Buying life insurance is less about age and more about who depends on your income, your health and how long you need protection. The best time is usually before major responsibilities stack up and before health risks can raise premiums.

A good policy can protect a partner, children, aging parents, or a business. It can also cover debts, replace income and fund final expenses without forcing your family into quick financial decisions.

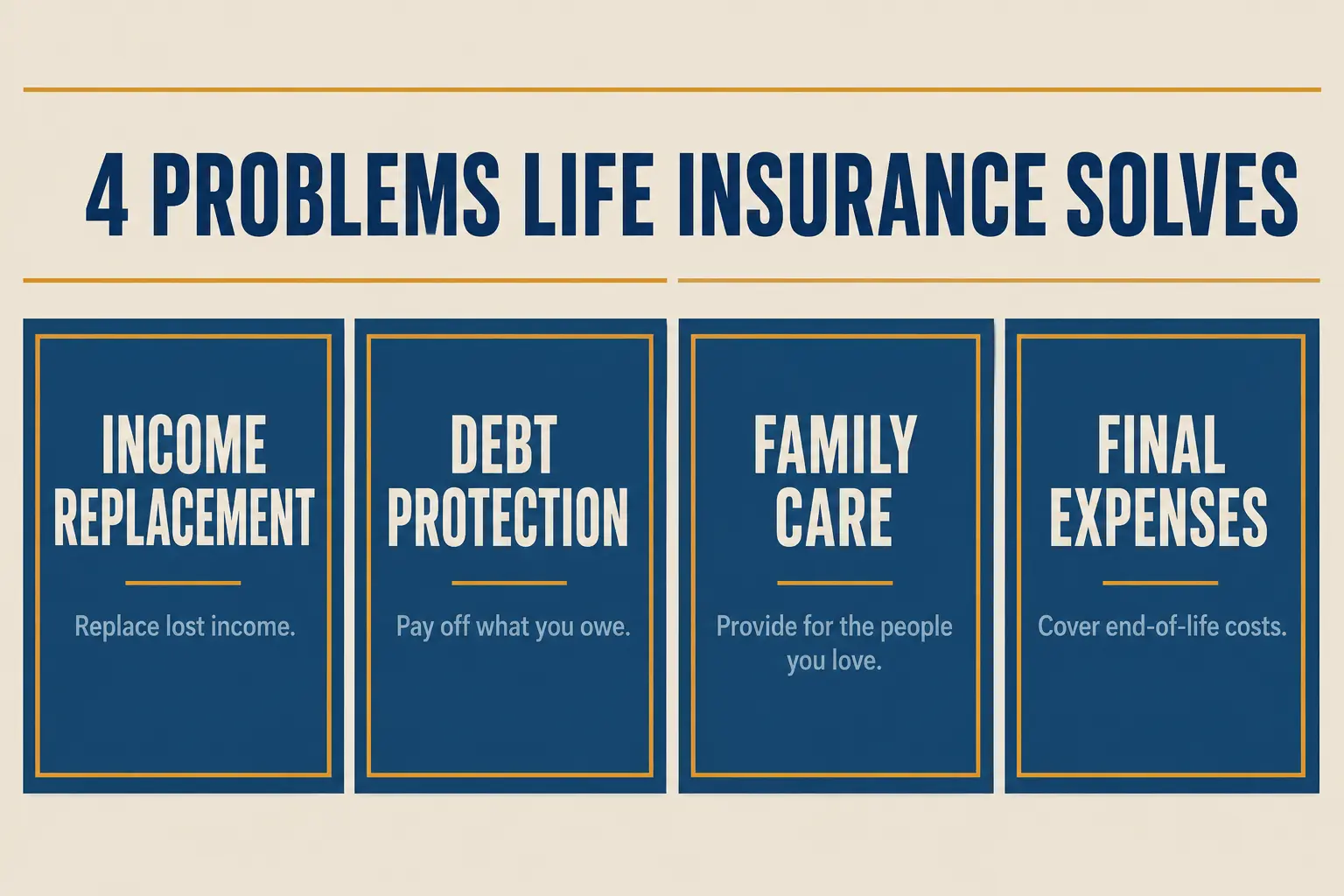

What Life Insurance Is Meant To Solve?

