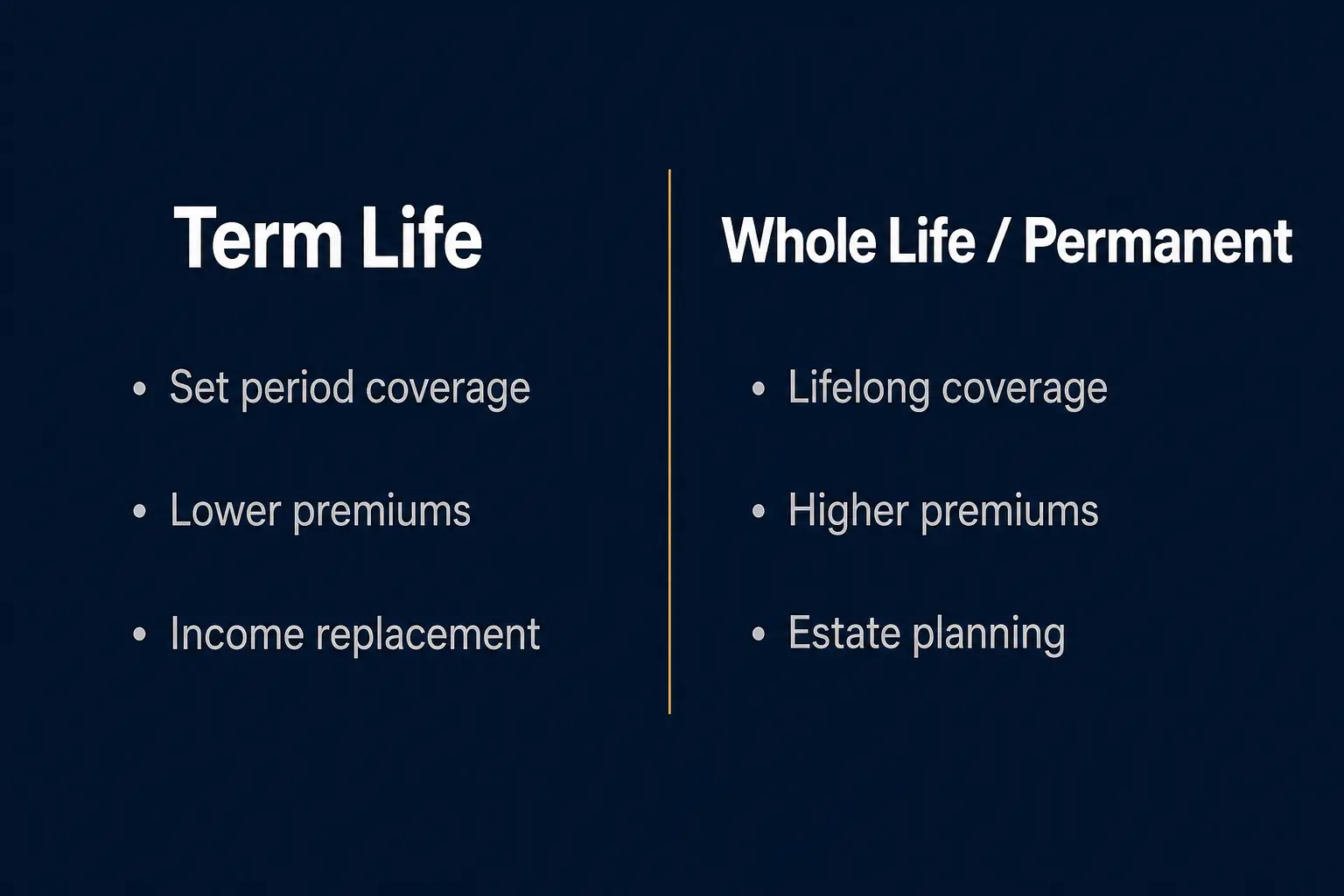

Term Life Versus Whole Life Costs by Age

Term life insurance typically has the lowest starting premium because it covers a set period. Whole life and other permanent policies cost more because they can last for life and include cash value features.

Life insurance cost by age tends to climb faster for permanent coverage since premiums reflect long-term guarantees and reserves. Term pricing still rises with age, but the increase is often easier to manage for many households.

When Term Life is Often a Better Fit?

Term is usually built for income replacement and debts with an end date. Many people align term length with the years that others depend on their income.

- Family protection: Replacing income during child-raising years.

