Health insurance costs are rising again in 2026, leaving many middle-income Americans frustrated and financially stretched. While some households qualify for government subsidies and high earners can absorb higher costs more easily, millions of families fall into what experts often call the “missing middle.”

These households earn too much to receive large subsidy assistance but not enough to comfortably handle rising premiums, deductibles, and out-of-pocket expenses.

That’s why understanding 2026 health insurance premium hikes has become more important than ever.

This guide explains why premiums are increasing, how the “missing middle” is being affected, and which insurance strategies may help families reduce financial pressure while maintaining quality healthcare coverage.

Who Is the “Missing Middle”?

The “missing middle” generally refers to individuals and families who:

- Earn too much for major ACA subsidy support

- Do not receive strong employer-sponsored benefits

- Face rising healthcare costs without financial protection

- Struggle balancing premiums with daily living expenses

For many middle-income households, 2026 health insurance premium hikes are creating difficult choices between healthcare coverage and other financial priorities.

These families often include:

- Self-employed professionals

- Small business owners

- Freelancers and contractors

- Early retirees

- Middle-income families without corporate benefits

Why Are 2026 Health Insurance Premium Hikes Happening?

Several factors are driving 2026 health insurance premium hikes across the market.

Rising Medical Costs

Hospitals, prescription drugs, specialist care, and advanced treatments continue becoming more expensive every year.

Insurance companies adjust premiums to offset these rising healthcare expenses.

Increased Chronic Illness Claims

More Americans are managing chronic conditions such as:

- Diabetes

- Heart disease

- Obesity

- Mental health conditions

Long-term treatment costs contribute heavily to overall insurance spending.

Expensive Specialty Medications

New medications and specialty drug therapies can cost thousands of dollars monthly, significantly impacting insurer expenses.

Healthcare Worker Shortages

Provider shortages and staffing costs are also increasing operational healthcare expenses nationwide.

All of these factors contribute to ongoing 2026 health insurance premium hikes.

How the Missing Middle Is Affected Most

Lower-income households often receive subsidies that reduce premium increases.

Higher-income households may still afford more expensive plans.

The missing middle, however, frequently absorbs the full impact of 2026 health insurance premium hikes without major financial assistance.

This creates problems such as:

- Choosing lower-quality coverage

- Delaying medical care

- Avoiding specialist visits

- Skipping prescriptions

- Increasing personal debt

Many families now face difficult trade-offs between affordability and adequate healthcare access.

HMO Plans: Lower Premiums but More Restrictions

Many middle-income households consider HMO plans to reduce costs during 2026 health insurance premium hikes.

HMO plans usually offer:

- Lower monthly premiums

- Lower routine care costs

- Coordinated primary care

- Smaller provider networks

However, HMOs may also include:

- Referral requirements

- Limited out-of-state coverage

- Restricted specialist access

For healthy individuals who rarely travel or need specialists, HMOs may still provide strong value.