Life insurance creates a lump sum payment for your beneficiary if you die while the policy is active. That money can keep a household stable when a paycheck disappears.

Most people use it to replace income, pay a mortgage, clear student loans, or cover childcare and education costs. Others use it to protect a co-signer, fund a buy-sell agreement, or leave a modest legacy.

- Income replacement. Helps a household pay rent, utilities and groceries while adjusting to a loss.

- Debt protection. Reduces the risk that survivors inherit or struggle with major debts.

- Family care. Supports childcare, eldercare and ongoing medical needs.

- Final expenses. Covers burial, cremation and end-of-life bills.

Once you know the problems you are solving, choosing the type and amount becomes much simpler.

Term Life Vs Whole Life

Term life covers you for a set period such as 10, 20, or 30 years. It is often the most cost-effective way to insure a large need for a limited time.

Whole life and other permanent policies can last for life and may build cash value. They can fit specific goals, but they usually cost more and require long-term commitment.

- Term life. Lower premiums for higher coverage, best for mortgages, income replacement and young families.

- Whole life. Lifetime coverage with fixed premiums, useful for estate needs or lifelong dependents.

- Universal life. Flexible premiums and potential cash value growth, but can be complex to manage.

Most households start with term life and add permanent coverage only when a clear, long-term need exists.

How Much Coverage You May Need?

A practical approach is to estimate how much money your family would need to maintain their standard of living. Then subtract assets that could realistically be used, such as savings, investments and existing employer life insurance.

Many people start with a simple checklist that covers big obligations and essential ongoing costs.

- Income years. How many years of income should be replaced and at what percentage.

- Housing. Mortgage balance, rent support, property taxes and maintenance.

- Debts. Student loans, car loans, personal loans and credit cards.

- Family needs. Childcare, education funding and care for a disabled family member.

- Buffer. An added margin for inflation, job changes and emergencies.

This creates a target range that can guide quotes and prevent underinsuring or overbuying.

Life Insurance In Your 20s

In your 20s, the main advantage is price and insurability. If you are healthy, you can often lock in a low premium for a long term length.

You may need coverage if someone would struggle to pay shared rent, debts, or funeral costs. A small to moderate term policy can also protect a parent who co-signed loans.

- Good fit. 20 to 30 year term life that can cover early career years and future family plans.

- Watch out for. Relying only on employer coverage that may end when you change jobs.

Getting coverage early can be a simple way to reduce long-term cost, even if your needs are not yet large.

Life Insurance In Your 30s

Your 30s often bring marriage, children and larger fixed expenses. This is when many people have their highest need for income replacement.

A term life policy aligned with the remaining years on a mortgage and the years until children become financially independent can be a strong match. If you are building a business, coverage can also support a partner or fund business continuity.

- Good fit. Term life sized to cover a mortgage payoff plus several years of living expenses.

- Watch out for. Choosing a term that ends before kids finish school or before debts are manageable.

At this stage, buying enough matters more than finding the lowest possible premium.

Life Insurance In Your 40s

In your 40s, your income may be higher, but so are the stakes. Health changes can also begin to affect underwriting, which can increase premiums or limit options.

Many families use this decade to review coverage, add supplemental term life, or extend a policy to match remaining obligations. If you support aging parents, insurance can reduce pressure on a surviving spouse.

- Good fit. 10 to 20 year term life that matches the final stretch of major debts and dependent years.

- Watch out for. Letting an older policy lapse without replacing it, especially if health has changed.

A review can uncover gaps caused by bigger mortgages, new children, or changes in income.

Life Insurance In Your 50s

In your 50s, the decision usually focuses on protecting a spouse, covering final expenses and managing debt as retirement approaches. Premiums can rise quickly, so you may need to balance coverage amount with affordability.

If your children are independent and your mortgage is nearly paid off, your need may be smaller. If you still have dependents, significant debt, or a business, coverage can still be essential.

