A premium increase can feel sudden, but it usually follows clear rules in your policy and the insurer’s pricing system. The reason depends on the type of life insurance you have, how long you have held it and what changed in your risk profile or the policy itself.

This guide breaks down the most common triggers, how to confirm the exact cause and which options typically reduce costs without creating coverage gaps. It also explains which increases are expected and which should be questioned.

Why Did My Life Insurance Premium Go Up?

Life insurance premiums go up for three broad reasons. The first is built into the policy design, especially with term policies that renew at higher ages and with permanent policies that have rising internal costs.

The second is a change in you or your policy, such as tobacco use, billing changes, missed payments, added riders, or a coverage adjustment. The third is a company level change allowed by the contract, most often in universal life products where rates can be adjusted within stated limits.

Start With Your Policy Type

Premium behavior is strongly tied to the policy category. A level term policy generally stays the same during the level period, while other types can increase as you age or as internal costs rise.

If you are unsure what you own, your annual statement and the declarations page typically list the type and the premium schedule. Knowing the type often explains most of the change on its own.

Term Life With Level Premiums

With level term, the premium is designed to stay flat for a set period, often 10, 20, or 30 years. If your increase happened within that level period, it may be tied to a billing issue, a lapse and reinstatement, or a policy change rather than age.

If the level period ended, the premium can jump sharply because renewal rates are based on your current age. That increase is usually expected and described in the renewal notice.

Term Life With Annual Renewable Term

Annual renewable term typically increases each year because the cost of insurance rises with age. The policy is priced with that upward schedule from the beginning.

If the increase seems larger than prior years, confirm whether the policy moved into a new age band or whether fees and riders changed.

Whole Life

Traditional whole life usually has fixed premiums, so a true premium increase is less common. What can feel like a premium increase is a change in how dividends are applied or a switch in payment method that changes the amount due.

If you use dividends to offset premiums, lower dividends can lead to higher out of pocket payments even when the base premium is unchanged.

Universal Life and Indexed Universal Life

Universal life policies separate what you pay from the actual monthly charges. The insurer deducts the cost of insurance and expenses from your cash value and those deductions can rise as you age.

If cash value is not keeping up, the policy may require higher payments to stay in force. Some universal life contracts also allow changes to certain rates or charges within limits, which can affect how much you must contribute.

Variable Universal Life

Variable universal life adds investment performance risk to the universal life structure. Poor subaccount performance can reduce cash value, which can force higher premiums to prevent lapse.

Premium pressure here can be driven by market volatility and by the same increasing insurance charges that affect other universal life policies.

Age Related Increases and Renewal Pricing

Age is the most common driver of higher costs when a term policy renews or when a policy has annually increasing charges. Even if your health is excellent, the probability of a claim rises with age and pricing reflects that.

Some products use age bands, so the increase may appear in larger jumps rather than smooth yearly changes. Your renewal schedule or illustration can show when those bands occur.

Health and Underwriting Changes That Can Raise Costs

Most level term policies do not reprice due to new health issues during the level period. However, health can matter if you applied for a policy change, reinstated after a lapse, or converted to a new product requiring underwriting.

Medical conditions, new medications, changes in build, or an updated family history can affect your classification. A move from preferred to standard, or a new table rating, can raise the required premium.

Tobacco Status and Nicotine Related Repricing

Tobacco and nicotine use can increase premiums significantly and the effect can appear after underwriting events such as reinstatement or policy replacement. Some insurers treat vaping and nicotine replacement products differently, so classification can vary.

If your billing indicates a tobacco rate and you believe it is incorrect, request the underwriting notes and confirm what was reported. Corrections typically require documentation and sometimes a new exam.

Lapse, Grace Period Issues and Reinstatement Costs

Missed payments can trigger late fees, coverage termination, or reinstatement requirements. Reinstatement may involve back premiums plus interest and it can also involve new underwriting.

Even without formal reinstatement, switching from annual to monthly billing can increase the total you pay over the year due to modal factors. Confirm whether the change is a true rate increase or a payment frequency effect.

Policy Changes That Increase The Amount Due

Premiums can rise if you increased the death benefit, extended the term period, or added riders. Waiver of premium, child term, accidental death and chronic illness riders can all change the total cost.

