Life insurance is meant to replace what your family would lose financially if you were not there. The right amount is personal, but the decision gets easier when you separate needs from nice-to-haves. This guide breaks coverage down into simple parts so you can choose a number you can defend.

The goal is not to buy the biggest policy available. It is to buy enough to protect dependents, cover obligations and fund key goals without paying for coverage you do not need. A clear method also makes it easier to review coverage over time.

What Life Insurance is Meant to Cover?

Most people buy life insurance to protect others from a sudden income gap. It can also keep a household stable by paying off debts and funding near-term expenses. Thinking in categories prevents missed items and reduces guesswork.

Coverage is commonly used for income replacement, debt payoff, education goals and final expenses. It may also support business needs or caregiving plans. Your priorities determine how far coverage should go and how long it needs to last.

- Income needs: Ongoing bills such as housing, food, childcare and health insurance.

- Debt and obligations: Mortgage balance, auto loans, personal loans and any co-signed debt.

- Milestones and goals: College funding, a surviving spouse retirement bridge and relocation costs.

- End-of-life costs: Funeral, medical bills and estate settlement expenses.

Once you know what the policy should accomplish, you can estimate an amount that fits your household and budget.

Key Inputs That Change The Coverage Amount

Two households with the same income can need very different life insurance. Dependents, debt, savings and support from a partner all change the picture. Collecting a few numbers first saves time later.

Start with monthly spending that must continue, then list one-time obligations. Add future goals that matter to you and subtract resources that would still be available. The result is a coverage range, not a single perfect number.

- Number and ages of dependents: Younger children typically mean a longer protection window.

- Household income mix: Single-income households often need more replacement coverage.

- Debt structure: Large mortgage balances and private student loans raise the need.

- Existing assets: Cash reserves, retirement accounts and taxable investments can reduce required coverage.

- Work benefits: Employer life insurance can help, but it may not be portable after job changes.

With these inputs, you can choose a calculation method that fits your comfort level.

Common Rules of Thumb and Their Limits

Rules of thumb are popular because they are quick. They are also easy to misuse if you ignore debt, childcare costs, or a partner’s earning ability. Use them to set an initial range, then refine with your real numbers.

Multiples of income are the most common approach, but they do not account for spending patterns. Another shortcut is to aim for a policy that pays off the mortgage and replaces several years of income. These can be good starting points when you do not have time for a full breakdown.

- Income multiple approach: Picks a multiple of annual income, then adjusts for children and debts.

- Mortgage plus income approach: Covers the home loan and adds a set number of income years.

- Minimum coverage approach: Focuses on final expenses and urgent debts when budgets are tight.

Shortcuts are helpful early on, but a detailed estimate gives you more confidence and usually avoids overbuying.