- Mortgage payoff: Matching coverage to the remaining loan period.

- Business needs: Covering a key person or a buy-sell obligation for a defined window.

These uses keep the plan focused on protection while avoiding the higher price of lifetime coverage.

When Permanent Insurance Can Make Sense?

Permanent insurance is often chosen for long-lasting needs that do not expire. It can also be used for estate planning or funding final expenses, depending on goals and affordability.

- Lifelong dependents: Long-term care for a child or adult with special needs.

- Estate liquidity: Providing cash to cover taxes or equalize inheritance.

- Legacy planning: Leaving a guaranteed benefit to heirs or a charity.

Because premiums are higher, the best fit usually depends on stable cash flow and long-term intent.

Typical Life Insurance Cost by Age Ranges

Exact premiums vary by insurer and underwriting result, so the most accurate view comes from personalized quotes. Still, broad ranges can help you set expectations before you apply.

The table below shows how costs generally trend as age increases, along with common planning priorities. It is directional guidance rather than a price quote.

| Age Range | Typical Premium Direction | Common Coverage Focus |

|---|---|---|

| 20 to 29 | Lowest starting premiums for most applicants | Lock in long term rates and cover early debts |

| 30 to 39 | Moderate increase as responsibilities grow | Income replacement and mortgage protection |

| 40 to 49 | Noticeable jump, underwriting matters more | Family security and college years planning |

| 50 to 59 | Steeper increase, health factors weigh heavily | Retirement timing and shorter term planning |

If you are comparing multiple carriers, look for the same coverage amount, term length and rate class assumptions. That is the only way to compare life insurance cost by age fairly.

Rate Classes and Medical Exams

Insurers often group applicants into rate classes such as preferred, standard and substandard. The difference between classes can be significant, especially as age increases.

Many policies still require a medical exam, but no-exam underwriting has expanded. No-exam options can be convenient, yet the best price may still come from a fully underwritten policy, especially for healthier applicants.

What a Medical Exam Usually Includes?

The exam is typically quick and done at home or a clinic. It often includes basic measurements and a short health questionnaire.

- Vitals: Blood pressure, pulse, height and weight.

- Labs: Blood and urine for markers related to heart health, diabetes and kidney function.

- History review: Medications, past procedures and follow-up care.

Preparing with good hydration, sleep and a calm schedule can help avoid abnormal readings that trigger extra review.

How Coverage Amount and Term Length Change Cost?

Premiums rise as the death benefit increases, but not always in a straight line. Some carriers price certain face amounts more competitively due to internal tiers.

Term length also matters. Longer terms often cost more because the insurer is guaranteeing the rate for more years, including higher-risk years later in the term.

Choosing a Coverage Amount That Fits

A solid target usually balances income replacement, debts and savings. It also accounts for what survivors would need to maintain housing, childcare and everyday expenses.

- Income needs: Years of income to replace, after considering existing assets.

- Debt cleanup: Mortgage, personal loans and other obligations.

- Future goals: Education funding and major life milestones.

- Final costs: Funeral and end-of-life expenses.

Getting the amount right keeps premiums efficient and reduces the risk of buying too little protection.