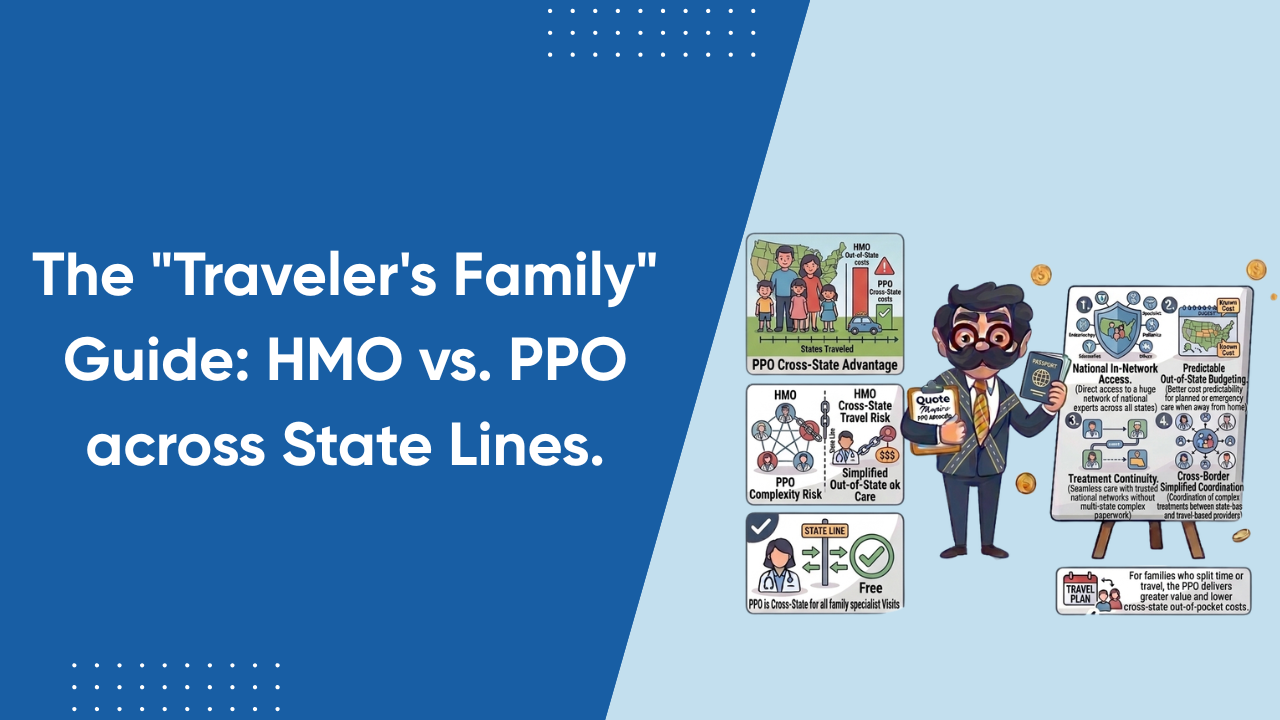

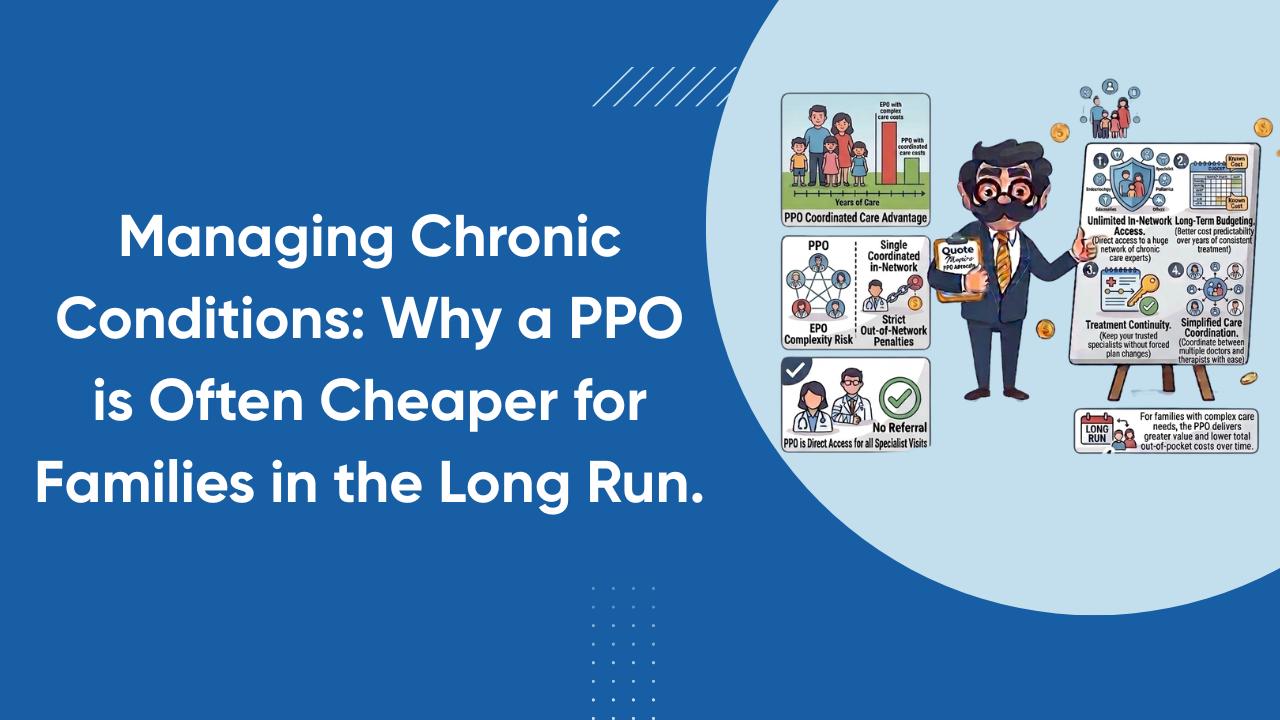

PPO Plans: Higher Cost but Greater Flexibility

PPO plans remain attractive despite rising costs because they provide:

- Larger provider networks

- Out-of-network flexibility

- Easier specialist access

- Better nationwide coverage

During periods of 2026 health insurance premium hikes, many families debate whether PPO flexibility justifies higher monthly premiums.

