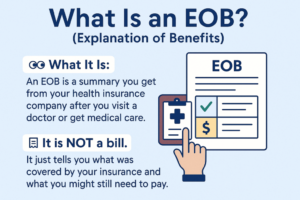

Understanding health insurance reading your EOB (Explanation of Benefits) is one of the most important skills for managing your medical bills. Many people assume an EOB is a bill—but it is NOT.

Instead, an EOB is a breakdown from your insurance company showing:

- What the provider charged

- What your insurance approved

- What they paid

- What you may owe

To explore more insurance breakdowns and financial structures, visit:

Quotemaestro Insurance Guides

[cta_alert id=”3100″]

What Is an EOB in Health Insurance?

An EOB (Explanation of Benefits) is a document sent after you receive medical care.

When focusing on health insurance reading your EOB, think of it as a receipt-style explanation—not a bill.

It includes:

- Service details (doctor visit, test, surgery)

- Total billed charges

- Insurance discounts (negotiated rates)

- Amount paid by insurance

- Your responsibility (if any)

👉 Important: You may still receive a separate bill from your provider.

Why Health Insurance Reading Your EOB Matters

Learning health insurance reading your EOB helps you:

- Catch billing errors early

- Understand insurance payments

- Avoid overpaying medical bills

- Track yearly healthcare spending

- Identify denied or reduced claims

Most billing mistakes are only discovered when patients carefully review their EOB.

Key Sections of an EOB Explained

When practicing health insurance reading your EOB, focus on these sections:

1. Provider Charges

This is the amount the hospital or doctor originally billed.

2. Allowed Amount

This is the discounted rate your insurance negotiated.

3. Insurance Paid

This shows what your insurance covered.

4. Patient Responsibility

This is what you may owe (copay, deductible, or coinsurance).

5. Adjustments

This shows discounts or reductions applied.

Common Mistakes People Make

Many people misunderstand health insurance reading your EOB, leading to confusion:

- Thinking EOB is a bill

- Ignoring denied claims

- Not checking duplicate charges

- Overlooking insurance adjustments

- Not comparing EOB with provider bills

Example of an EOB Breakdown

Let’s simplify:

- Hospital billed: $1,200

- Insurance allowed: $800

- Insurance paid: $600

- You owe: $200

Even though the hospital billed $1,200, you are NOT responsible for that full amount.

This is why health insurance reading your EOB is so important—it reveals the real cost behind the scenes.

Hidden Insight: Why Bills Don’t Match EOBs

Many people get confused when their hospital bill doesn’t match their EOB.

That’s because:

- Insurance negotiates lower rates

- Some charges are adjusted or removed

- Billing cycles may differ

If you understand health insurance reading your EOB, you can quickly spot inconsistencies.

Internal Insurance Resource (Important)

For deeper understanding of insurance funding structures, you can also explore:

Level Funded vs True Self-Funded Insurance Guide

This helps you understand how employer insurance plans process claims behind the scenes.

You can also revisit it here for comparison:

Level Funded vs True Self-Funded Insurance Guide

Understanding funding models makes health insurance reading your EOB much easier because it explains how payments are structured.

How to Check Your EOB Properly

To master health insurance reading your EOB, follow this checklist:

- Match patient name and provider details

- Compare dates of service

- Verify billed vs allowed amounts

- Check insurance payment accuracy

- Confirm your responsibility

- Look for denial codes

Even small errors can lead to unnecessary payments.

What If a Claim Is Denied?

A denial on your EOB does NOT always mean you must pay.

Common reasons:

- Missing information

- Out-of-network service

- Pre-authorization not obtained

- Coding errors

In many cases, denied claims can be appealed.

[cta_alert id=”3103″]

Tips to Avoid EOB Confusion

To improve health insurance reading your EOB, follow these smart tips:

- Keep all medical bills and EOBs together

- Compare EOB with provider invoice

- Log into your insurance portal regularly

- Ask for clarification when something looks wrong

- Track annual deductible progress

Advanced Insight: EOB vs Medical Bill

Understanding the difference is critical:

| EOB | Medical Bill |

|---|---|

| Sent by insurance | Sent by provider |

| Shows breakdown | Shows amount owed |

| Not a bill | Actual payment request |

This comparison is key to mastering health insurance reading your EOB.

Why EOB Literacy Saves Money

People who understand health insurance reading your EOB often:

- Pay fewer incorrect charges

- Detect duplicate billing

- Avoid unnecessary payments

- Maximize insurance benefits

It’s one of the simplest ways to protect your healthcare budget.

FAQs About Health Insurance Reading Your EOB

1. Is an EOB a bill?

No, it is not a bill. It is only a statement from your insurance company.

2. Why did I receive an EOB?

You received medical services and your insurance processed the claim.

3. Do I always have to pay what the EOB says?

Not always. You only pay what your provider bills you.

4. What if my EOB and bill don’t match?

Contact your provider or insurance company to clarify differences.

5. Can I dispute an EOB?

Yes, if you find errors or incorrect claim decisions.

Final Thoughts

Mastering health insurance reading your EOB is essential for avoiding billing surprises and understanding your true healthcare costs. While insurance documents can seem complicated, once you understand the structure, everything becomes much clearer.

Always review your EOB carefully and compare it with your provider’s bill to ensure accuracy.

For more helpful insurance insights, visit:

Quotemaestro Insurance Guides

And explore related funding structures here:

Level Funded vs True Self-Funded Insurance Guide

Level Funded vs True Self-Funded Insurance Guide

[cta_alert id=”3105″]