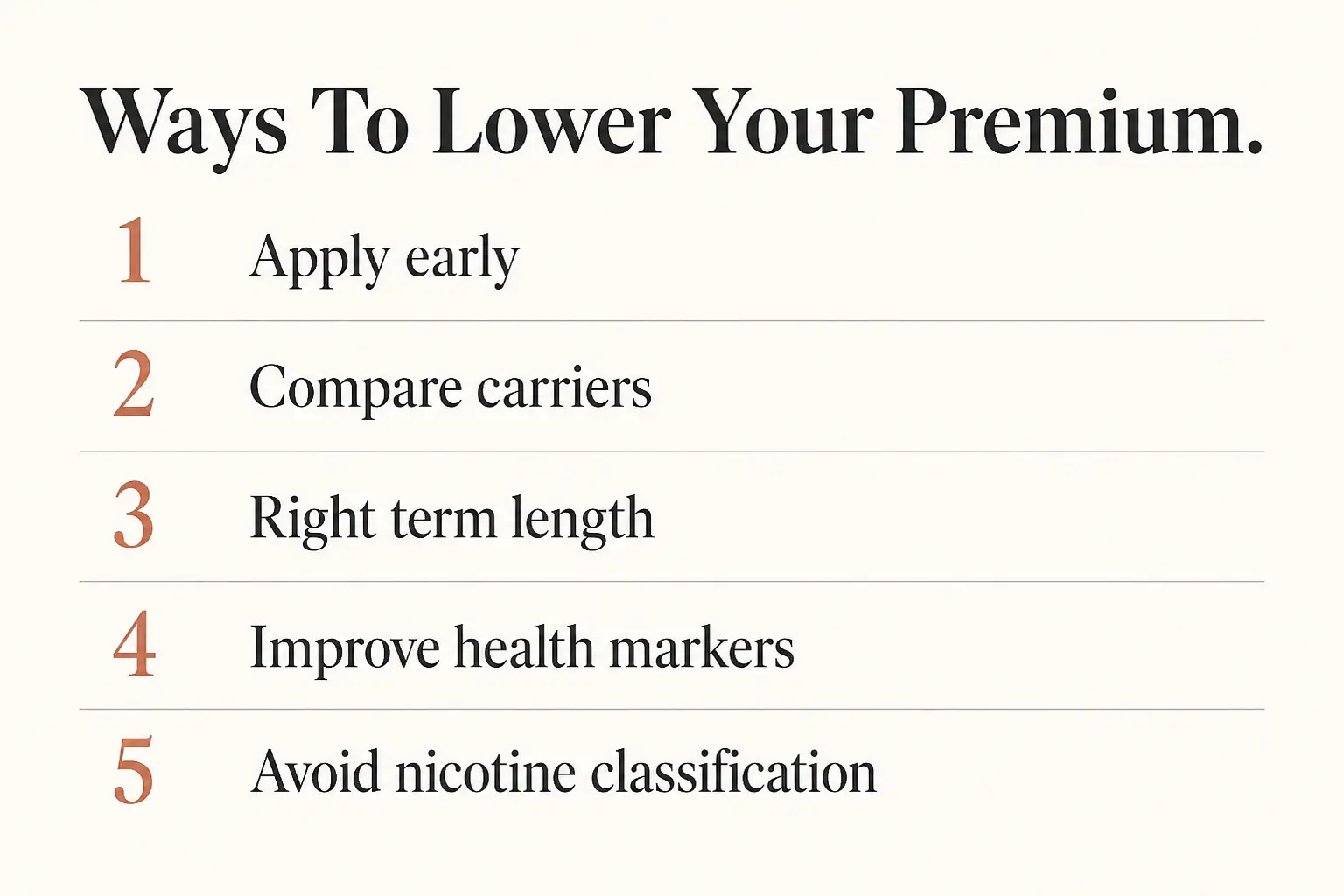

Ways to Lower Your Premium at Any Age

Even though life insurance cost by age trends upward, you can still improve pricing and reduce the chance of overpaying. Most savings come from aligning the policy to the real need and presenting a clean underwriting profile.

- Apply before your next age band. Submitting an application earlier can help you lock a lower age rating with many insurers.

- Compare multiple carriers. Different underwriting guides treat the same health history differently, which can change rate class.

- Choose the right term length. Match the term to the time your dependents or debts need protection rather than defaulting to the longest option.

- Improve controllable health markers. Better blood pressure, weight management and stable labs can move you into a stronger rate class over time.

- Avoid nicotine classification issues. Confirm how the insurer defines nicotine use and when you qualify as non-nicotine.

After you narrow choices, ask for an illustration of the premium schedule and confirm what is guaranteed versus non-guaranteed.

Common Mistakes When Comparing Quotes

Quotes are easy to misread because small differences in assumptions change the price. A low number is not helpful if it reflects a different term, different benefit, or an optimistic rate class.

- Mismatched product types: Term and whole life premiums are not comparable without understanding guarantees and features.

- Different underwriting assumptions: A quote based on preferred health can be misleading if your history points to standard.

- Overlooking riders: Waiver of premium, child riders and accelerated benefit riders can affect cost and value.

- Ignoring conversion options: Term policies may allow conversion to permanent coverage, which can be valuable later.

Reading the policy details and not just the monthly premium leads to better decisions and fewer surprises.

Conclusion

Life insurance cost by age generally increases as you get older, with the sharpest jumps often tied to health and the type of policy you choose. Term life usually offers the lowest cost for income protection, while permanent coverage can serve long-term planning needs at a higher price.

To keep premiums manageable, apply before your next age band when possible, compare carriers and match coverage length to real obligations. A well-matched policy can protect your family or business without stretching your budget.