When choosing a health plan, one of the most important—but often misunderstood—features is the health insurance out-of-pocket maximums limit.

This limit is your financial safety ceiling. It ensures that no matter how expensive your medical care becomes in a year, your spending on covered services will not exceed a fixed amount.

In simple words:

👉 It is the maximum amount you will pay before insurance pays 100%.

To explore more insurance education resources, visit:

https://quotemaestro.com/

[cta_alert id=”3100″]

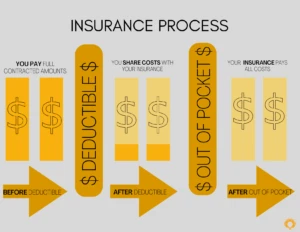

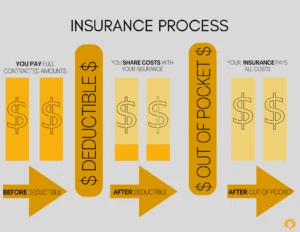

What Are Health Insurance Out-of-Pocket Maximums?

The health insurance out-of-pocket maximums refer to the total amount you are responsible for paying in a policy year before your insurance company fully covers eligible medical costs.

It typically includes:

- Deductibles (what you pay first)

- Copayments (fixed visit charges)

- Coinsurance (percentage of costs you share)

Once you hit the annual out-of-pocket limit, your insurer pays 100% of covered essential health benefits.

What Does NOT Count Toward the Maximum?

Many people misunderstand this part of health insurance out-of-pocket maximums.

Usually NOT included:

- Monthly premiums

- Cosmetic or elective procedures

- Out-of-network penalties (in some plans)

- Non-covered treatments

That’s why two people with the same plan may still pay very different total costs.

Why Out-of-Pocket Maximums Matter More Than You Think

The health insurance out-of-pocket maximums are one of the strongest financial protections in modern healthcare systems.

They help you:

- Avoid unlimited medical bills

- Control yearly healthcare spending

- Protect family savings during emergencies

- Reduce financial stress during chronic illness treatment

Without this limit, a single hospital stay could lead to overwhelming debt.

Real-Life Example (Easy Breakdown)

Let’s say your plan has:

- Deductible: $2,000

- Coinsurance: 20%

- Out-of-pocket maximum: $7,000

You keep paying until your total spending (deductible + copays + coinsurance) reaches $7,000.

After that:

👉 Insurance pays 100% of covered services

👉 You pay $0 (for covered care only)

This is why understanding health insurance out-of-pocket maximums is so important when comparing plans.

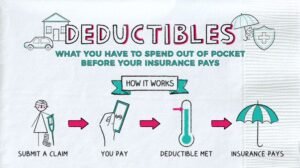

Health Insurance Maximum Limit vs Deductible

People often confuse these two:

Deductible

- You pay first before insurance starts sharing costs

Out-of-Pocket Maximum

- Total limit you pay in a year (final cap)

So basically:

👉 Deductible = starting point

👉 Out-of-pocket maximum = ending protection limit

Understanding this difference helps you avoid surprises in medical billing.

Common Mistakes People Make

Many families misunderstand health insurance out-of-pocket maximums, leading to financial stress:

- Choosing a low premium but high maximum plan

- Not checking family vs individual limits

- Ignoring prescription drug costs

- Assuming everything counts toward the limit

- Not reviewing in-network rules

These mistakes can increase your total yearly spending significantly.

Internal Insurance Insight (Important)

Some health plans separate:

- Individual out-of-pocket maximum

- Family out-of-pocket maximum

This means one person in a family might hit their limit faster, but the full family limit may still apply.

For more insurance rights and coverage issues, read here:

https://quotemaestro.com/ada-obesity-insurance-denial-rights/

Understanding this is especially important when dealing with chronic conditions or long-term treatments.

How to Choose the Best Health Plan Using Out-of-Pocket Limits

When comparing plans, always evaluate:

- Annual out-of-pocket maximum amount

- Monthly premium balance

- Hospital network coverage

- Prescription drug tier costs

- Family vs individual protection limits

A plan with slightly higher premiums but lower health insurance out-of-pocket maximums may actually save you thousands in emergencies.

Hidden Benefit Most People Don’t Know

Once you reach your health insurance out-of-pocket maximums, you don’t just save money—you gain peace of mind.

At that point:

- No surprise bills

- No percentage-based charges

- No stress during treatment decisions

This allows patients to focus fully on recovery instead of finances.

[cta_alert id=”3103″]

Smart Tips to Reduce Out-of-Pocket Costs

To maximize your benefits:

- Always use in-network providers

- Choose generic medications when possible

- Use preventive care services (often free)

- Check billing statements carefully

- Compare treatment costs before procedures

These habits help you reach your health insurance out-of-pocket maximums more strategically (and sometimes avoid unnecessary spending).

Advanced Insight (2026 Trend)

In newer health plans, insurers are increasingly:

- Adjusting out-of-pocket maximums yearly

- Separating drug vs medical spending caps

- Offering HDHP (High Deductible Health Plans) with HSAs

This makes understanding health insurance out-of-pocket maximums even more important than before.

FAQs About Health Insurance Out-of-Pocket Maximums

1. What is the main purpose of out-of-pocket maximums?

To limit the total amount you pay for covered healthcare services in a year.

2. Do all health plans have out-of-pocket maximums?

Yes, most ACA-compliant health plans include them.

3. What happens after I reach my maximum limit?

Insurance pays 100% of covered essential services.

4. Does my family share one out-of-pocket maximum?

Some plans have both individual and family limits.

5. Are prescriptions included in out-of-pocket maximums?

Yes, in most plans, prescription costs count toward the limit.

Final Thoughts

The health insurance out-of-pocket maximums are one of the most important financial protections in any health plan. While premiums get most of the attention, the out-of-pocket limit determines your real financial risk during medical emergencies.

Understanding this concept helps you choose smarter, safer, and more cost-effective health coverage.

For more insurance guides, visit:

https://quotemaestro.com/

And learn more about coverage issues here:

https://quotemaestro.com/ada-obesity-insurance-denial-rights/

https://quotemaestro.com/ada-obesity-insurance-denial-rights/

[cta_alert id=”3105″]