For young professionals focused on building wealth, every financial decision matters. From investing early to reducing unnecessary expenses, smart money habits can create long-term financial freedom.

One strategy gaining attention is combining low-cost health insurance with tax-advantaged healthcare savings. That’s why many financially focused individuals are exploring the powerful combination of HMO and HSA benefits.

But is this setup really the ultimate wealth-building hack for healthy single professionals?

In many situations, the answer may be yes.

This guide explains how HMO plans and Health Savings Accounts (HSAs) work together, why they can save significant money over time, and who benefits most from this strategy.

Understanding HMO and HSA Benefits

Before deciding whether this strategy fits your lifestyle, it’s important to understand the basics of HMO and HSA benefits.

What Is an HMO?

A Health Maintenance Organization (HMO) plan is a type of health insurance that usually offers:

- Lower monthly premiums

- Lower out-of-pocket costs

- Coordinated care through a primary doctor

- Restricted provider networks

HMO plans are often attractive for healthy individuals who rarely need specialists or expensive treatments.What Is an HSA?

A Health Savings Account (HSA) is a tax-advantaged savings account used for qualified medical expenses.

HSAs allow you to:

- Contribute pre-tax money

- Grow savings tax-free

- Withdraw funds tax-free for medical expenses

Many financially savvy professionals use HSAs as both healthcare savings tools and long-term investment accounts.

Why Healthy Professionals Like HMO and HSA Benefits

Single healthy professionals often use fewer healthcare services than families or individuals with chronic conditions.

Because of that, many prioritize:

- Lower monthly insurance costs

- Tax savings

- Investment opportunities

- Long-term wealth growth

That’s where HMO and HSA benefits can become financially powerful.

Lower insurance premiums allow more money to stay invested or saved each month, while HSA contributions provide additional tax advantages.

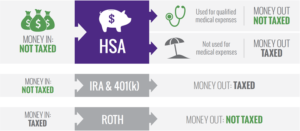

The Triple Tax Advantage of an HSA

One reason people love HMO and HSA benefits is the unique tax structure of HSAs.

An HSA offers three major tax advantages:

- Contributions are tax-deductible

- Investments grow tax-free

- Qualified withdrawals remain tax-free

Very few financial accounts receive all three tax benefits simultaneously.

Over time, consistent HSA investing can create a substantial healthcare fund while also supporting retirement planning.

Lower Monthly Premiums Can Accelerate Wealth Building

Many healthy professionals rarely visit doctors beyond annual checkups.

Choosing a lower-cost HMO plan may reduce monthly insurance expenses significantly compared to PPO options.

The savings from lower premiums can then be redirected toward:

- Retirement accounts

- Emergency funds

- Debt payoff

- Stock market investments

- HSA contributions

This is one of the main reasons financially focused individuals research HMO and HSA benefits as part of long-term wealth strategies.

HSA Investing Can Create Long-Term Financial Growth

Many people mistakenly treat HSAs like ordinary savings accounts.

However, many HSA providers allow investments in:

- Index funds

- Mutual funds

- ETFs

- Interest-bearing accounts

Healthy professionals who avoid frequent medical spending may allow HSA balances to grow for decades.

Some investors even use HSAs as supplemental retirement accounts because healthcare costs often increase later in life.

Who Benefits Most from HMO and HSA Benefits?

The combination of HMO and HSA benefits often works best for individuals who:

- Are generally healthy

- Rarely need specialists

- Want lower monthly premiums

- Prefer long-term investing

- Have emergency savings available

- Are focused on tax-efficient wealth building

For disciplined savers, this strategy can become a powerful financial tool.

Potential Downsides to Consider

Although HMO and HSA benefits can be attractive, this strategy is not perfect for everyone.

Possible disadvantages include:

- Limited doctor networks

- Referral requirements for specialists

- Higher deductibles on some plans

- Unexpected medical costs if health changes suddenly

Individuals with chronic illnesses or frequent specialist visits may prefer more flexible insurance options like PPO plans.

Healthcare needs can also change unexpectedly over time.

Emergency Savings Still Matter

Even with strong HMO and HSA benefits, healthy professionals should maintain emergency savings outside their HSA.

Unexpected situations like:

- Injuries

- Surgeries

- Job loss

- Major illnesses

can still create financial stress.

An HSA works best as part of a broader financial plan rather than a complete replacement for emergency funds.

Is an HMO + HSA Really a Wealth Hack?

For many single healthy professionals, the answer is yes.

The combination of lower insurance premiums, tax-free investment growth, and reduced healthcare spending can create long-term financial advantages.

However, success depends on:

- Staying disciplined financially

- Maintaining consistent HSA contributions

- Understanding plan limitations

- Choosing healthcare coverage carefully

The real power of HMO and HSA benefits comes from using healthcare savings strategically over many years.

How to Choose the Right Plan

Before selecting any health insurance plan, compare:

- Monthly premiums

- Deductibles

- HSA eligibility

- Provider networks

- Prescription coverage

- Maximum out-of-pocket costs

The cheapest plan is not always the smartest option if it creates problems accessing care later.

For more health insurance comparisons and financial planning resources, visit Quote Maestro.

Final Thoughts

The combination of HMO and HSA benefits can be a powerful wealth-building strategy for healthy single professionals focused on long-term financial growth.

Lower insurance premiums combined with tax-advantaged healthcare investing may help individuals save thousands of dollars over time while building future financial security.

Still, choosing the right plan depends on your personal healthcare needs, risk tolerance, and financial goals.

Understanding how to balance healthcare costs with wealth-building opportunities can help create smarter financial decisions for the future.

FAQs About HMO and HSA Benefits

Can you have an HSA with an HMO plan?

Yes, but only if the HMO is considered HSA-qualified and meets high-deductible health plan requirements.

Why are HMO and HSA benefits popular with young professionals?

Many healthy professionals prefer lower premiums and tax-saving investment opportunities that HSAs provide.

Is an HSA good for long-term investing?

Yes, HSAs offer tax-free growth and can become valuable long-term healthcare or retirement savings accounts.

Are HMO plans cheaper than PPO plans?

In many cases, HMO plans have lower monthly premiums and lower routine healthcare costs.

What happens to HSA money if unused?

Unused HSA funds roll over every year and remain yours permanently.

Are HMO and HSA benefits good for everyone?

No, individuals with chronic conditions or frequent specialist visits may need more flexible insurance coverage options.