Health insurance can feel confusing when you first start researching plans. Between deductibles, premiums, provider networks, copays, and acronyms like HMO, PPO, and EPO, many people struggle to understand how coverage actually works.

That’s why this health insurance beginner guide was created.

Whether you are choosing your first health plan, changing jobs, becoming self-employed, or simply trying to lower healthcare costs, understanding the basics of health insurance is essential in 2026.

The good news is that health insurance becomes much easier to understand once you learn the core concepts.

In this guide, we’ll explain how health insurance works, common plan types, important insurance terms, and how to choose the right plan for your needs.

[cta_alert id=”3100″]

What Is Health Insurance?

The first step in any health insurance beginner guide is understanding what health insurance actually does.

Health insurance helps pay for medical expenses such as:

- Doctor visits

- Hospital stays

- Prescription medications

- Emergency care

- Preventive services

- Surgeries and treatments

Instead of paying the full cost of healthcare yourself, you share costs with the insurance company.

In exchange for monthly payments called premiums, your insurer helps cover eligible healthcare expenses.

Why Health Insurance Matters

Healthcare costs continue rising every year.

Without coverage, even a single medical emergency can create massive financial stress.

A strong health insurance beginner guide should explain that insurance helps protect you from:

- Unexpected hospital bills

- Expensive surgeries

- Emergency room costs

- Long-term medical treatment expenses

Health insurance also improves access to preventive care and routine medical services.

Understanding Monthly Premiums

One of the most important concepts in a health insurance beginner guide is the monthly premium.

A premium is the amount you pay each month to maintain your health insurance coverage.

Even if you do not use medical services, you still pay your premium to keep the plan active.

Generally:

- Lower premiums often mean higher out-of-pocket costs

- Higher premiums may reduce costs when you receive care

Choosing the right balance depends on your healthcare needs and budget.

What Is a Deductible?

A deductible is another key concept in any health insurance beginner guide.

Your deductible is the amount you pay for healthcare services before your insurance starts sharing costs.

For example:

- If your deductible is $2,000, you pay the first $2,000 of eligible medical expenses yourself before insurance contributes.

Plans with lower premiums often have higher deductibles.

Understanding this trade-off is essential when comparing health plans.

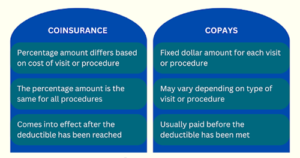

Understanding Copays and Coinsurance

After meeting your deductible, you may still share healthcare costs through:

Copays

Fixed amounts you pay for services, such as:

- $30 doctor visits

- $15 prescriptions

Coinsurance

A percentage of healthcare costs shared between you and your insurer.

Example:

- Insurance pays 80%

- You pay 20%

A good health insurance beginner guide helps people understand that healthcare costs are often shared in multiple ways.

What Is an Out-of-Pocket Maximum?

Your out-of-pocket maximum is the most you pay for covered healthcare services during a plan year.

After reaching this limit:

- Insurance usually pays 100% of covered services

This protection helps prevent catastrophic medical debt.

Understanding out-of-pocket maximums is extremely important when choosing a plan.

[cta_alert id=”3103″]

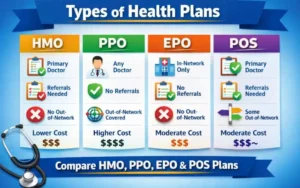

Common Health Insurance Plan Types

A complete health insurance beginner guide should explain the major types of health insurance plans.

HMO (Health Maintenance Organization)

- Lower costs

- Requires primary care physician referrals

- Limited provider network

PPO (Preferred Provider Organization)

- More provider flexibility

- No referral requirements

- Higher premiums

EPO (Exclusive Provider Organization)

- In-network care only

- No referral requirements

- Often lower premiums than PPOs

If you want to better understand EPO plans, check out EPO Health Insurance Benefits for a detailed explanation of how EPO coverage works.

What Is a Provider Network?

Provider networks are groups of doctors, hospitals, and healthcare providers that work with insurance companies.

