Becoming a parent changes what financial security means. Life insurance can turn a worst day into a survivable one by replacing income, paying debts and protecting a child’s future.

As you compare options, focus on the amount of coverage, how long you need it and how it fits your budget. A solid plan feels boring and predictable, which is exactly the point.

Why New Parents Often Need Life Insurance?

Parenthood creates long-term obligations that do not pause if a wage earner dies. Life insurance provides cash when it is needed most, without forcing a surviving parent to sell assets quickly.

Coverage can help with everyday bills, childcare and housing costs. It can also cover major expenses that may otherwise become unmanageable during grief.

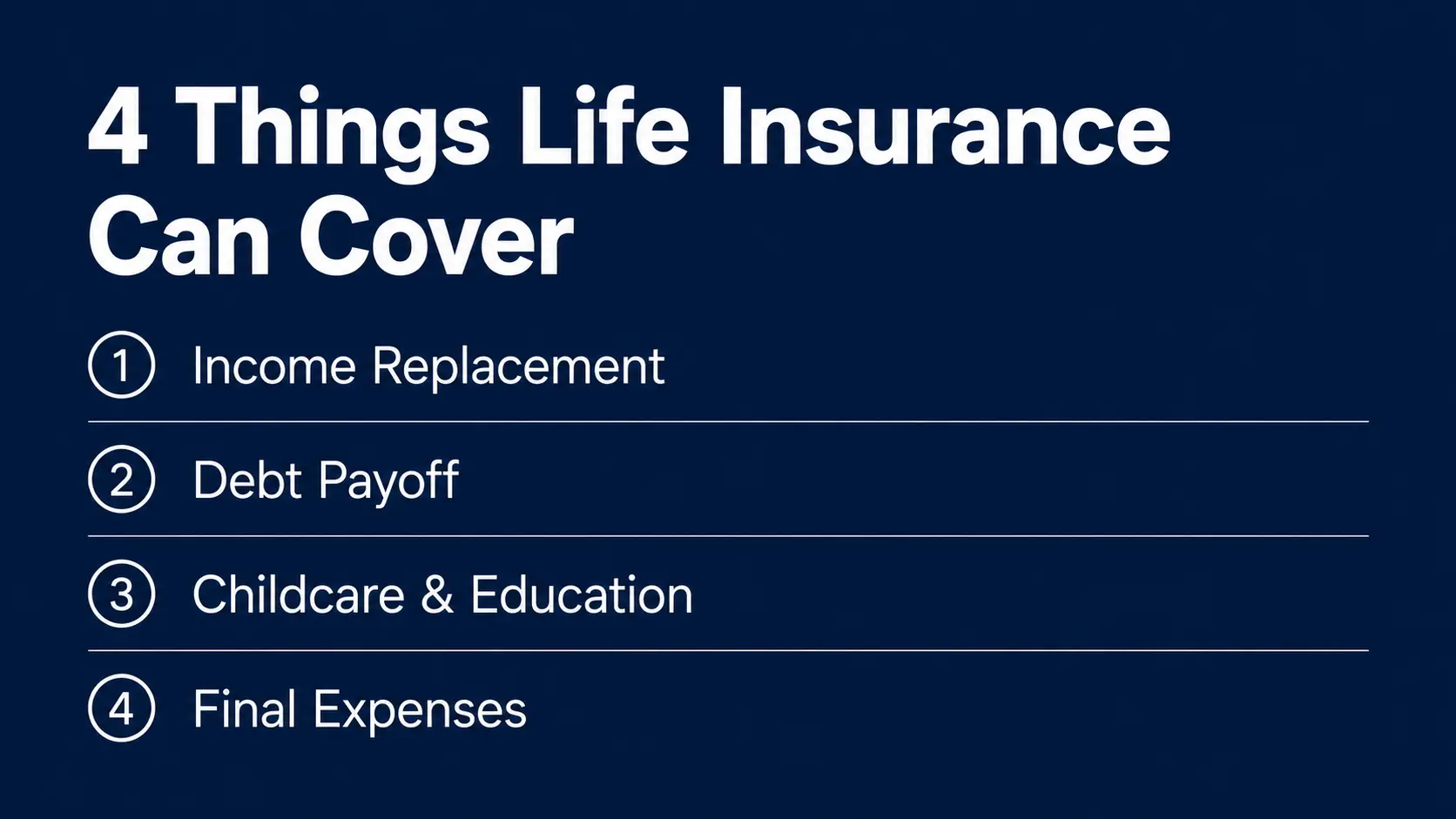

- Income replacement: Helps maintain the household standard of living while a family adjusts.

