Spouse life insurance is life insurance coverage on your husband or wife, designed to protect your household if that person dies. It can replace income, cover debts, and fund essential costs that would otherwise fall on the surviving partner.

It also helps protect the value of unpaid work such as childcare, caregiving, home management, and coordination of family logistics. When it is structured well, it reduces financial shock during a time when decision-making is hardest.

What Spouse Life Insurance Means?

Spouse life insurance refers to a policy where the insured is your spouse and the benefit is paid to a beneficiary, often you. The goal is not only to replace a paycheck, but to preserve the household’s ability to function financially.

Coverage can be purchased as an individual policy on your spouse or as an optional rider attached to your own life insurance. The best structure depends on the amount of coverage needed, the term length, and whether long-term flexibility matters.

How Spouse Coverage Works?

Life insurance pays a death benefit when the insured person dies and the claim is approved. With spouse coverage, the insured is your spouse, and you typically name yourself or a trust as the beneficiary.

Premiums are based on age, health, coverage amount, and policy type. The insurer may require an application, health questions, and sometimes a medical exam for larger policies.

Policy Ownership and Beneficiary Details

Usually, the person paying for the policy is also the owner, which allows them to control beneficiaries and make changes. Ownership matters when marriages change, when estate planning becomes more complex, or when you want to ensure the benefit is protected for children.

Beneficiary designations should be reviewed after major life events. A small update now can prevent delays, disputes, and unintended payouts later.

Types of Spouse Life Insurance

Spouse coverage can be term life, permanent life, or a rider. Each option fits a different planning need and budget.

The right type is usually the one that covers the risk for the period you actually need protection. Cost, simplicity, and long-term flexibility should all be weighed.

Term Life Insurance For a Spouse

Term life covers a set period such as 10, 20, or 30 years. It is often the most affordable way to buy a higher death benefit during the years when financial responsibilities are highest.

This option tends to work well when you want coverage until children are grown, a mortgage is paid down, or retirement savings are built. It can also be a clean fit for a single major risk window.

Permanent Life Insurance For a Spouse

Permanent life, such as whole life or universal life, can last for life if premiums are kept current. It often includes cash value, which can grow over time depending on the policy design and performance.

This option can make sense when the need for coverage does not end, such as long-term dependent care, estate planning, or leaving a legacy. It is usually more expensive than term for the same death benefit.

Spouse Term Rider Versus Separate Policy

A spouse rider adds limited term coverage on your spouse to your own policy. It can be convenient and low-cost, but it often has lower maximum coverage amounts and fewer customization options.

A separate policy may cost more, yet it gives stronger control over term length, conversion features, and future adjustments. It can also be easier to keep if you change your own coverage later.

When Spouse Life Insurance Makes Sense?