For people with chronic conditions, ongoing specialist needs, or college students living out of state, PPO plans may still offer better long-term value.

EPO Plans: The Growing Middle Ground

EPO plans are becoming increasingly popular during 2026 health insurance premium hikes because they balance affordability with flexibility.

EPO plans typically offer:

- Lower premiums than PPOs

- No referral requirements

- Moderate provider flexibility

- Simplified healthcare access

Many younger professionals and healthy families now see EPO plans as an attractive compromise between HMOs and PPOs.

High-Deductible Plans and HSA Strategies

Some middle-income earners are responding to 2026 health insurance premium hikes by choosing High-Deductible Health Plans (HDHPs) paired with Health Savings Accounts (HSAs).

This strategy may help lower monthly premiums while providing tax advantages.

HSAs offer:

- Tax-deductible contributions

- Tax-free growth

- Tax-free medical withdrawals

For healthy individuals with emergency savings, this approach can reduce immediate healthcare costs while building long-term financial protection.

Why Network Size Matters More in 2026

As insurers attempt to control costs, many are narrowing provider networks.

This means families affected by 2026 health insurance premium hikes should carefully review:

- Hospital access

- Specialist availability

- Prescription coverage

- Emergency care rules

- Out-of-state coverage

A cheaper plan may become far more expensive if your preferred doctors or hospitals are excluded.

How Families Can Reduce Healthcare Costs

Although 2026 health insurance premium hikes are challenging, there are ways to reduce financial pressure.

Compare Plans Every Year

Many families automatically renew plans without reviewing updated pricing or networks.

Comparing plans annually may uncover:

- Better premiums

- Lower deductibles

- Expanded provider networks

- Improved prescription coverage

Use Preventive Care

Preventive care helps reduce expensive future medical problems.

Consider Telehealth Options

Telemedicine services may reduce urgent care and specialist costs.

Maximize HSA Contributions

Tax-advantaged healthcare savings can improve long-term financial stability.

Choosing the Right Plan During Premium Increases

When evaluating plans during 2026 health insurance premium hikes, focus on total healthcare costs rather than monthly premiums alone.

Compare:

- Premiums

- Deductibles

- Copays

- Out-of-pocket maximums

- Specialist access

- Prescription coverage

The “cheapest” plan upfront may create larger expenses later if healthcare needs increase unexpectedly.

For more health insurance comparisons and cost-saving guidance, visit Quote Maestro.

Final Thoughts

The reality of 2026 health insurance premium hikes is creating growing pressure for middle-income households that already feel financially squeezed.

The “missing middle” faces unique challenges because many families earn too much for substantial subsidies yet still struggle with rising healthcare expenses.

Choosing the right insurance plan now requires balancing affordability, provider access, specialist flexibility, and long-term financial protection.

By carefully comparing HMO, PPO, EPO, and HDHP options, families can make smarter healthcare decisions while protecting both their health and financial future.

FAQs About 2026 Health Insurance Premium Hikes

Why are 2026 health insurance premium hikes happening?

Premiums are increasing due to rising medical costs, prescription drug expenses, chronic illness claims, and healthcare staffing shortages.

Who is most affected by 2026 health insurance premium hikes?

Middle-income households that receive limited subsidy assistance are often affected the most.

Are PPO plans still worth it in 2026?

For families needing specialist care or broader provider access, PPO plans may still provide valuable flexibility despite higher premiums.

Can EPO plans help reduce healthcare costs?

Yes, EPO plans often offer lower premiums than PPOs while still allowing direct specialist access.

How can families save money during premium hikes?

Comparing plans yearly, using preventive care, maximizing HSAs, and reviewing provider networks can help reduce healthcare costs.

What is the best insurance option for the missing middle?

The best plan depends on healthcare needs, budget, travel habits, and provider preferences. Many families now compare HMO, PPO, EPO, and HDHP options carefully before enrolling.