Buying life insurance for the first time can feel unfamiliar, but the process becomes manageable when you break it into clear decisions. The goal is simple protect the people who rely on you while keeping the premium affordable and the policy easy to maintain.

This guide focuses on how policies work, how insurers price coverage and how to choose an amount and term that match real needs. You will also learn what to prepare before applying so underwriting surprises are less likely.

What Life Insurance Does and When You Need It?

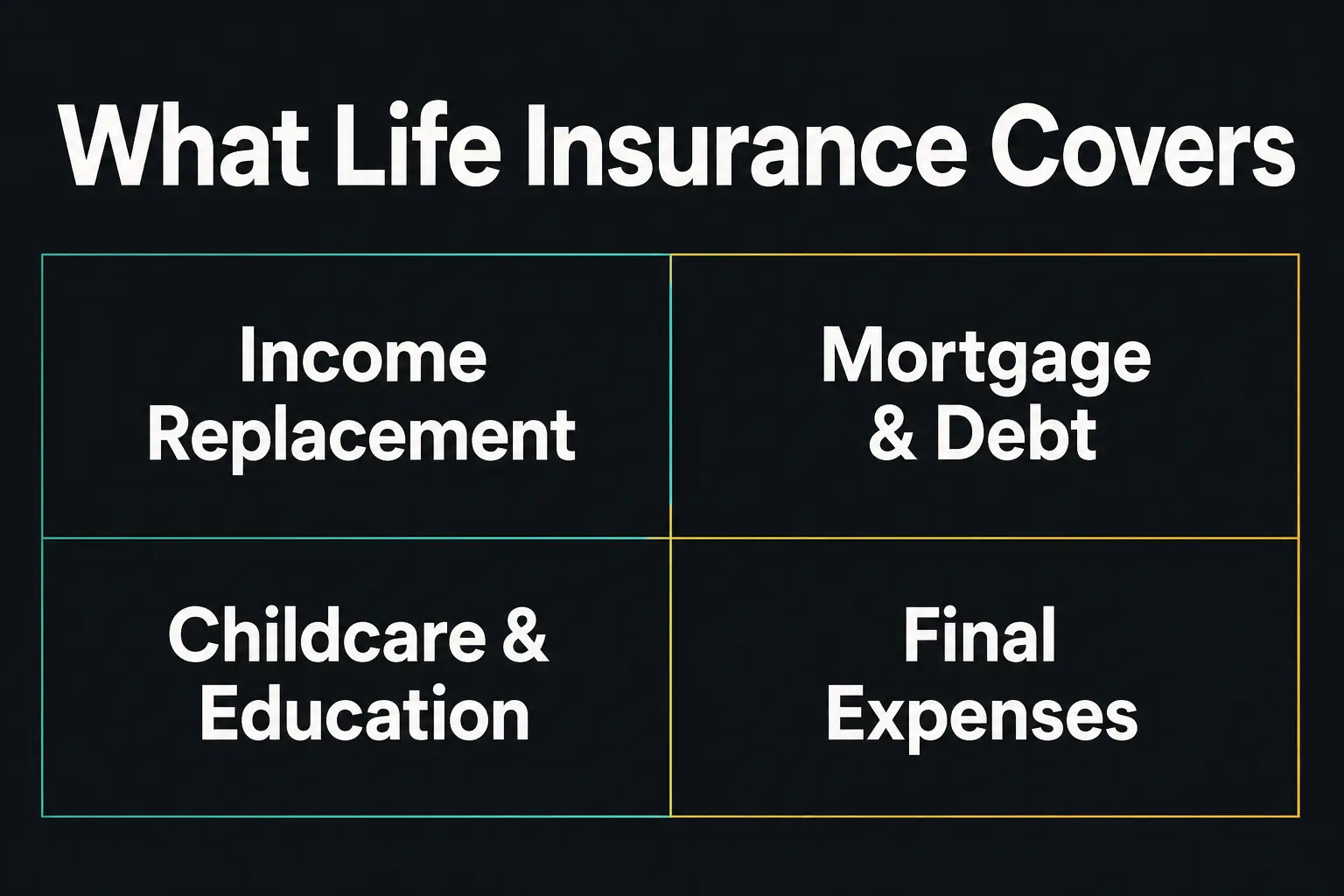

Life insurance replaces income and covers costs if you die while the policy is in force. It can pay for housing, childcare, debt payoff, education plans and final expenses.