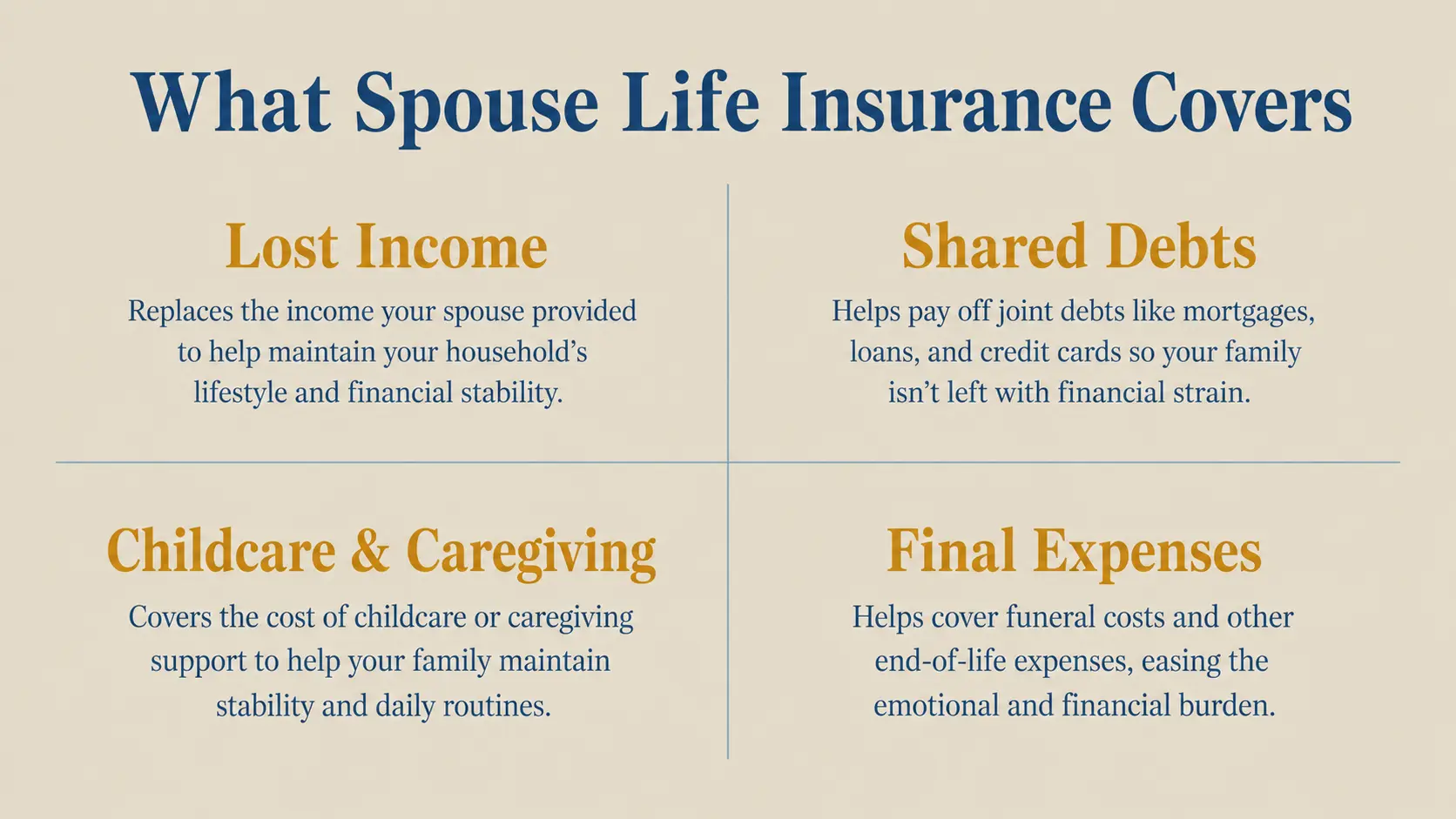

Spouse life insurance makes sense when your household would face real financial strain after your spouse’s death. That strain can come from lost income, new expenses, or the need to replace essential services.

It also makes sense when you want to protect long-term goals, including paying off debt, keeping a home, or funding education. A clear need often becomes obvious once you list what the surviving spouse would have to pay for alone.

When Your Spouse Earns Income?

If your spouse provides income, the surviving spouse may need time to adjust, pay bills, and maintain savings contributions. Coverage can act as a bridge that keeps the household stable while new plans are made.

Income replacement is not only about paychecks. It also covers employer benefits that may end, such as health insurance subsidies or retirement matches.

When Your Spouse Does Unpaid But Essential Work?

A non-working or lower-earning spouse often performs work that still has a market cost. Childcare, transportation, meal planning, eldercare coordination, and home management can be expensive to replace quickly.

Coverage can fund those replacements, allowing the surviving spouse to keep working, avoid burnout, and prevent rushed decisions that cost more over time.

When You Share Debt and Long-Term Commitments?

Mortgages, auto loans, business loans, and personal loans do not disappear simply because one spouse dies. Some debts may be joint, some may be secured by property, and some may be tied to a co-signer.

A death benefit can prevent forced asset sales and protect credit. It can also keep the surviving spouse from draining emergency savings and retirement accounts.

When Children or Dependents Rely On Both of You?

Families with children often need coverage on both parents, even if one parent earns less. The cost of care, tutoring, therapy, and daily supervision can rise sharply after a loss.

If you support an adult child with special needs or an aging parent, the need may last longer than a typical child-raising timeline. In those cases, longer-term or permanent coverage can be worth evaluating.