Some changes also affect how long the premium is guaranteed or whether the policy remains within a guaranteed premium schedule. Always review the updated illustration after any policy change.

Universal Life Cash Value Performance and Cost of Insurance Charges

With universal life, the question is often not whether the premium went up, but whether the required funding level increased to keep the policy active. Rising cost of insurance charges, policy fees and insufficient crediting can drain cash value over time.

Indexed and variable versions can add performance variability, which can widen the gap between what you are paying and what the policy needs. Monitoring statements and in-force illustrations helps you see issues early.

Company Level Adjustments and Contract Limits

Some policies allow the insurer to adjust certain charges, often within maximum rates stated in the contract. These changes are more common in flexible premium products and are usually communicated in writing.

If you receive a notice referencing changes to cost of insurance rates or expense loads, verify the effective date and the contract provisions that permit the adjustment.

Billing and Administrative Reasons That Look Like a Premium Increase

Not every higher bill is a pricing change. Common causes include switching payment modes, losing a discount for electronic funds transfer, or paying a past due balance that makes one month look unusually high.

Also check whether you accidentally paid for multiple policies, duplicated riders, or a new supplemental benefit. A quick call to confirm the itemized billing breakdown can resolve many surprises.

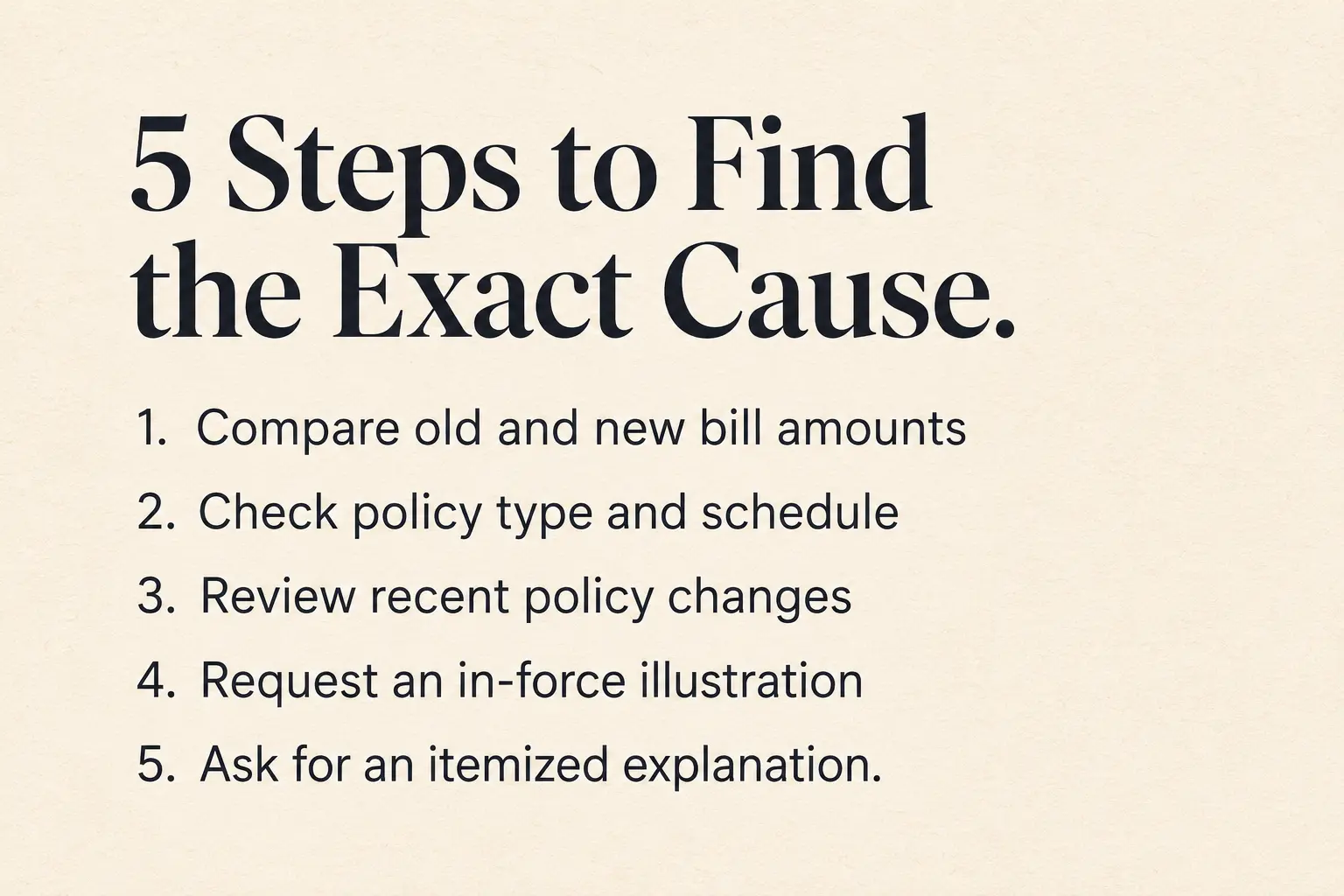

How to Confirm The Exact Reason Quickly?

You can usually pinpoint the cause with a few documents and a short checklist. Start with the most recent bill, the policy page showing your current premium and the annual statement.

- Compare the old and new amounts. Note the effective date and whether the change is permanent or limited to one billing cycle.

- Check the policy type and schedule. Look for level term end dates, renewal tables, or cost of insurance charges on universal life statements.

- Review recent policy changes. Confirm any rider additions, benefit increases, or billing mode changes that occurred around the same time.

- Request an in-force illustration. This shows how long the policy is projected to last at your current funding and crediting assumptions.

- Ask for an itemized explanation. Insist on a breakdown of premium, fees and charges and keep the response for your records.

Once you know the driver, you can evaluate the best fix instead of guessing.

Common Causes and What to do Next

The table below summarizes typical triggers and practical next actions. Use it as a quick reference before you request changes or cancel coverage.

| What Changed | Why it Raises Your Cost | Best Next Action |