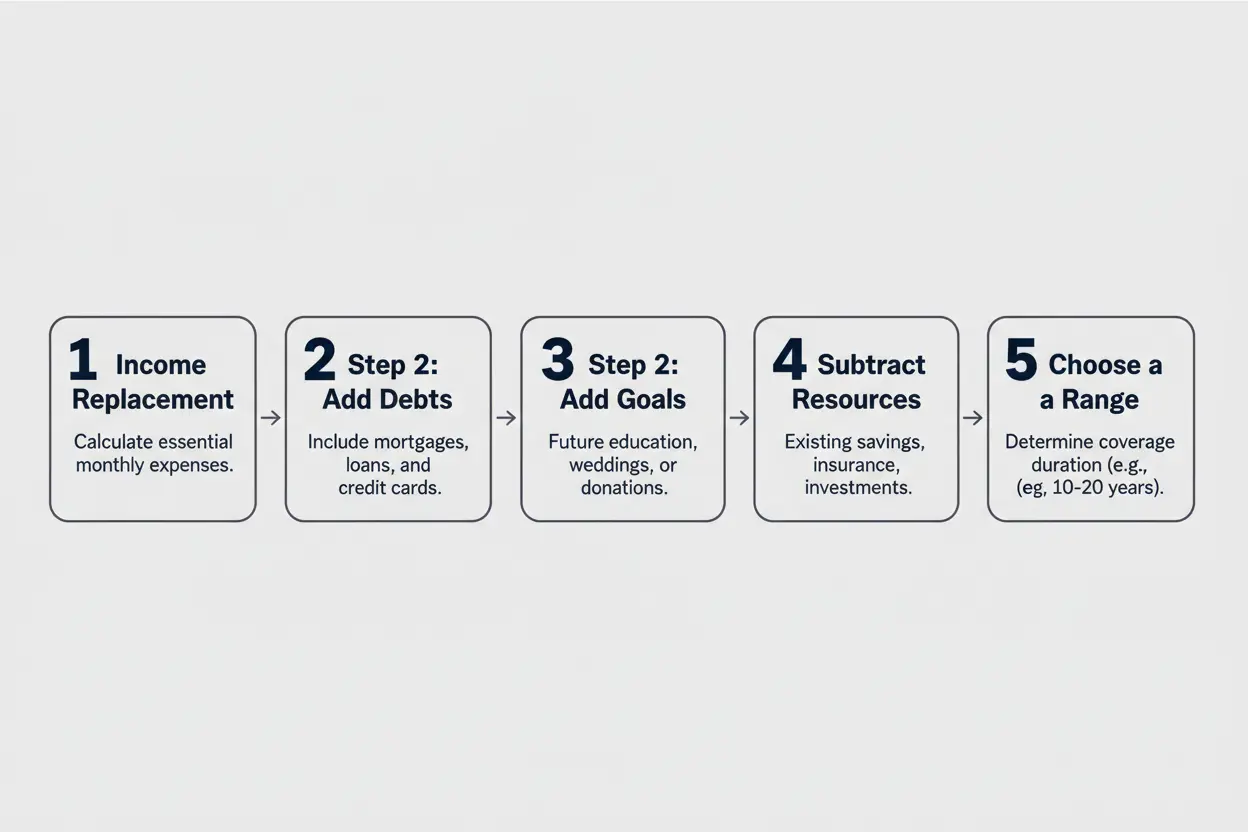

A Practical Way to Calculate Your Coverage

A solid method adds what must be funded and subtracts what is already available. This mirrors how a financial planner would frame the question. It also produces a number you can explain to a spouse or adviser.

Use annual spending for needs that should continue and one-time totals for items that should be paid off. Then reduce the total by savings and other resources. If you are unsure about a number, use a conservative range rather than a single point.

- Estimate ongoing income replacement. Multiply the yearly amount your household would need by the number of years support is required.

- Add one-time obligations. Include mortgage payoff, other debts, childcare transition costs and final expenses.

- Add goal funding. Include education goals or a retirement bridge if you want the surviving spouse to keep saving.

- Subtract available resources. Deduct liquid savings, investment accounts you expect to use and any existing life insurance.

- Choose a coverage range. Round to a level that matches policy options and your premium comfort.

After you have the range, term length and policy type become the next decision.

