Cash value life insurance is permanent life insurance that includes a savings-like component called cash value. Alongside the death benefit, part of your premium can build an internal account that grows over time under the rules of the policy.

This type of coverage is designed to last for your lifetime as long as required premiums are paid. It can support long-term planning, but it also comes with higher costs and more moving parts than term life insurance.

How Cash Value Life Insurance Works?

When you pay premiums, the insurer allocates them to policy charges, the cost of insurance and the cash value. Over time, the cash value may grow based on a fixed interest rate, dividends, or market-linked credits, depending on policy type.

The cash value is not the same as a bank account. It is an internal value that grows within the contract and is affected by fees, interest crediting rules and how long the policy has been in force.

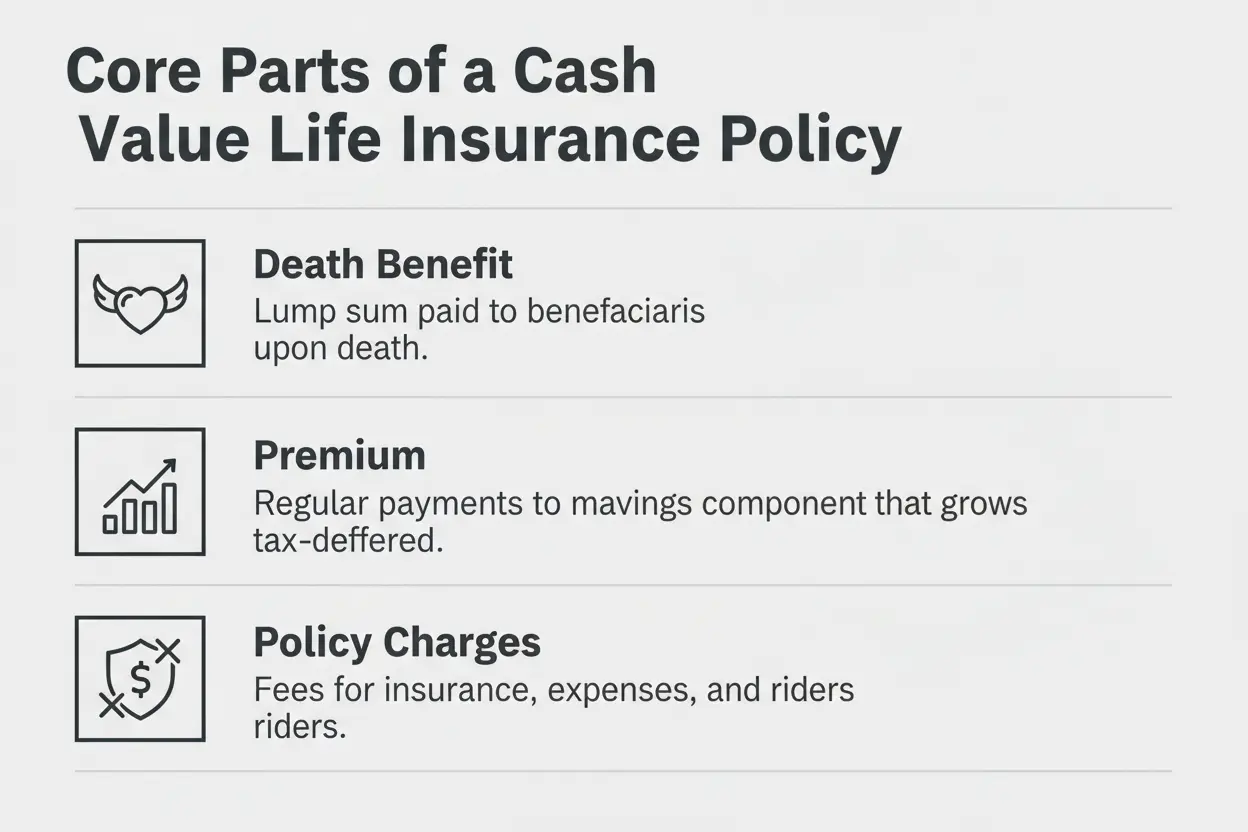

Core Parts of The Policy

Most cash value life insurance policies share a similar structure even when the details vary by carrier. Understanding these parts makes it easier to compare illustrations and avoid surprises later.