When Spouse Life Insurance May Not Be Necessary?

Not every household needs a separate policy right away. If your spouse has significant independent assets, minimal financial obligations, and no dependents, the impact of a loss may be manageable without insurance.

It may also be less necessary when you have ample liquid savings, strong survivor benefits from a pension, or existing life insurance that already covers the household’s full needs. Even then, a quick needs review is still wise, since goals change.

How Much Coverage To Consider?

The best coverage amount is driven by obligations, income needs, and the cost to replace services. Many families start by estimating how long they would need support and what expenses would increase after a loss.

Focus on the gap between what you would need and what you already have. Assets, existing insurance, and expected survivor benefits should be counted so you do not overpay for coverage you do not need.

- Income gap: Estimate the after-tax income needed to keep core bills paid and savings on track.

- Debt payoff goals: Consider whether you want the benefit to clear the mortgage, loans, or credit balances.

- Child and dependent costs: Add childcare, after-school care, caregiving help, and health-related support.

- Final expenses: Plan for funeral and immediate administrative costs that often arrive quickly.

- Time to reset: Build in a buffer for grief time, job changes, or relocation decisions.

Once you have those inputs, you can match a policy term and amount to the period of greatest risk. Keeping the plan simple often leads to better follow-through.

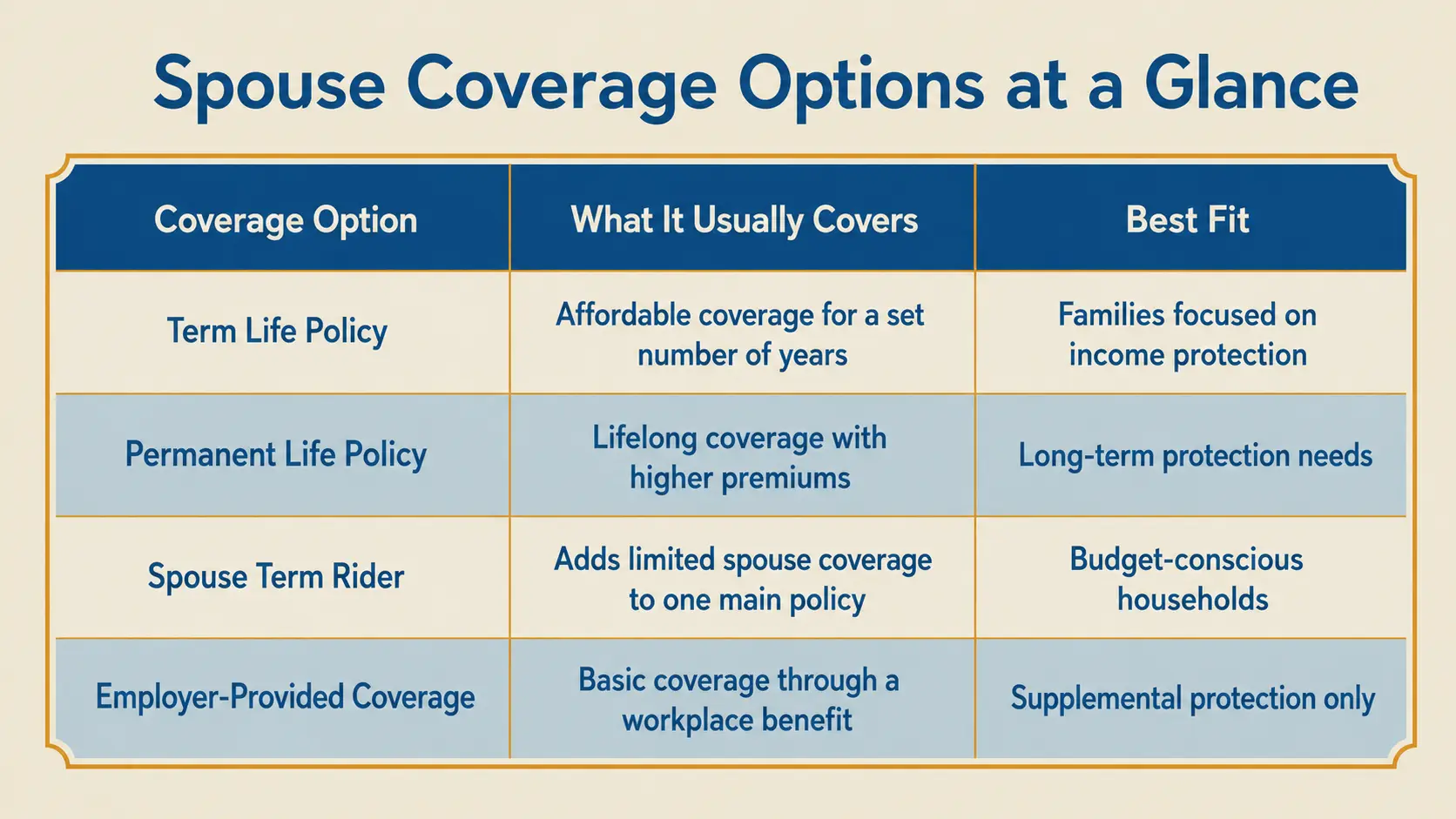