|---|---|---|

| Term renewal after level period | Renewal pricing is based on older age and higher claim probability | Shop new term quotes and compare to conversion options |

| Universal life cash value falling | Monthly charges rise and cash value no longer subsidizes the policy | Request an in-force illustration and adjust funding or benefits |

| Billing mode changed to monthly | Modal factors can increase the total paid over the year | Ask for annual or semiannual pricing and autopay discounts |

| Rider added or benefit increased | Additional benefits add risk and administrative costs | Reassess rider value and confirm the updated illustration |

This overview helps you separate expected increases from avoidable ones.

Ways to Lower Your Premium Without Losing Protection

Not every solution requires canceling your policy. The right option depends on whether your policy is term or permanent and whether your health has improved since you bought it.

- Request a new underwriting review. If your health or build improved, a new policy may qualify at a better rate class.

- Adjust the death benefit thoughtfully. A lower benefit can cut cost, but confirm it still covers debts, income needs and final expenses.

- Extend the level period strategically. Replacing a renewing term policy with a new level term can stabilize payments if you still qualify.

- Review and remove low value riders. Dropping optional riders can reduce cost while keeping core coverage intact.

- For universal life, set a sustainable funding level. Funding to the level needed to carry the policy can prevent repeated increases later.

Before you make changes, confirm whether your policy has surrender charges, conversion privileges, or contestability implications tied to replacement.

When a Premium Increase is a Red Flag

An increase deserves extra scrutiny when it conflicts with what you were promised in writing. This is especially important for policies sold as having guaranteed level premiums or guaranteed no lapse features.

Watch for mismatches between your bill and your contract terms, unexpected classification changes, or vague explanations that do not cite policy provisions. If the explanation is unclear, request it in writing and ask for the exact contract language supporting the change.

Conclusion

A life insurance premium can go up due to renewal pricing, rising internal charges, policy changes, or billing and payment issues. The fastest way to get clarity is to identify your policy type, compare statements and request an itemized explanation or in-force illustration.

Once the cause is confirmed, you can often reduce costs by adjusting benefits, requalifying for better rates, changing billing modes, or funding a universal life policy more consistently. Avoid canceling coverage before you know the lapse and replacement consequences.