- Death benefit. The amount paid to beneficiaries when the insured dies, assuming the policy is in force.

- Premium. The money paid into the policy, either on a set schedule or with flexible funding depending on the design.

- Cash value. The internal accumulation that can grow and may be accessible through loans or withdrawals.

- Policy charges. Costs that can include administrative fees, the cost of insurance and optional rider charges.

Those components interact over decades, so early-year results often look different from long-term results.

Types of Cash Value Life Insurance

Cash value life insurance comes in several forms. The best fit depends on risk tolerance, budget and how much flexibility you want in premiums and death benefit options.

Each type has its own method for building cash value, as well as different guarantees and tradeoffs.

Whole Life Insurance

Whole life insurance generally offers level premiums and guarantees for cash value growth and death benefit as long as policy terms are met. Some whole life policies also pay dividends, which can increase cash value or purchase paid-up additions.

Because guarantees and reserves are built in, whole life tends to be less flexible but more predictable.

Universal Life Insurance

Universal life insurance typically provides flexible premiums and an adjustable death benefit within limits. Cash value can earn interest at a rate set by the insurer, often with a minimum guaranteed rate.

Flexibility can be helpful, but it also means performance depends on interest crediting and ongoing costs. If funding is too low, the policy can lapse.

Indexed Universal Life Insurance

Indexed universal life insurance credits interest based on an external index, using rules such as caps, participation rates and spreads. It usually has a floor that limits negative credits, though policy charges still apply.

Returns can vary widely because index crediting is not the same as owning the index. Reviewing the crediting method and historical cap changes can help set realistic expectations.

Variable Life Insurance

Variable life insurance allows cash value to be invested in subaccounts similar to mutual fund options. Growth potential can be higher, but so is downside risk and cash value can decline with market performance.

Because of investment risk and complexity, variable policies often require careful monitoring and comfort with volatility.

Cash Value Growth and What Affects It?

Cash value growth depends on premium level, policy charges, crediting method and time. Early in the policy, cash value typically grows slowly because initial expenses and insurance costs are front loaded.

Later, growth may accelerate as the internal account becomes larger and the policy has had time to compound.

Costs That Reduce Cash Value

Even strong crediting years can be offset by charges. A policy illustration can show projected values, but it is also important to understand what must happen for those values to materialize.

- Cost of insurance charges. Ongoing charges tied to age, underwriting class and policy design.

- Administrative fees. Monthly or annual charges for policy maintenance.

- Rider costs. Fees for optional benefits such as chronic illness, waiver of premium, or additional purchase options.

- Surrender charges. Charges applied if you cancel the policy early, often lasting many years.

Knowing which charges are fixed and which can change over time helps you evaluate long-term sustainability.

How You Can Access Cash Value?

Cash value life insurance can offer liquidity, but access rules matter. Withdrawals and loans can reduce the death benefit and cash value and they can trigger taxes if handled incorrectly.

Before taking money out, confirm how the insurer treats loans and withdrawals and verify whether the policy is at risk of lapsing.

Policy Loans

A policy loan uses the cash value as collateral and generally does not require credit checks. Interest accrues and if the loan balance grows too large, it can erode the policy and potentially cause a lapse.

If a policy lapses with an outstanding loan, the taxable amount can be significant. That risk is often overlooked when loans are taken repeatedly over many years.

Withdrawals And Partial Surrenders

Withdrawals remove cash value directly and may reduce the death benefit. Depending on the policy and tax rules, amounts above your cost basis may be taxable.

Some policies treat withdrawals differently than loans, so review the contract provisions and confirm the impact on long-term performance.

