Shopping for life insurance in your 50s is less about finding a bargain and more about locking in dependable protection before rates rise again. Your priorities may also shift, with retirement timing, debt and family needs changing faster than they did in your 30s.

This guide breaks down the main policy types, underwriting paths and planning moves that often matter most between 50 and 59. The goal is to help you choose coverage that stays useful and affordable through your 60s and beyond.

Why Coverage Needs Change After 50?

Many people reach their 50s with a mix of responsibilities that can be hard to balance. Adult children may still need support, a spouse may depend on one income and retirement savings may not be fully funded yet.

At the same time, the financial risk of a premature death can still be significant. Life insurance can protect a partner’s lifestyle, prevent rushed asset sales and keep long-term plans intact.

Common goals for life insurance over 50 include income replacement, paying off a mortgage, covering final expenses, supporting a surviving spouse and leaving a legacy. Some buyers also want coverage that can help fund a trust or charitable giving plan.

Term Life Insurance Options

Term life insurance is often the most cost-efficient way to get a large death benefit. It is designed for a specific period, such as 10, 15, 20, or 30 years and it typically has no cash value component.

In your 50s, term coverage can be a strong fit if you have a clear time horizon for your needs. Many people align the term length to mortgage payoff, retirement date, or the years a spouse would rely on their income.

Pay attention to what happens after the initial level term period. Some policies increase sharply at renewal, so it helps to plan for whether you intend to keep the policy long-term or replace it later.

- Level term: Premiums usually stay the same during the level period, which can simplify budgeting.

- Convertible term: Some policies allow conversion to permanent coverage without a new medical exam, which can add flexibility.

- Decreasing term: The death benefit declines over time and can pair with a reducing mortgage balance, though availability varies.

Once you narrow the type, the next decision is the amount and duration that match your real obligations.

Whole Life Insurance Options

Whole life insurance is permanent coverage with fixed premiums and a guaranteed death benefit as long as premiums are paid. It also includes a cash value component that grows based on the policy design and some policies may pay dividends, though dividends are not guaranteed.

In your 50s, whole life is often used for lifelong needs such as final expenses, leaving money to heirs, or equalizing an inheritance. It can also appeal to people who want predictable premiums and do not want to revisit coverage later.

Whole life can be more expensive than term, so the tradeoff is usually between budget and permanence. It is important to understand policy fees, surrender charges and how long it takes for cash value to become meaningful.

Universal Life Insurance Options

Universal life insurance is permanent coverage with more flexibility than whole life. Depending on the policy, you may be able to adjust premiums and sometimes the death benefit, within limits and subject to the policy’s cost structure.

There are several subtypes and features vary by carrier. Some versions focus on guaranteed death benefit protection, while others emphasize cash value growth tied to interest crediting methods.

- Guaranteed universal life: Often designed to keep coverage in force to a specific age, with less focus on cash value.

- Indexed universal life: Cash value is credited based on an index method with caps and participation rates and it is not direct market investment.

- Variable universal life: Cash value can be invested in subaccounts and carries market risk, which may not fit every risk tolerance.

Universal life can work well when you need permanent coverage but want a design that better fits your budget, time horizon and risk comfort.

Guaranteed Issue and Final Expense Policies

Guaranteed issue life insurance usually has no medical exam and asks few, if any, health questions. It can be accessible for people with serious health conditions, but it often comes with higher premiums for lower coverage amounts.

Many guaranteed issue and simplified issue policies include a graded benefit period. During the early years, the full death benefit may not be paid for some causes of death, so reading the benefit schedule is critical.

Final expense insurance is commonly a small whole life policy meant to cover funeral and end-of-life costs. It can be a practical solution when the main goal is to reduce the burden on family and avoid using savings for these expenses.

How Health and Underwriting Affect Rates?

Underwriting is the process insurers use to assess risk and set premiums. In your 50s, the difference between preferred and standard health classifications can be large, so preparation can pay off.

Medical exams, lab work, prescription history and medical records may be reviewed. Insurers also look at tobacco use, blood pressure, cholesterol, A1C, BMI, driving history and sometimes hobbies.

If you take medications for common conditions, it does not automatically mean you will be declined. Stable management, good follow-up and consistent labs often matter as much as the diagnosis itself.

- Be consistent on applications: Mismatched dates or conditions can slow approval and trigger extra documentation.

- Prepare for the exam: Hydration and avoiding heavy meals or alcohol beforehand can help reduce lab volatility.

- Disclose tobacco use accurately: Nicotine classifications can affect premiums for years and may be verified.

Once you understand how underwriting works, you can pick a policy path that fits your health profile and timing.