Key Differences Between Spouse Coverage Options

Comparing options side by side helps you see tradeoffs in cost, flexibility, and control. Use the table as a planning tool, not a final decision, since pricing and features vary by insurer.

| Coverage Option | Best Fit | Primary Tradeoff |

|---|---|---|

| Term Life Policy On Spouse | High needs for a defined period | Coverage ends unless renewed or converted |

| Permanent Life Policy On Spouse | Long-lasting needs and legacy planning | Higher premiums for the same death benefit |

| Spouse Term Rider | Simple, low-cost add-on coverage | Lower limits and fewer customization options |

| Employer-Provided Spouse Coverage | Basic coverage while employed | May end with job changes and may be limited |

What To Look For In a Good Policy?

Start with insurers that have strong financial ratings and clear claims processes. Reliability matters more than small price differences when your family is counting on a payout.

Then review the policy’s design features. The right features reduce the chance you will need to replace coverage later at a worse health rating.

- Conversion option: Allows term coverage to convert to permanent coverage without a new medical exam, within stated limits.

- Level premiums: Keeps costs predictable for the chosen term period.

- Riders that match real needs: Consider only those that clearly improve protection, such as waiver of premium in specific situations.

- Clear exclusions and definitions: Know how the policy treats contestability periods, suicide clauses, and claim documentation.

A policy that is easy to understand is usually easier to keep in force. Simplicity is a practical advantage, not a compromise.