Tax Treatment And Key Rules

Cash value growth is generally tax deferred while it remains inside the policy. Death benefits are generally paid income tax free to beneficiaries, though estate tax can still apply in certain ownership structures.

Tax outcomes depend on how the policy is funded and accessed. Overfunding can create a modified endowment contract, which changes the tax treatment of loans and withdrawals.

Modified Endowment Contract Considerations

A modified endowment contract, often called a MEC, is triggered when premiums paid exceed limits under tax rules. Once a policy becomes a MEC, loans and withdrawals are typically taxed differently and may be subject to additional penalties depending on age.

For those funding aggressively, MEC testing should be monitored from the beginning so the policy design matches the intended use.

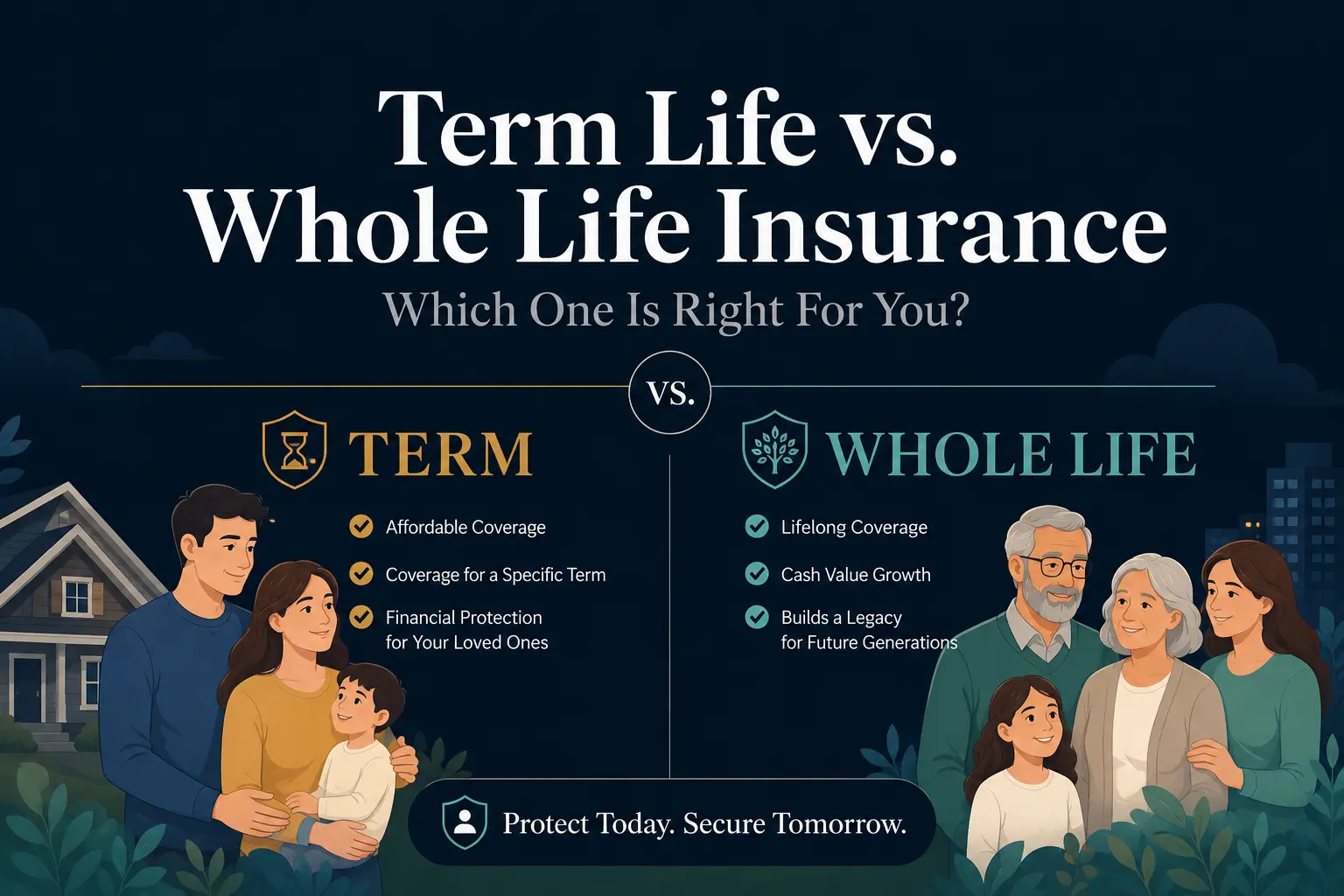

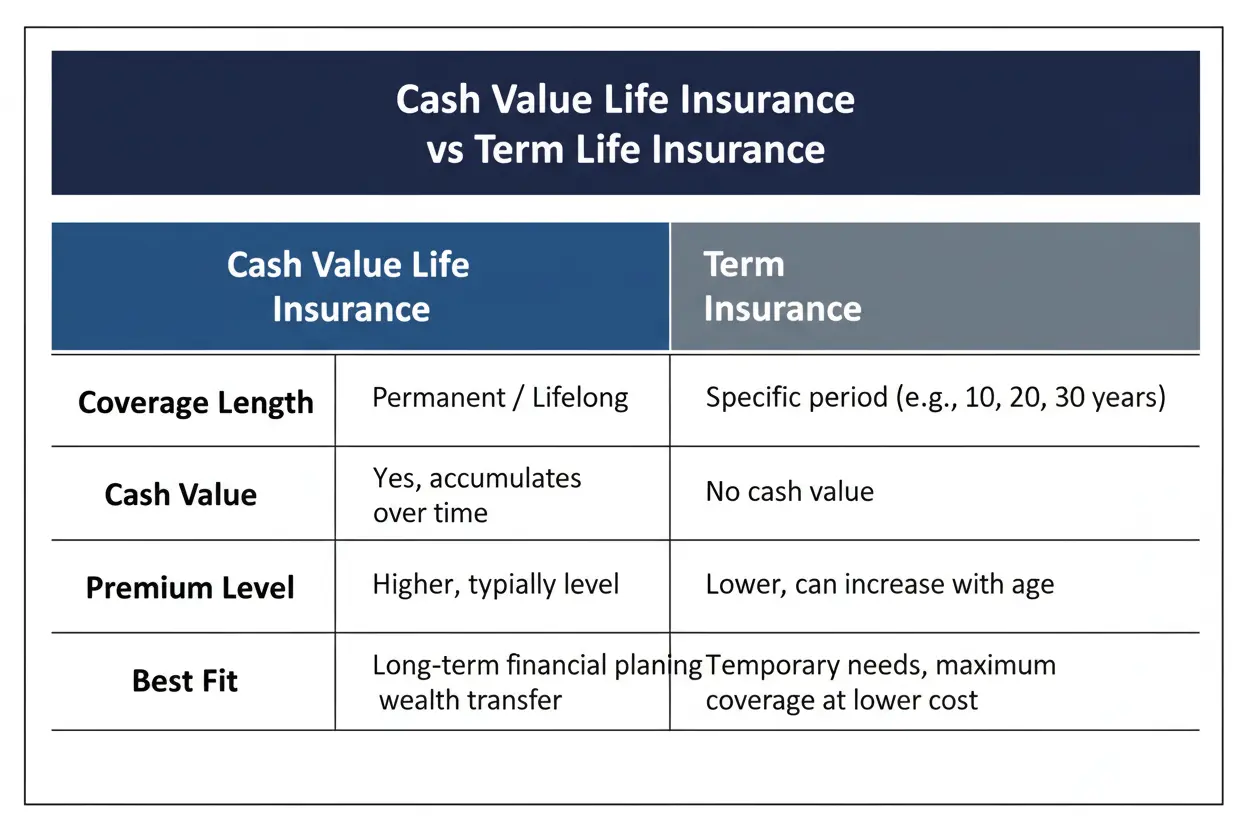

Cash Value Life Insurance Vs Term Life Insurance

Term life insurance covers you for a set period and does not build cash value. Cash value life insurance is designed for lifelong coverage and includes an accumulation component.

