Open enrollment is one of the most important times of the year for anyone with health insurance. Yet many people rush through it without fully understanding their options, which can lead to higher costs or poor coverage choices.

That’s why having a clear open enrollment health insurance guide is essential in 2026.

During open enrollment, you have a limited window to sign up for, change, or update your health insurance plan. Once the deadline passes, you usually have to wait until the next year unless you qualify for a special enrollment period.

In this guide, we’ll explain everything you need to know about open enrollment, how to choose the right plan, and how to avoid costly mistakes.

[cta_alert id=”3100″]

What Is Open Enrollment?

To understand the open enrollment health insurance guide, you first need to know what open enrollment means.

Open enrollment is a fixed time period when you can:

- Enroll in a new health insurance plan

- Switch existing plans

- Add or remove dependents

- Update coverage details

Outside this period, changes are usually not allowed unless you experience a qualifying life event.

Why Open Enrollment Matters

Open enrollment is your yearly opportunity to review and improve your health coverage.

A strong open enrollment health insurance guide should highlight that this is the only time most people can make changes without restrictions.

Missing this window may result in:

- Being locked into a costly plan

- Losing access to preferred doctors

- Higher out-of-pocket expenses

When Does Open Enrollment Happen?

Open enrollment dates vary depending on your insurance type:

- Employer plans: usually fall (Oct–Dec)

- Marketplace plans: typically Nov–Jan (varies by country/state)

Marking these dates is essential for following any open enrollment health insurance guide properly.

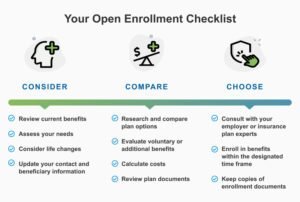

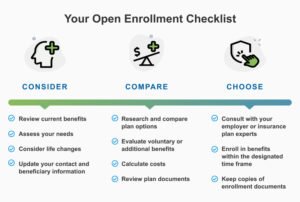

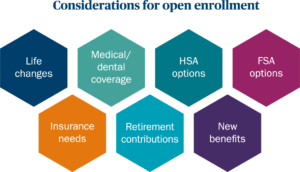

What You Can Change During Open Enrollment

During this period, you can:

- Switch from HMO to PPO or EPO

- Change deductible levels

- Add family members

- Update prescriptions coverage

- Adjust coverage tiers

Understanding these options is key to making the most of open enrollment.

How to Choose the Right Plan

When using an open enrollment health insurance guide, consider:

- Monthly premiums

- Deductibles

- Provider networks

- Prescription coverage

- Out-of-pocket maximums

Choosing the wrong plan can cost you significantly more over the year.

Common Mistakes People Make

Many people rush through open enrollment and make costly mistakes:

- Choosing only based on premium price

- Ignoring provider networks

- Not checking medication coverage

- Missing deadlines

- Not comparing plan options

Avoiding these mistakes is a core part of any good open enrollment health insurance guide.

Understanding Rising Health Insurance Costs

Healthcare costs continue to increase, making plan selection even more important.

Learn more about rising costs here: 2026 Health Insurance Premium Hikes.

These increases make it more important to carefully review options during open enrollment.

Employer vs Marketplace Open Enrollment

You may get insurance through:

Employer Plans

- Offered through your job

- Employer may pay part of premium

Marketplace Plans

- Purchased individually

- Based on income eligibility

Both options require careful review during open enrollment.

How to Compare Plans Effectively

A proper open enrollment health insurance guide should include comparison tips:

- Total yearly cost (not just monthly premium)

- Doctor and hospital networks

- Prescription drug coverage

- Specialist access

- Emergency care coverage

[cta_alert id=”3103″]

Why Reviewing Plans Every Year Is Important

Even if you’re happy with your current plan, reviewing options annually is essential.

Healthcare costs and coverage rules change every year.

See updated trends here: 2026 Health Insurance Premium Hikes.

Special Enrollment Exceptions

Outside open enrollment, you may still qualify for changes if you experience:

- Marriage or divorce

- Birth of a child

- Job change

- Loss of coverage

- Relocation

These are called qualifying life events.

How to Avoid Overpaying for Insurance

To avoid overpaying:

- Compare multiple plans

- Check provider networks

- Review drug coverage

- Estimate yearly medical usage

This is a key step in any open enrollment health insurance guide.

What Happens If You Miss Open Enrollment?

If you miss the deadline:

- You may be stuck with your current plan

- You may lose coverage options

- You may need to wait until next year

That’s why planning ahead is so important.

Rising Premiums and Your Decision

Increasing premiums are forcing many people to rethink coverage choices.

Learn more here: 2026 Health Insurance Premium Hikes.

Understanding cost trends helps you choose smarter during open enrollment.

Tips to Prepare for Open Enrollment

Before enrollment begins:

- Review last year’s medical usage

- List your preferred doctors

- Check prescriptions

- Compare plan summaries

- Set a decision deadline

Preparation makes the process much easier.

Final Thoughts

A strong open enrollment health insurance guide helps you make smarter, more informed decisions about your healthcare coverage.

Open enrollment is your yearly opportunity to improve your plan, reduce costs, and ensure better access to care.

With rising healthcare expenses in 2026, taking time to compare options carefully is more important than ever.

[cta_alert id=”3105″]

FAQs About Open Enrollment Health Insurance Guide

What is open enrollment?

It is a limited time period when you can enroll in or change your health insurance plan.

What happens if I miss open enrollment?

You usually must wait until the next year unless you qualify for a special enrollment event.

Can I change my plan anytime?

No, only during open enrollment or qualifying life events.

Why is open enrollment important?

It allows you to update coverage, reduce costs, and improve benefits.

What should I compare during open enrollment?

Premiums, deductibles, networks, prescriptions, and total yearly costs.

Why are premiums increasing in 2026?

Rising healthcare costs and inflation are driving higher insurance premiums.