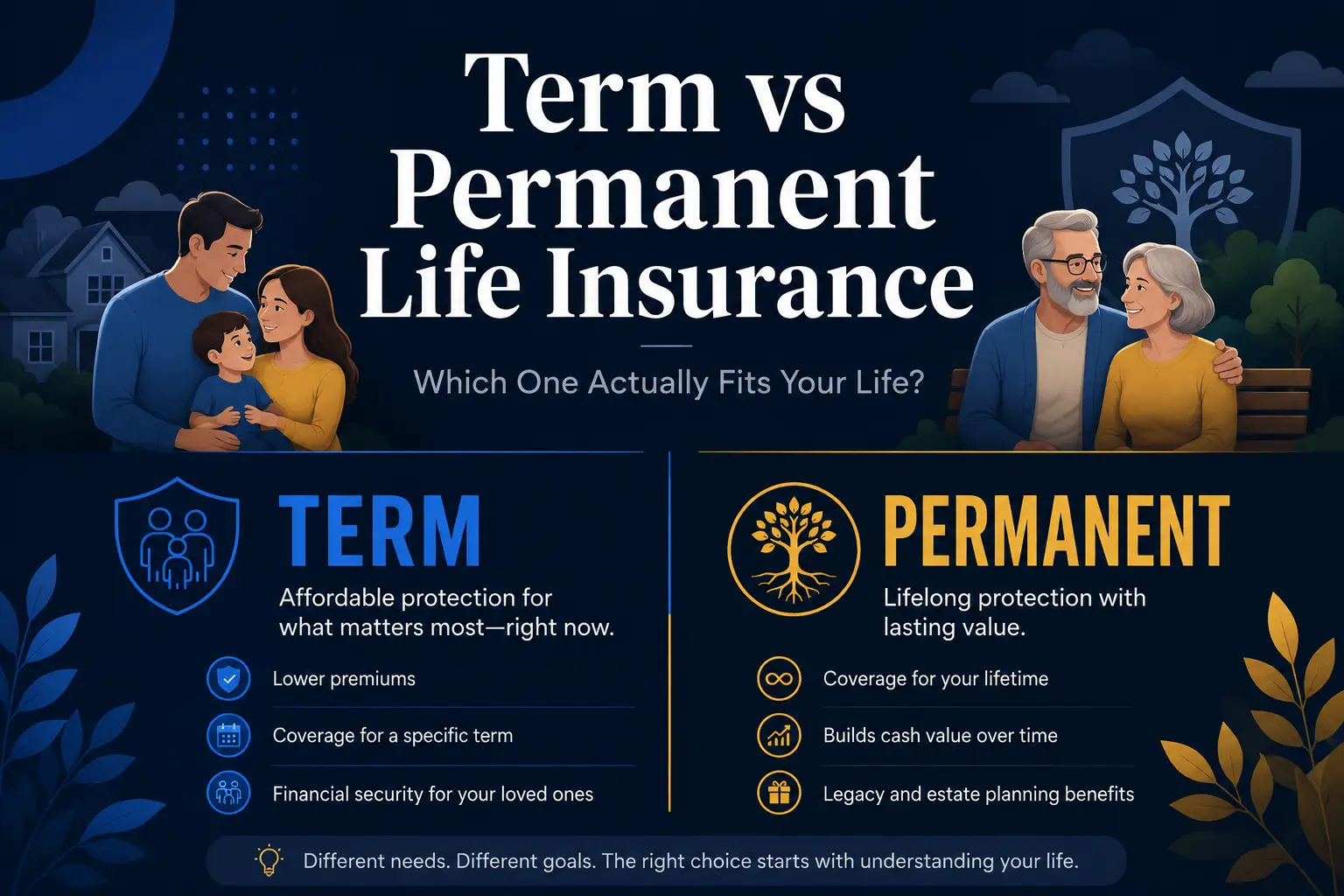

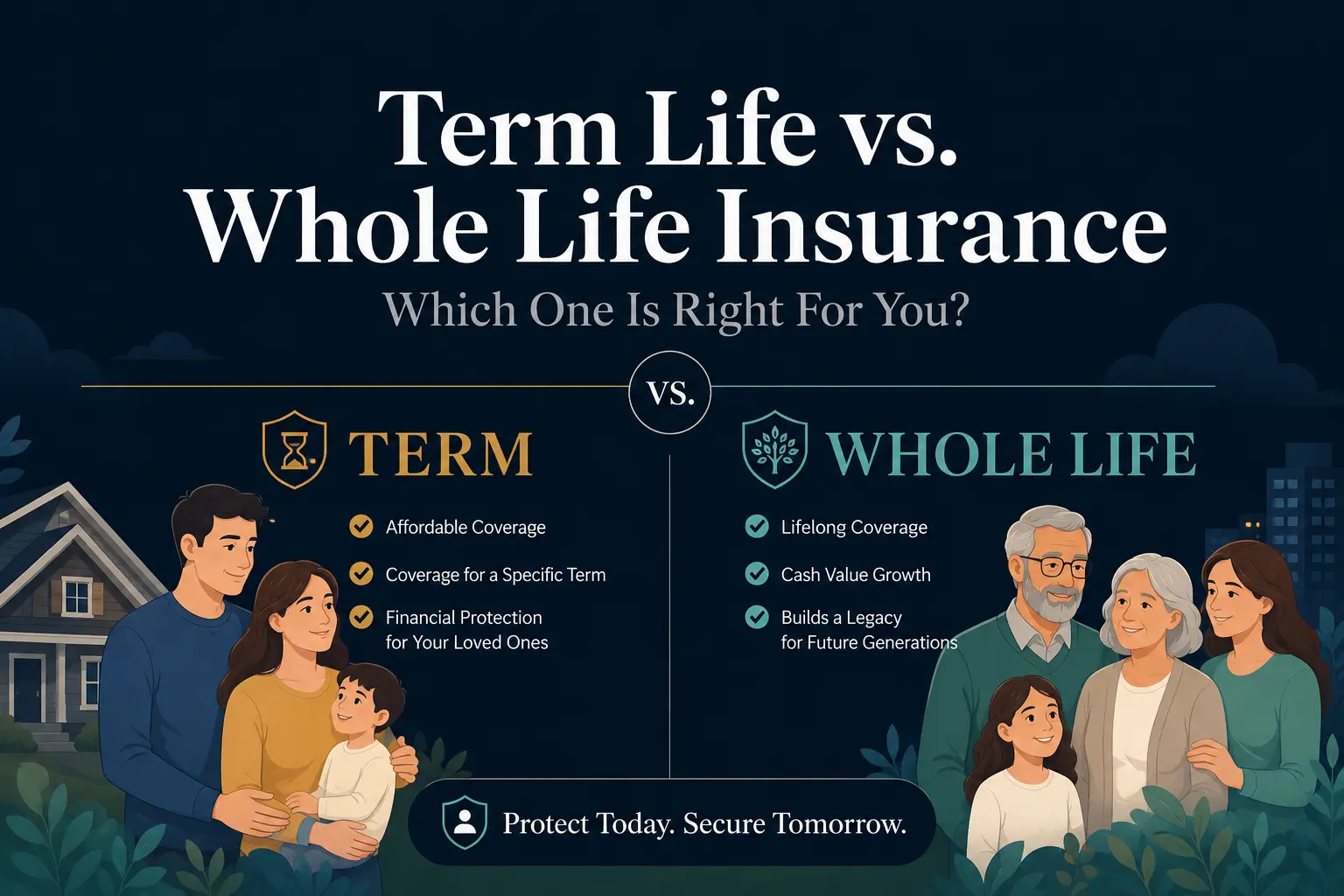

Term Life Insurance Vs Permanent Life Insurance

Term life insurance provides coverage for a set period, such as 10, 20, or 30 years. It is often the most cost-effective way to cover high-need years like raising kids or paying a mortgage. Premiums are usually lower because it is designed for protection rather than long-term cash value.

Permanent life insurance can last for life if premiums are paid. It may build cash value and can be used for estate planning or lifelong dependents, but costs are typically higher. Matching policy type to the purpose keeps the plan efficient.

- Term coverage fit: Income replacement, mortgage protection and temporary family obligations.

- Permanent coverage fit: Long-term needs, legacy goals and complex tax or estate situations.

Many households use term life insurance for the bulk of coverage and add permanent coverage only if a long-lasting need exists.

How Long Your Coverage Should Last?

The amount and the term length work together. A larger amount for a shorter term can be cheaper than a smaller amount for a longer term, depending on age and health. The right duration follows the timeline of your obligations.

Common end points include when children become financially independent, when a mortgage is paid off, or when retirement savings are on track. If your income would be hard to replace due to specialized skills, a longer term may make sense. If you have strong savings and low debt, a shorter term may be enough.

- Family timeline: Coverage through the years dependents rely on your income.

- Debt timeline: Coverage until large loans are paid off or refinanced.

- Retirement timeline: Coverage until the surviving spouse can rely on retirement assets.

When term length matches real deadlines, it becomes easier to avoid paying for coverage beyond the need.

Use This Coverage Planning Table

A table helps you organize the decision without turning it into a complicated spreadsheet. Add your own numbers in each row, then total the needs and subtract available resources. Review it with the person who would be impacted by the policy.

| Coverage Component | What To Include | How It Affects Your Amount |

|---|---|---|

| Income Replacement | Essential annual spending minus survivor income | Usually the largest driver of coverage |

| Debt Payoff | Mortgage, loans, credit balances, co-signed debts | Adds one-time needs and reduces monthly burden |