- Debt payoff: Can eliminate a mortgage, car loans, or private student loans tied to cash flow.

- Childcare and education: Supports daycare, after-school care and future schooling expenses.

- Final expenses: Covers funeral costs and medical bills that can arrive quickly.

Once you know what you want coverage to do, choosing a policy type and amount becomes much clearer.

How Much Coverage Should You Consider?

A useful starting point is to estimate how much money your family would need if one parent died. This is not just income replacement, because the surviving parent may need added support for childcare and time off work.

Many families combine short-term needs, long-term needs and existing resources. The goal is to avoid both underinsuring and overpaying for coverage you do not need.

- Replace earnings: Consider years of income needed until children are adults or a partner is financially stable.

- Cover big fixed costs: Mortgage balance, rent support and any loans that would strain the budget.

- Plan for child-related costs: Ongoing childcare, healthcare copays and education savings goals.

- Subtract available resources: Savings, employer benefits and existing policies already in place.

This approach keeps the calculation practical and tied to real obligations rather than a random multiple.

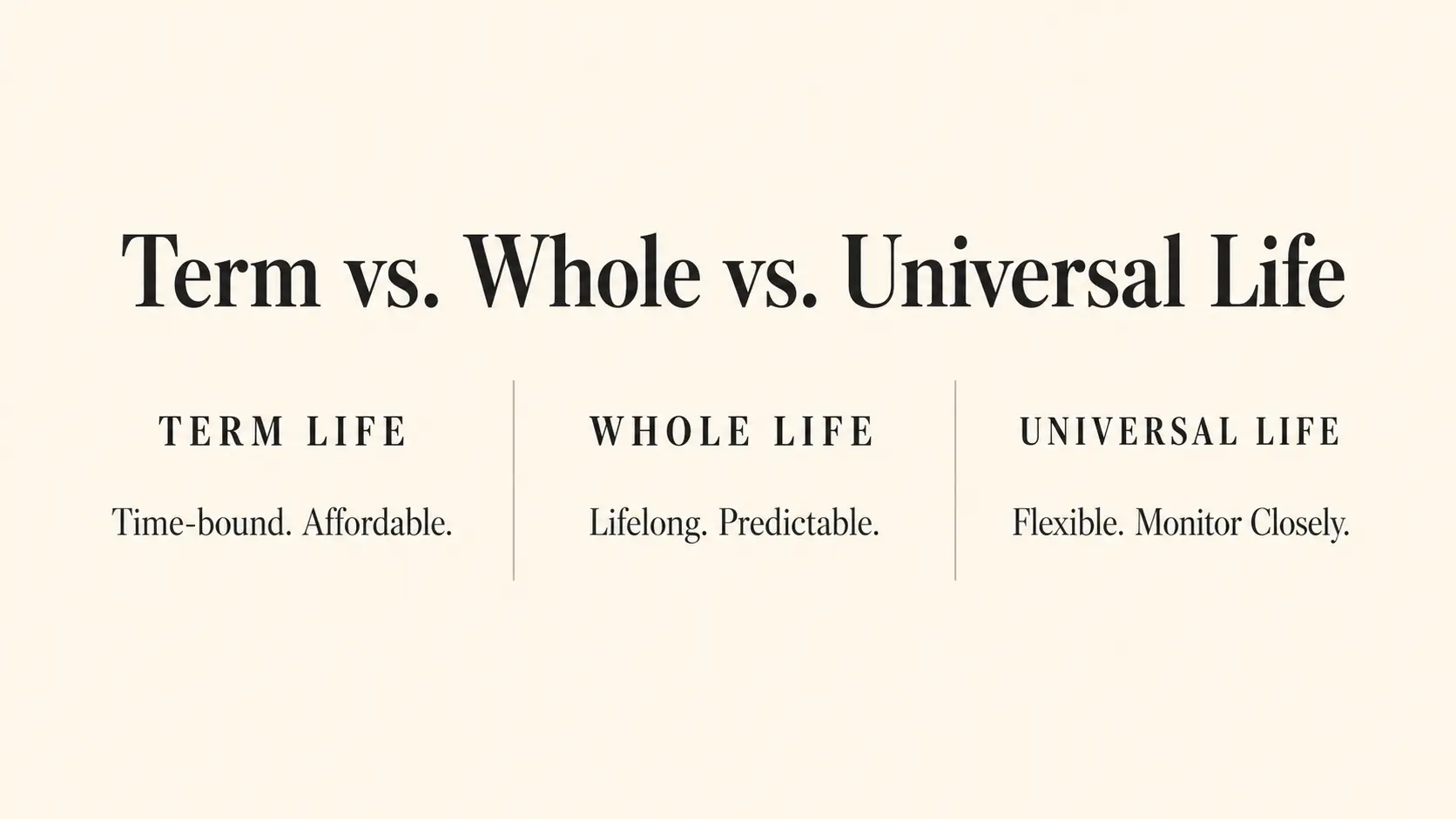

Term Life Insurance and When It Fits Best

Term life insurance is usually the simplest way for new parents to buy a large death benefit for a lower premium. It lasts for a set period, such as 10, 20, or 30 years and then expires unless renewed.

It often fits well when most obligations are time-limited, such as raising children, paying a mortgage, or replacing income during peak earning years. It can also be layered with more than one policy to match changing needs.

- Pros: High coverage for lower cost, easy to compare, strong fit for time-bound needs.

- Cons: Coverage can become expensive to renew later, no cash value, expires if you outlive the term.

If your main goal is protection while your kids are dependent, term coverage is often the first policy to evaluate.

Whole Life and Other Permanent Coverage Options