- Good fit. A shorter term policy to bridge to retirement income or a smaller permanent policy for lifelong needs.

- Watch out for. Buying more coverage than your budget can sustain for the full term.

This is also a good time to confirm beneficiaries and ensure your policy aligns with your estate plan and retirement accounts.

Quick Timing Guide By Decade

Age is not a rule, but it can shape price, health underwriting and how long you need coverage. Use the table to compare common goals and policy choices across decades.

| Decade | Common Financial Trigger | Typical Policy Approach |

|---|---|---|

| 20s | First major debt, co-signed loans, partner relies on income | Longer term life with modest to mid coverage |

| 30s | Marriage, kids, mortgage, peak income replacement need | Term life matched to mortgage and child-rearing years |

| 40s | Higher income, larger obligations, health changes | Review and extend term or add supplemental term life |

| 50s | Retirement planning, debt payoff, spouse protection | Shorter term bridge or smaller permanent coverage for lasting needs |

Once you identify your trigger, you can choose a term length that ends when your biggest financial risks end.

What Affects Your Premium The Most?

Insurers price policies based on risk and a few factors carry more weight than most people expect. Health and tobacco use often matter more than age alone.

Understanding these drivers can help you prepare before applying.

- Health history. Blood pressure, cholesterol, diabetes and past diagnoses can change rates.

- Tobacco and nicotine. Smoking and vaping can raise premiums significantly.

- Build and vitals. Height, weight and lab results influence underwriting classes.

- Family history. Some conditions in close relatives can affect risk scoring.

- Driving record. Serious violations can raise premiums.

Small improvements in health and documentation can sometimes move you into a better rate class.

How To Choose a Term Length That Fits>

Term length should match the period when your family would be financially exposed. If your main risk is a 25-year mortgage, a 20-year policy may end too soon.

It can help to map coverage to milestones like the last day of a mortgage, the youngest child finishing school, or a planned retirement date.

- List time-bound obligations. Include mortgages, loans and the years dependents will rely on you.

- Pick the longest critical timeline. Choose a term that covers the largest risk window, not the smallest one.

- Stress-test affordability. Ensure premiums still fit if your budget tightens or you change jobs.

- Consider layered coverage. Pair a longer base term with a shorter additional term for peak years.

A clear timeline prevents buying a policy that ends right when protection is needed most.