The right choice depends on your time horizon and financial priorities. Many people use term insurance for temporary needs and permanent coverage for legacy, lifetime dependents, or long-range planning.

| Feature | Cash Value Life Insurance | Term Life Insurance |

|---|---|---|

| Coverage length | Permanent if funded | Temporary term length |

| Cash value | Builds internal value | No cash value |

| Premium level | Higher, policy dependent | Lower initially |

| Best fit | Lifetime planning and flexibility needs | Income replacement during key years |

This comparison highlights the structural differences, but the best decision comes from matching the policy to the purpose and budget.

Who Cash Value Life Insurance Can Be A Good Fit For

Cash value life insurance is often chosen when someone wants permanent coverage plus the ability to build value inside the policy. It can also appeal to those who want a structured way to save with insurance features, while accepting added cost and complexity.

It is less suitable when the primary need is low-cost coverage for a limited time frame.

- People with lifelong dependents. Permanent coverage can support care needs that do not end at retirement.

- Households focused on estate planning. Death benefit proceeds can help with liquidity needs and legacy goals.

- Business owners. Certain designs can support buy-sell planning or key person coverage when permanence matters.

- High savers needing diversification. Some use it as a complement to other tax-advantaged strategies, with careful attention to costs and funding limits.

If the priority is purely maximum death benefit per dollar, term insurance often wins on efficiency.

What To Review Before You Buy?

Policies can look similar on the surface while performing very differently. The purchase decision should be based on contract mechanics, illustrated assumptions and how sensitive the plan is to interest rates or cap changes.

Focusing on a few critical checkpoints can reduce the chance of disappointment later.

Policy Illustration and Assumptions

An illustration is a projection, not a promise, unless a value is explicitly guaranteed. Ask to see guaranteed values, current assumptions and reduced crediting scenarios so you can gauge how resilient the policy is.

Also review whether the policy is designed for level premiums, flexible funding, or accelerated cash value growth, since those goals can conflict.

Surrender Period and Liquidity Limits

Many policies have surrender charges that make early exit costly. Confirm how long the surrender period lasts, whether partial withdrawals are restricted and how loans are treated during early years.

Liquidity is usually better viewed as a long-term feature rather than a short-term cash reserve.

Carrier Strength and Contract Guarantees

Cash value life insurance is a long-duration contract, so insurer stability matters. Review financial strength ratings, underwriting reputation and how the carrier has managed crediting rates or caps over time.

Also verify which elements are guaranteed and which can change, including cost of insurance charges in certain universal life designs.

Common Misunderstandings to Avoid

Confusion often comes from treating cash value as identical to an investment account or assuming illustrated values are inevitable. These policies can be useful, but they require realistic expectations and consistent funding.

Clarifying a few points up front can prevent costly mistakes.

- Cash value is not free money. Growth occurs after policy charges and depends on crediting rules.

- Loans are not risk free. Interest and compounding loan balances can threaten policy durability.

- Flexibility can cut both ways. Underfunding a flexible premium policy can lead to lapse risk.

- Early years can look slow. Many designs need time to overcome initial costs and surrender charges.

With a clear understanding of mechanics, you can judge whether the tradeoffs make sense for your goals.

Conclusion

Cash value life insurance combines permanent coverage with an internal cash value that can grow over time. It can support lifetime protection, long-term planning and structured access to funds, but it is more expensive and complex than term life insurance.

The best outcome comes from matching the policy type to your needs, reviewing guarantees versus projections and understanding how fees, loans and withdrawals affect long-term performance.