Permanent life insurance is designed to last your entire life as long as premiums are paid. It typically costs more than term, but it can offer stable premiums and a cash value component.

Whole life is one common form and it is usually more predictable than flexible policies. Permanent coverage may suit families who want lifelong protection, have a dependent with special needs, or want to leave a legacy.

- Whole life: Level premiums, guaranteed death benefit and cash value growth based on the policy design.

- Universal life: More flexibility in premiums and cash value, but it requires careful monitoring.

- Guaranteed issue policies: Easier approval, but often smaller benefits and higher costs per dollar of coverage.

Permanent coverage can be valuable, but it should be selected for a specific reason, not because it sounds more complete.

Coverage Length and Matching It to Parenting Timelines

The best term length is usually tied to your longest financial obligation. For many families, that is the time until the youngest child becomes independent, the mortgage is paid down, or retirement savings are on track.

Longer terms can lock in insurability and pricing for more years, but they cost more each month. A shorter term can be fine if the budget is tight and you plan to reassess as income grows.

- 10-year term: Useful when you expect a big change soon, such as returning to work or paying off a large debt.

- 20-year term: Often aligns with raising children through major schooling years.

- 30-year term: Common when a large mortgage and young children create long-lasting obligations.

Choosing the length first helps you avoid buying the wrong policy just because the premium looks attractive.

Two-Parent Households and Stay-at-Home Parents

Life insurance is not only for the highest earner. The financial impact of losing a stay-at-home parent can be significant because paid services replace unpaid work.

Coverage on both parents can protect against the costs of childcare, housekeeping support and the income hit if a working parent reduces hours. It can also prevent the survivor from draining savings just to keep routines stable.

- Working parent: Focus on income replacement and long-term stability.

- Stay-at-home parent: Focus on childcare costs, household management and transition support.

