Healthcare costs continue rising in 2026, and many individuals and families are asking the same frustrating question:

“Why is my health insurance consuming such a large part of my income?”

If your monthly premiums, deductibles, and medical expenses are becoming difficult to manage, you are not alone. Millions of Americans are struggling with increasing healthcare costs while trying to maintain quality coverage.

That’s why understanding your 2026 health insurance affordability rights is more important than ever.

In some situations, federal laws and marketplace rules may provide financial protections, subsidy opportunities, or alternative coverage options that can reduce your healthcare burden.

This guide explains what counts as “unaffordable” health insurance, your legal protections, and what steps you can take if your coverage is becoming financially overwhelming.

What Does “Unaffordable” Health Insurance Mean in 2026?

Under federal healthcare guidelines, affordability is tied to how much of your household income goes toward health insurance premiums.

For many people researching 2026 health insurance affordability rights, the major concern is whether employer-sponsored coverage or marketplace plans exceed affordability thresholds.

If your health insurance costs consume a significant percentage of your income, you may qualify for:

- Marketplace subsidies

- Premium tax credits

- Alternative plan options

- Special enrollment opportunities

Affordability rules can change slightly each year based on federal adjustments and healthcare regulations.

Why So Many Families Are Struggling in 2026

Several factors are increasing healthcare costs nationwide.

These include:

- Rising hospital costs

- Expensive prescription drugs

- Chronic illness treatment expenses

- Increased insurance premiums

- Narrower provider networks

- Higher deductibles and copays

As a result, many middle-income families are discovering that their insurance costs now exceed what feels financially manageable.

This growing pressure is driving more interest in 2026 health insurance affordability rights.

Employer Coverage and the Affordability Test

One important part of 2026 health insurance affordability rights involves employer-sponsored health insurance.

In general, employer coverage is considered “affordable” if the employee’s premium contribution for self-only coverage stays below a federally determined percentage of household income.

If employer coverage exceeds affordability thresholds, employees may become eligible for marketplace subsidies instead.

This can significantly reduce monthly healthcare expenses for qualifying households.

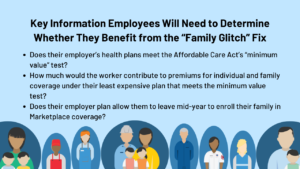

Understanding the “Family Glitch” Fix

In previous years, many families were blocked from receiving subsidies even when employer-sponsored family coverage was extremely expensive.

This issue became known as the “family glitch.”

Recent federal changes improved 2026 health insurance affordability rights by allowing some families to qualify for marketplace subsidies if family coverage through an employer is considered unaffordable.

This update may help many households lower monthly insurance costs dramatically.

What Legal Protections Do You Have?

Consumers have several important 2026 health insurance affordability rights under federal healthcare laws.

These protections may include:

- Access to ACA marketplace plans

- Protection against denial for pre-existing conditions

- Premium subsidy eligibility

- Coverage for preventive care

- Appeals for denied claims

- Annual open enrollment protections

Understanding these rights can help families avoid overpaying or remaining stuck in financially harmful coverage situations.

Can You Change Plans Mid-Year?

In some cases, yes.

Certain life events may trigger a Special Enrollment Period (SEP), allowing you to change coverage outside the normal enrollment window.

Qualifying events may include:

- Loss of employer coverage

- Marriage

- Divorce

- Birth of a child

- Moving to a new area

- Significant income changes

These protections are an important part of 2026 health insurance affordability rights because they provide flexibility during major life changes.

Marketplace Subsidies Can Reduce Monthly Costs

Many people assume they earn too much to qualify for healthcare subsidies.

However, because of updated affordability calculations and rising healthcare costs, more households may now qualify for assistance.

Subsidies can help reduce:

- Monthly premiums

- Deductibles

- Out-of-pocket costs

For families struggling with rising expenses, reviewing marketplace eligibility is one of the smartest ways to use 2026 health insurance affordability rights effectively.

How to Know If Your Plan Is Too Expensive

Your health plan may be financially problematic if:

- Premiums consume a large portion of monthly income

- Deductibles are difficult to afford

- You delay medical care due to cost

- Prescription expenses create financial strain

- Healthcare bills increase debt

Many consumers focus only on premiums, but total healthcare spending matters just as much.

Evaluating overall affordability is essential when reviewing 2026 health insurance affordability rights.