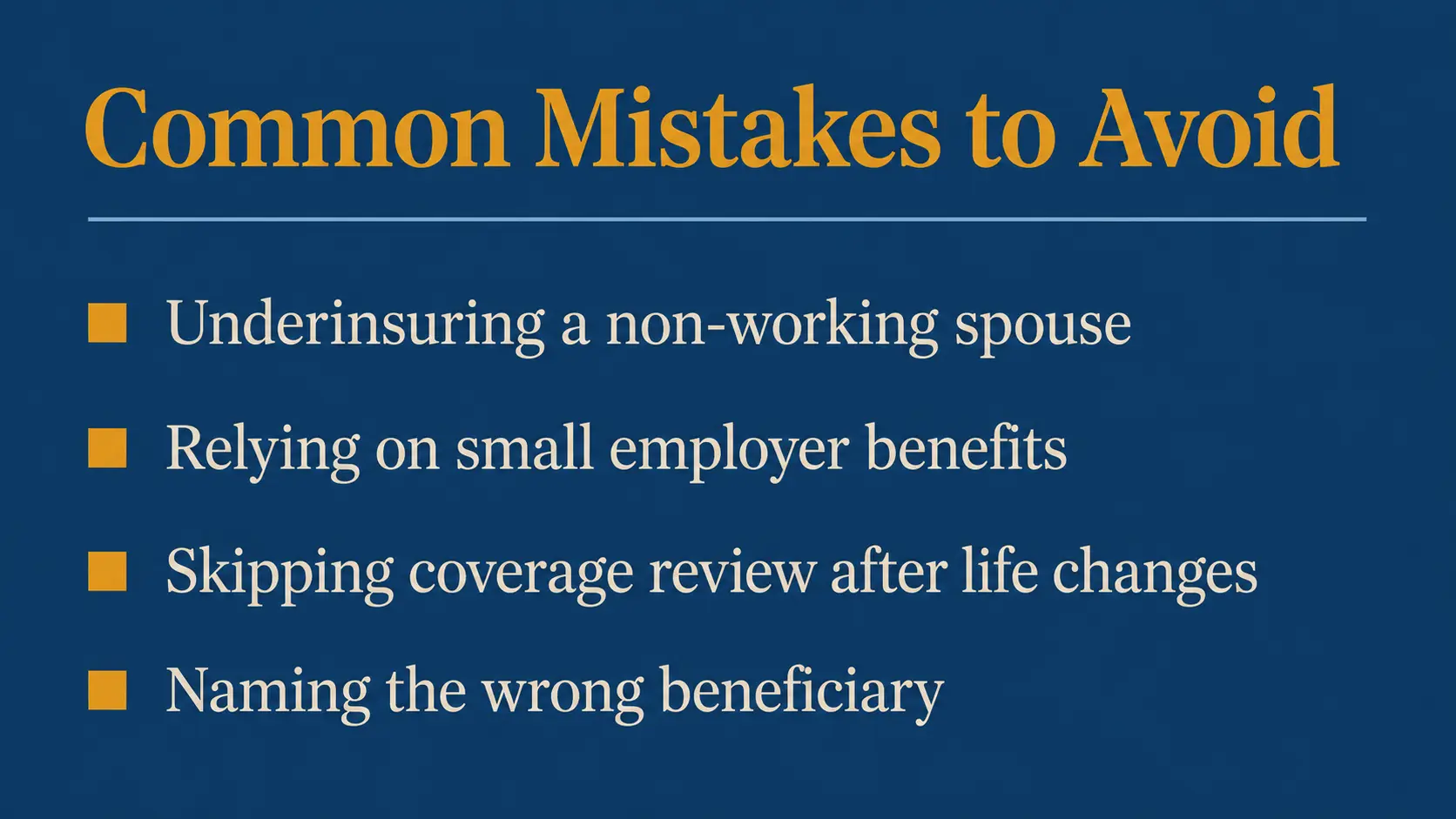

Common Mistakes To Avoid

Many households underinsure a non-working spouse because the value of their work is not visible on a pay stub. Others rely on a small employer benefit that would not cover more than a few months of expenses.

Another frequent issue is buying coverage without aligning it to the timeline of financial risk. A term that ends too early can leave you exposed when you still have a mortgage, dependents, or a single income.

- Skipping coverage review after life changes: Marriage, a new child, a home purchase, or a new job should trigger a checkup.

- Naming the wrong beneficiary: Outdated designations can override a will and cause delays or disputes.

- Assuming joint life insurance is always better: Joint policies can be complex and may not fit needs when both spouses require protection.

- Choosing price over policy strength: A slightly cheaper premium is not worth it if the insurer or contract terms create uncertainty.

Correcting these issues typically costs less when done early. A short review can prevent long-term gaps.

Conclusion

Spouse life insurance protects a household against the financial impact of losing a partner, whether that partner earns income or provides essential unpaid work. It makes the most sense when debts, dependents, or daily responsibilities would strain the surviving spouse’s budget and stability.

Pick a coverage amount tied to real obligations and choose a policy type that matches how long the risk lasts. A simple, well-aligned plan is often the most effective way to protect your family’s future decisions.

FAQ’s

1. Do I need life insurance for my spouse if they do not earn income?

Yes, you may still need coverage. A non-working spouse often handles childcare, home management, transportation, and caregiving. If they pass away, replacing that work can become expensive.

2. Is a separate spouse life insurance policy better than a spouse rider?

A separate policy usually gives more control, higher coverage options, and better flexibility. A spouse rider can be cheaper and simple, but it may offer limited coverage and fewer options.

3. How much spouse life insurance should I consider?

The right amount depends on your income needs, debts, childcare costs, final expenses, and how long your family would need support. The goal is to cover the real financial gap your spouse would leave behind.