- Both parents: Consider a coordinated plan so benefits and terms align with shared goals.

Thinking in terms of household function, not just paychecks, leads to more realistic coverage decisions.

Riders and Features Worth Considering

Policy riders can add flexibility, but they also add cost and complexity. The best riders are the ones that protect against common risks for young families and reduce the need to buy additional policies later.

Keep the focus on features that directly support your family if your health or income changes.

- Waiver of premium: Can keep the policy in force if disability prevents you from paying premiums.

- Convertible term option: Allows switching to permanent coverage later without a new medical exam.

- Child term rider: Adds limited coverage for children, often to handle final expenses.

- Accelerated death benefit: May allow early access to part of the benefit with a qualifying terminal illness.

Before adding riders, confirm what your employer benefits already provide and where the gaps remain.

Medical Underwriting and When to Apply

Most individual policies require a health application and sometimes a medical exam. Applying earlier can help if you are younger and healthier and it reduces the risk of waiting until after a diagnosis changes your pricing.

New parents are often busy, so scheduling the process matters. Gather basic health history, current medications and recent doctor visits so the application is accurate.

- Define the need. Choose a target death benefit, a term length and who needs coverage.

- Compare quotes and policy details. Review premiums, conversion options and exclusions rather than price alone.

- Complete underwriting. Provide health information, attend an exam if required and respond quickly to follow-ups.

- Lock in beneficiaries and ownership. Set primary and contingent beneficiaries and confirm who owns the policy.

A smooth underwriting process usually comes down to good paperwork and quick responses.

Common Mistakes New Parents Should Avoid

Life insurance decisions can go off track when parents buy based on fear or incomplete information. Avoiding a few predictable mistakes can save money and reduce the chance of coverage gaps.

These pitfalls are common because many families purchase insurance while sleep-deprived and managing new expenses.