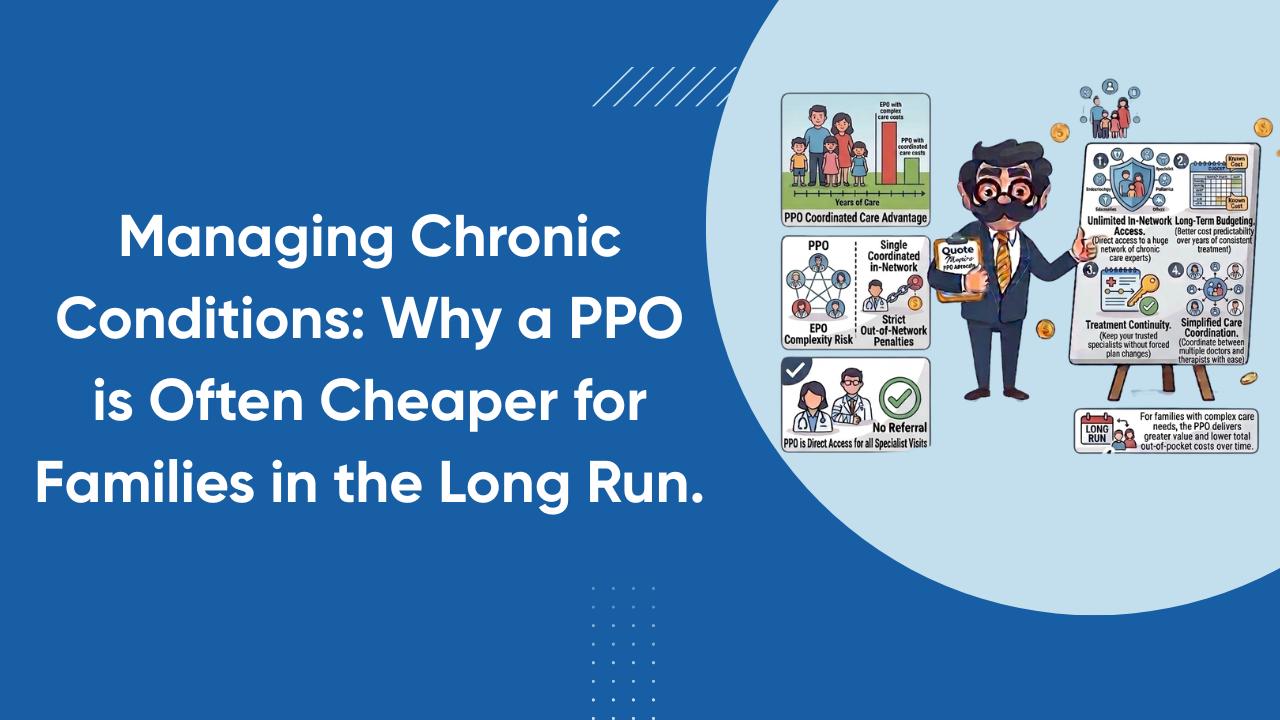

Comparing HMO, PPO, and EPO Plans in 2026

Different insurance plan types may help reduce costs depending on your healthcare needs.

HMO Plans

HMO plans often provide:

- Lower premiums

- Coordinated care

- Smaller provider networks

PPO Plans

PPO plans usually offer:

- Greater provider flexibility

- Easier specialist access

- Higher monthly premiums

EPO Plans

EPO plans combine:

- Lower costs than PPOs

- No referral requirements

- Moderate provider flexibility

Understanding these options can help families make smarter decisions while navigating 2026 health insurance affordability rights.

Why Reviewing Coverage Every Year Matters

Healthcare plans change constantly.

Premiums, provider networks, prescription formularies, and deductibles may all shift from year to year.

That’s why reviewing coverage annually is critical for maximizing your 2026 health insurance affordability rights.

Many families unknowingly stay enrolled in plans that no longer fit their financial or healthcare needs.

Comparing plans carefully each enrollment season can potentially save thousands of dollars annually.

Steps You Can Take Right Now

If healthcare costs feel overwhelming, consider these steps:

- Compare marketplace plans

- Check subsidy eligibility

- Review employer affordability rules

- Explore HSA-qualified plans

- Analyze total healthcare costs

- Verify provider networks

- Consult licensed insurance professionals

Small changes in coverage selection can create major long-term savings.

For more insurance comparisons and healthcare cost-saving guidance, visit Quote Maestro.

Final Thoughts

Rising healthcare costs are creating financial stress for millions of individuals and families in 2026.

Understanding your 2026 health insurance affordability rights can help you identify subsidy opportunities, compare smarter coverage options, and avoid paying more than necessary for healthcare.

Whether you receive employer coverage or purchase insurance independently, reviewing affordability protections and plan options carefully may help reduce both financial strain and long-term healthcare risks.

The right coverage decision can protect not only your health, but also your financial future.

FAQs About 2026 Health Insurance Affordability Rights

What are 2026 health insurance affordability rights?

These rights include protections related to healthcare affordability, marketplace subsidies, employer coverage rules, and access to ACA-compliant insurance plans.

What happens if my employer insurance is too expensive?

If employer coverage exceeds federal affordability thresholds, you may qualify for marketplace subsidies.

Can I get subsidies in 2026?

Possibly. Many households qualify for premium tax credits based on income and healthcare affordability calculations.

What is considered affordable health insurance in 2026?

Affordability depends on federal guidelines comparing premium costs to household income.

Can I change my health insurance plan outside open enrollment?

Yes, certain life events may trigger a Special Enrollment Period allowing mid-year plan changes.

Why should I compare plans every year?

Premiums, provider networks, and deductibles change frequently, so annual plan reviews may help reduce healthcare costs significantly.