| Future Goals | Education funding, retirement bridge, caregiving costs | Raises coverage when goals are important |

| Existing Resources | Savings, investments, current policies, employer benefits | Subtracts from needed coverage total |

Once the table is filled, you can round the final range to a policy amount that is easy to maintain.

Budget and Underwriting Realities

The best coverage amount is the one you can keep in force. Premiums depend on age, health, tobacco use and the policy type and length. Shopping for a realistic amount helps you avoid dropping coverage later.

Underwriting can also affect timing. If you have medical conditions, the insurer may ask for records, labs, or an exam. If speed matters, ask about accelerated underwriting options, but confirm any limits on coverage amounts.

- Premium flexibility: A slightly lower amount that stays active is better than an unaffordable ideal.

- Policy ownership: Keep beneficiaries updated and store documents where family can access them.

- Riders and add-ons: Choose only those that match your needs, such as a waiver of premium.

Balancing coverage with affordability is part of building a plan that survives real life changes.

When to Recalculate Your Life Insurance Need

Life insurance is not a one-time decision. Major life events can shift both the amount and the term you need. Regular reviews keep coverage aligned with your current responsibilities.

Revisit your numbers after marriage, divorce, a new child, a home purchase, or a significant change in income. Also review after paying off large debts or building substantial savings. A quick annual check is often enough to catch changes early.

- Family changes: New dependents or a spouse returning to work.

- Debt changes: Refinancing, new mortgage, or paying off student loans.

- Career changes: Job loss, self-employment, or losing employer-provided coverage.

Small updates over time prevent the need for stressful last-minute decisions.

Conclusion

The right answer to how much life insurance you need comes from matching coverage to real obligations and real goals. Add income replacement, debt payoff and key milestones, then subtract resources already in place. Choose a term length that lines up with the years your household would be most vulnerable.

When you use a clear method and review it after major life changes, life insurance becomes a simple protective tool rather than a mystery number. Aim for enough coverage to keep your family stable and keep premiums at a level you can sustain.