Choosing The Right Coverage Amount

A good coverage amount is tied to your obligations, not a generic multiple of income. The right number also depends on whether your spouse or partner would keep working and how much retirement savings is already in place.

Start with essential needs such as replacing income for a set number of years, paying off a mortgage or other debt and covering final expenses. Then consider goals like college support for dependents or a legacy gift.

- Income needs: Estimate how many years of income your household would need and how benefits like Social Security survivor benefits affect the gap.

- Debt and housing: Include mortgage payoff, HELOCs and any co-signed debt that would remain.

- Cash reserves: Account for emergency savings and retirement assets that are realistically available to a survivor.

- Taxes and beneficiaries: Consider whether beneficiaries may face estate liquidity needs depending on your state and overall estate plan.

After you set the target, you can decide whether to use one policy or layer multiple policies to manage cost.

Comparing Policy Types Side By Side

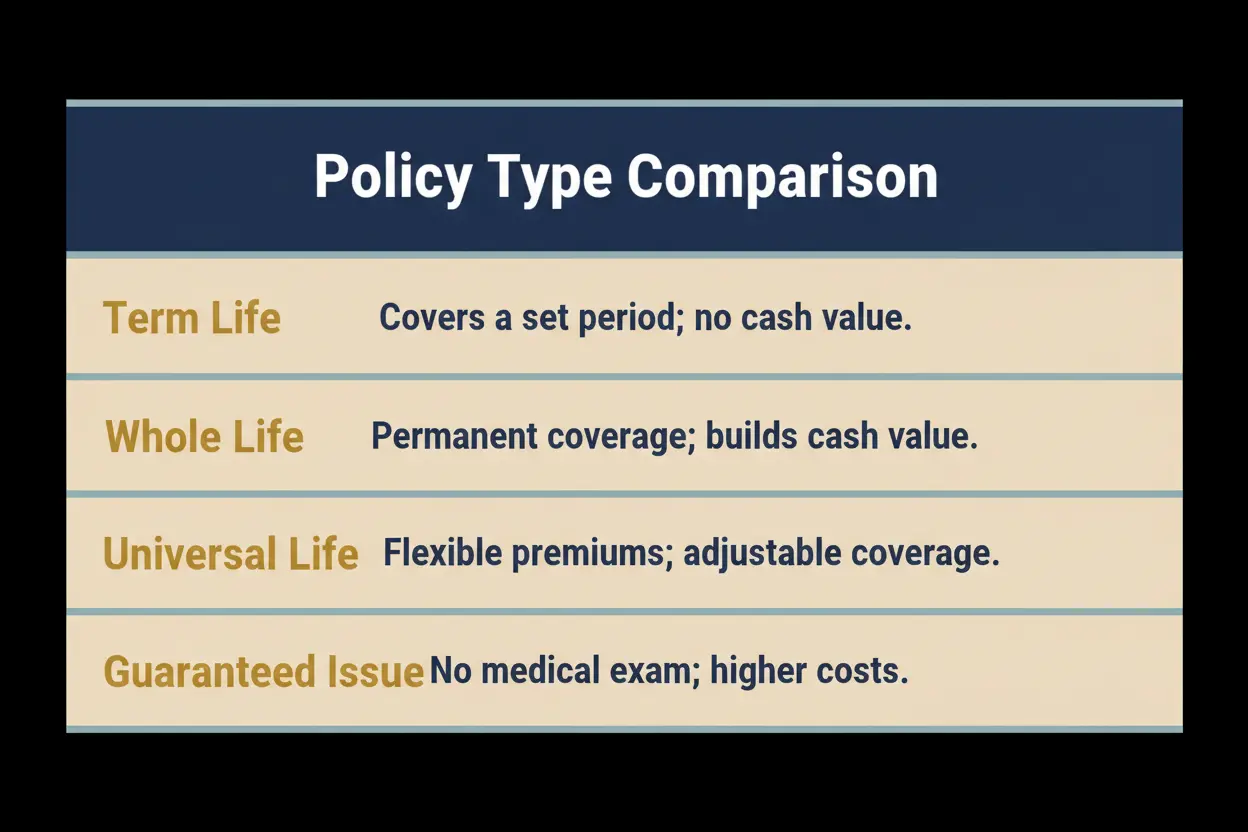

Different life insurance options solve different problems. A direct comparison helps you see which tradeoffs are acceptable for your budget and planning goals.

| Policy Type | Best Fit In Your 50s | Key Tradeoffs |

|---|---|---|

| Term Life | High coverage for a fixed time window such as mortgage or income needs | No cash value and renewal premiums can jump after the level period |

| Whole Life | Lifelong protection for final expenses, inheritance planning and predictable premiums | Higher premiums and slower cash value growth in early years |

| Universal Life | Permanent coverage with flexibility, including guaranteed death benefit designs | Costs and performance assumptions matter, especially for cash value focused designs |

| Guaranteed Issue | Access to coverage when health conditions limit other options | Lower coverage amounts, higher cost per dollar and possible graded benefits |

With the main types clear, the next step is to evaluate features that can change how the policy behaves later.