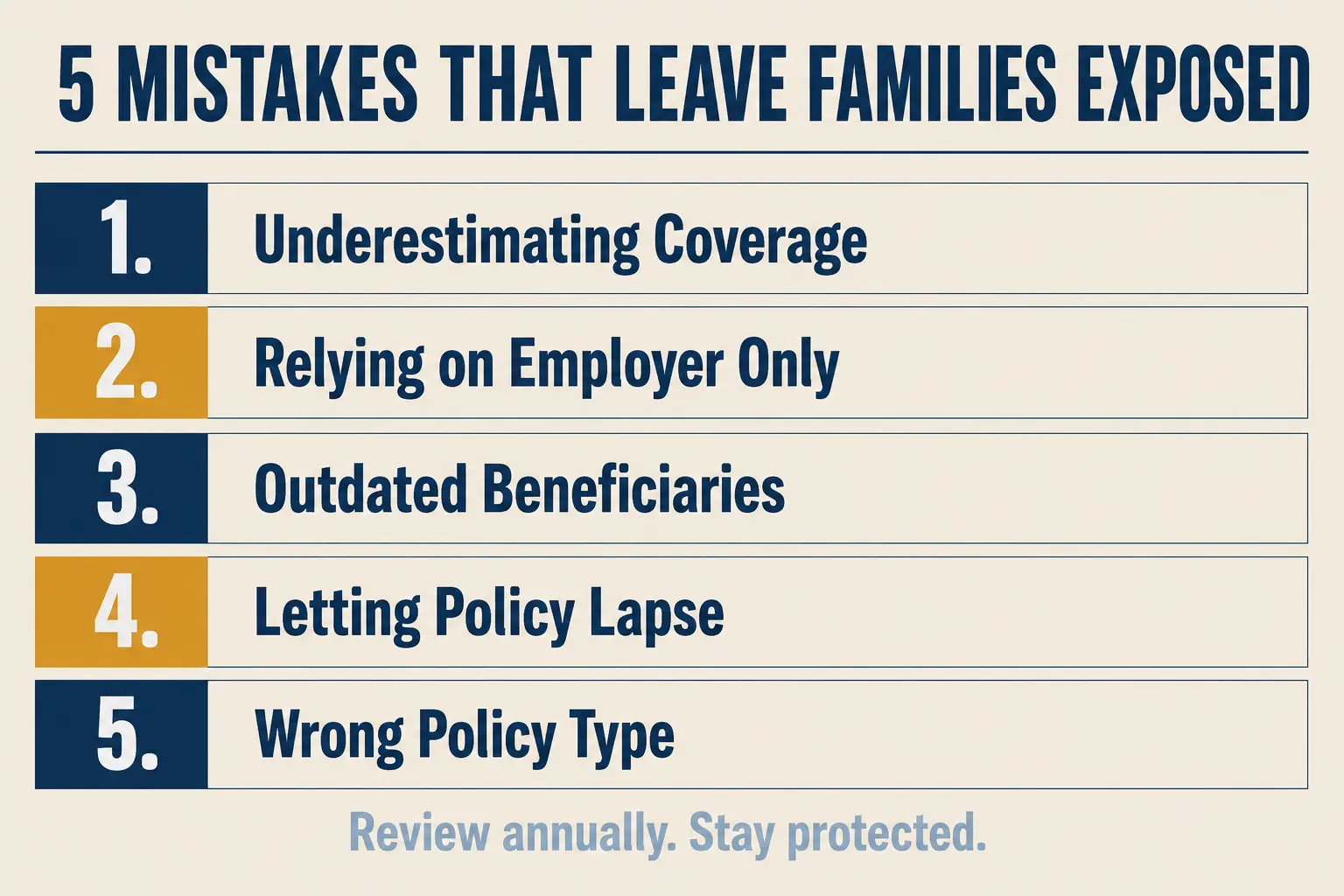

Mistakes That Can Leave Families Exposed

Life insurance works best when it is simple, accurate and kept up to date. Many coverage gaps happen because policies were never reviewed after a major life change.

These issues are common and often easy to avoid.

- Underestimating coverage. Small policies may not replace income long enough to matter.

- Only using employer coverage. Job changes and layoffs can end protection quickly.

- Outdated beneficiaries. Divorce, remarriage and new children require updates.

- Letting a policy lapse. Missed payments can cancel coverage when health has already changed.

- Buying the wrong type. Permanent life may strain cash flow if term life would meet the same goal.

A short annual review can prevent most of these problems and keep your plan aligned with your life.

Conclusion

The best time to buy life insurance is when someone would be financially hurt by your absence and while you can still qualify for strong rates. Your 20s favor locking in affordability, your 30s often bring the largest need, your 40s reward proactive reviews and your 50s focus on bridging to retirement and protecting a spouse.

Start with the financial risk you need to cover, choose term life when the need is time-limited and keep beneficiaries current. A policy that matches your timeline and budget can provide clear protection without complexity.

FAQ’s

1: Can I buy life insurance if I already have health problems?

Yes, many people with existing health conditions can still qualify for life insurance. Your premium will depend on factors such as the type and severity of your condition, your treatment history and your overall health. Comparing multiple insurers can help you find coverage that fits your situation.

2: Is employer-provided life insurance enough for most families?

In many cases, no. Employer-sponsored life insurance is often limited to one or two times your annual salary and may end if you leave your job. If you have a mortgage, children, or other financial responsibilities, an individual life insurance policy can provide more reliable long-term protection.

3: Can I have more than one life insurance policy?

Yes, it is possible to own multiple life insurance policies if the total coverage reflects your financial needs. Some people combine different policies to cover separate goals, such as income replacement, mortgage protection, business obligations, or final expenses. This approach can provide more flexibility as your financial responsibilities change over time.