A strong health insurance beginner guide should explain the difference between:

In-Network Providers

- Lower costs

- Pre-negotiated pricing

Out-of-Network Providers

- Higher costs

- Limited coverage in some plans

Using in-network providers usually saves money.

Preventive Care and Why It Matters

Most health insurance plans cover preventive care services such as:

- Annual checkups

- Vaccinations

- Screenings

- Wellness visits

Preventive care helps detect health problems early before they become more expensive and serious.

Many preventive services are covered without additional costs.

How Prescription Drug Coverage Works

Prescription benefits are another important part of any health insurance beginner guide.

Insurance plans often organize medications into tiers:

- Generic drugs

- Preferred brand-name drugs

- Specialty medications

Higher-tier medications usually cost more.

Always review a plan’s prescription drug coverage before enrolling.

EPO Plans Are Becoming More Popular

EPO plans are gaining attention because they often balance affordability with flexibility.

Many people researching a health insurance beginner guide are now considering EPO options due to:

- Lower monthly premiums

- No specialist referrals

- Strong provider networks

To learn more, visit EPO Health Insurance Benefits for a deeper look at EPO plan advantages and limitations.

Employer Health Insurance vs Marketplace Plans

There are several ways to get health insurance.

Employer-Sponsored Insurance

- Offered through work

- Employers often pay part of premiums

Marketplace Plans

- Purchased individually

- Available through ACA exchanges

Government Programs

- Medicaid

- Medicare

- CHIP

Your income, employment status, and healthcare needs affect which option is best.

How to Choose the Right Health Plan

A complete health insurance beginner guide should help readers compare plans carefully.

Consider factors such as:

- Monthly premiums

- Deductibles

- Provider networks

- Prescription coverage

- Out-of-pocket maximums

- Specialist access

Choosing the cheapest plan is not always the best financial decision long term.

Common Health Insurance Mistakes

Many beginners make avoidable insurance mistakes, including:

- Ignoring provider networks

- Choosing plans based only on premiums

- Not understanding deductibles

- Overlooking prescription coverage

- Skipping preventive care

Learning these basics early can help avoid expensive surprises later.

Why Health Insurance Is Changing in 2026

Healthcare and insurance continue evolving rapidly.

Modern trends affecting this health insurance beginner guide include:

- Telehealth growth

- Rising healthcare costs

- AI-powered healthcare tools

- Expanded wellness programs

- More high-deductible plans

Consumers now have more plan choices than ever before, making education increasingly important.

Health Insurance Literacy Helps You Save Money

Understanding insurance basics can help people:

- Avoid unnecessary healthcare costs

- Choose better plans

- Use preventive care effectively

- Reduce surprise medical bills

- Make smarter financial decisions

Health insurance literacy is becoming an essential life skill.

If you are considering EPO coverage specifically, review EPO Health Insurance Benefits for more detailed insights into how these plans compare to other network types.

Final Thoughts

Understanding health insurance may seem overwhelming at first, but learning the basics can make a huge difference financially and medically.

This health insurance beginner guide covered the essential concepts every consumer should know, including premiums, deductibles, provider networks, plan types, and cost-sharing structures.

The more you understand your health plan, the better prepared you’ll be to manage healthcare expenses and make informed coverage decisions in 2026 and beyond.

For more healthcare planning resources and insurance insights, visit Quote Maestro.

[cta_alert id=”3105″]

FAQs About Health Insurance Beginner Guide

What is health insurance?

Health insurance helps cover medical expenses such as doctor visits, hospital stays, prescriptions, and preventive care.

What is a deductible?

A deductible is the amount you pay for healthcare services before insurance begins sharing costs.

What is the difference between HMO, PPO, and EPO plans?

HMOs require referrals, PPOs offer more flexibility, and EPOs typically require in-network care without referrals.

Why are provider networks important?

Using in-network providers usually lowers healthcare costs and improves coverage access.

What is an out-of-pocket maximum?

It is the maximum amount you pay for covered healthcare services during a plan year.

Are EPO plans good for beginners?

Yes, many EPO plans offer affordable premiums and simplified specialist access, making them attractive for first-time insurance buyers.