Riders and Features To Consider

Riders can add protections that matter more in your 50s, especially if you are planning for retirement risks. Not every rider is worth the added cost, so focus on features that solve a specific problem.

- Accelerated death benefit: Allows access to part of the death benefit for qualifying terminal illness, which can help protect savings.

- Chronic or critical illness rider: May provide benefits for certain long-term care needs, but definitions and limits vary.

- Waiver of premium: Can keep coverage active if disability prevents you from working, subject to rider terms.

- Guaranteed insurability: Lets you buy more coverage later without new underwriting, though it is less common at older ages.

- Conversion option: For term policies, this can be a valuable safety net if health changes before the term ends.

Once you choose riders, it helps to confirm the policy aligns with your estate plan and beneficiary structure.

Beneficiaries and Estate Planning Basics

Beneficiary designations control who receives the death benefit and they should match your broader plan. A mismatch between a will and a beneficiary form can create delays and disputes.

Review primary and contingent beneficiaries and keep them current after marriage, divorce, or a death in the family. If your situation is complex, a trust may be appropriate, but it should be set up correctly to avoid unintended tax or control issues.

If your estate is large or you have special family circumstances, it can be worth coordinating with a qualified attorney. Clear documentation improves trust and reduces the chance of claim complications later.

How to Apply Before You Turn 60?

Applying in your 50s often gives you more choices than waiting, especially if health is stable. A structured approach helps you avoid coverage gaps and reduces the chance of delays.

- Clarify the purpose. Decide whether the need is temporary, lifelong, or a mix so you can choose term, permanent, or layered coverage.

- Gather health and financial details. Compile medications, diagnoses, physician contact information and basic income and debt numbers to speed underwriting.

- Choose an underwriting path. Decide between fully underwritten, simplified issue and guaranteed issue based on health and desired coverage size.

- Compare more than price. Review renewal terms, conversion options, riders and carrier financial strength rather than focusing only on the monthly premium.

- Time the effective date carefully. Keep existing coverage active until the new policy is approved, in force and paid as required.

This process is simple, but it works best when you stay organized and avoid rushing the medical and beneficiary details.

Common Mistakes To Avoid

Small missteps can make life insurance over 50 more expensive or less useful than it should be. Most issues come from buying the wrong duration, misunderstanding policy mechanics, or letting coverage lapse during transitions.

- Buying too short a term: A low premium can look attractive, but it can create a forced renewal or replacement when rates are higher.

- Overpaying for cash value you will not use: Permanent coverage is useful, but only when it matches a lifelong need or a specific strategy.

- Ignoring graded benefits: Some policies do not pay the full death benefit immediately, which can undermine the goal of quick protection.

- Leaving beneficiaries outdated: Old designations can send money to the wrong person and cause avoidable family conflict.

- Canceling too early: Dropping current coverage before the new policy is active can leave a gap during underwriting delays.

A quick review of these pitfalls can prevent costly surprises and keep your plan stable through retirement transitions.

Conclusion

Life insurance over 50 is about making a clean match between your remaining responsibilities and the type of coverage that can carry you into retirement. Term can handle time-limited risks, while whole life and universal life can cover permanent needs and legacy goals.

Focus on health-driven underwriting realities, solid beneficiary choices and policy features that will still matter in your 60s. When the coverage amount, term length and policy type fit your plan, you gain protection that stays dependable instead of becoming a burden.

FAQ’s

1: Is it worth buying life insurance after age 50?

Yes, buying life insurance after 50 can still provide valuable financial protection. It can help replace income, pay off remaining debts, cover funeral expenses and support a surviving spouse or family members. The key is choosing a policy that fits your current financial goals, health and retirement plans.

2: Can you get life insurance over 50 without a medical exam?

Yes, many insurers offer no-medical-exam options, including simplified issue and guaranteed issue life insurance. These policies can make it easier to qualify, especially if you have health concerns. However, they may have higher premiums, lower coverage limits, or graded death benefits compared to fully underwritten policies.

3: How can you lower the cost of life insurance in your 50s?

You can reduce life insurance costs by applying while you’re still in good health, comparing quotes from multiple insurers, selecting only the coverage you need and avoiding unnecessary riders. If your needs are temporary, a term life policy may also provide more affordable protection than permanent coverage.