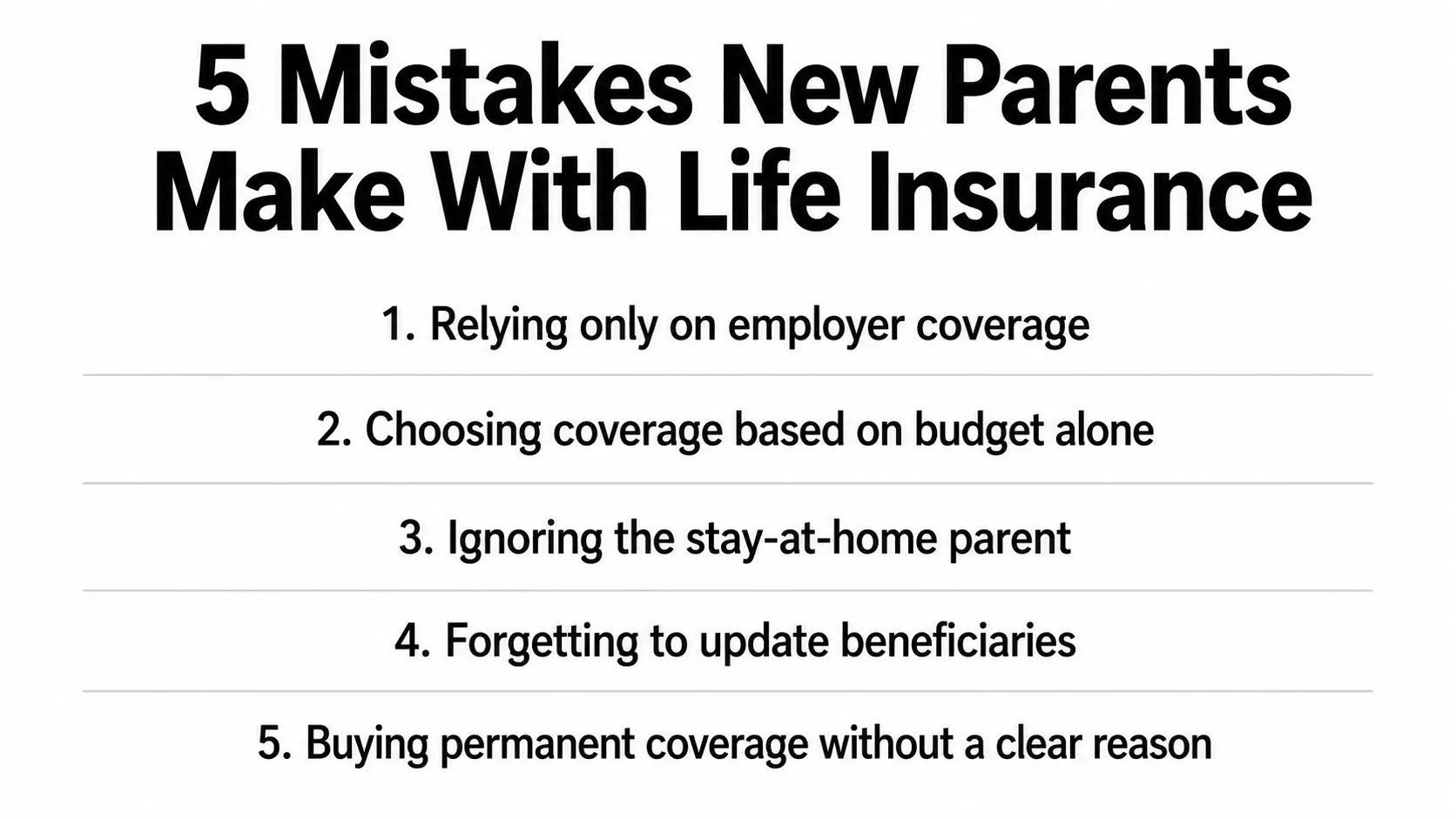

- Relying only on employer coverage: Workplace policies may be limited and may not follow you if you change jobs.

- Choosing a death benefit based only on budget: A low premium is not helpful if it does not protect essentials.

- Ignoring the stay-at-home parent: Replacement childcare and household support can be costly.

- Forgetting to update beneficiaries: Life changes can make an old beneficiary designation risky.

- Buying permanent coverage without a clear reason: Higher premiums can strain a young family budget.

Fixing these issues early makes the rest of your financial plan easier to maintain.

Quick Comparison of Policy Types

Seeing key tradeoffs side by side helps you make a decision without getting lost in jargon. Use this as a starting point, then confirm details in the actual policy illustration and contract.

| Policy Type | Best Fit For | Main Tradeoff |

|---|---|---|

| Term Life | Income replacement while children are dependent | Ends after the term unless renewed |

| Whole Life | Lifelong protection and predictable premiums | Higher cost compared with term |

| Universal Life | Families needing flexibility with premiums and cash value | Requires monitoring to avoid policy underfunding |

| Employer Group Life | Basic coverage at work and supplemental protection | May not be portable and can be limited |

Once you pick a policy type, the next priority is aligning the coverage amount and term with your real obligations.

Conclusion

Life insurance for new parents is about protecting time, stability and options for the people who depend on you. The most effective plan replaces income, covers major debts and funds transition costs without straining monthly cash flow.

Start with a clear coverage goal, choose a term length that matches your parenting timeline and insure both parents when household responsibilities would be costly to replace. Review beneficiaries and coverage every few years so the policy keeps pace with your family.

Life Insurance FAQs for New Parents

1. How much life insurance do new parents usually need?

New parents should consider enough coverage to replace income, pay major debts, cover childcare and support future education costs. A practical way is to list your family’s monthly expenses, long-term obligations and existing savings before choosing a coverage amount.

2. Is term life insurance better for new parents?

Term life insurance is often a good choice for new parents because it provides higher coverage at a lower cost for a fixed period. It works well when your main goal is to protect your family while your children are young and financially dependent.

3. What is the biggest life insurance mistake new parents make?

One of the biggest mistakes is relying only on employer-provided life insurance. Workplace coverage may be limited and may not continue if you change jobs, so many families need a personal policy for stronger long-term protection.