You typically need it when someone would face financial hardship without your earnings or support. Common triggers include starting a family, buying a home, taking on shared debt or supporting aging parents.

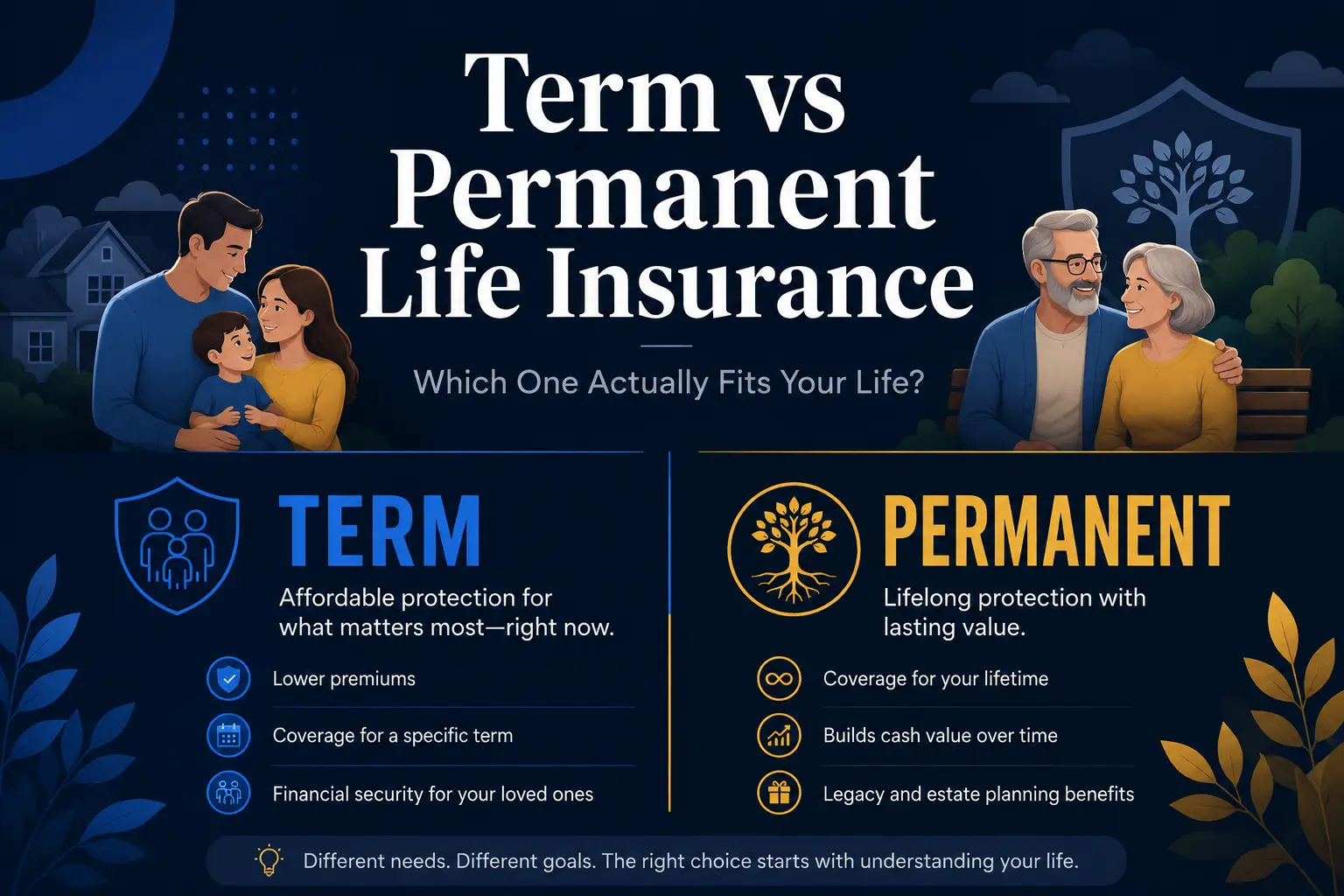

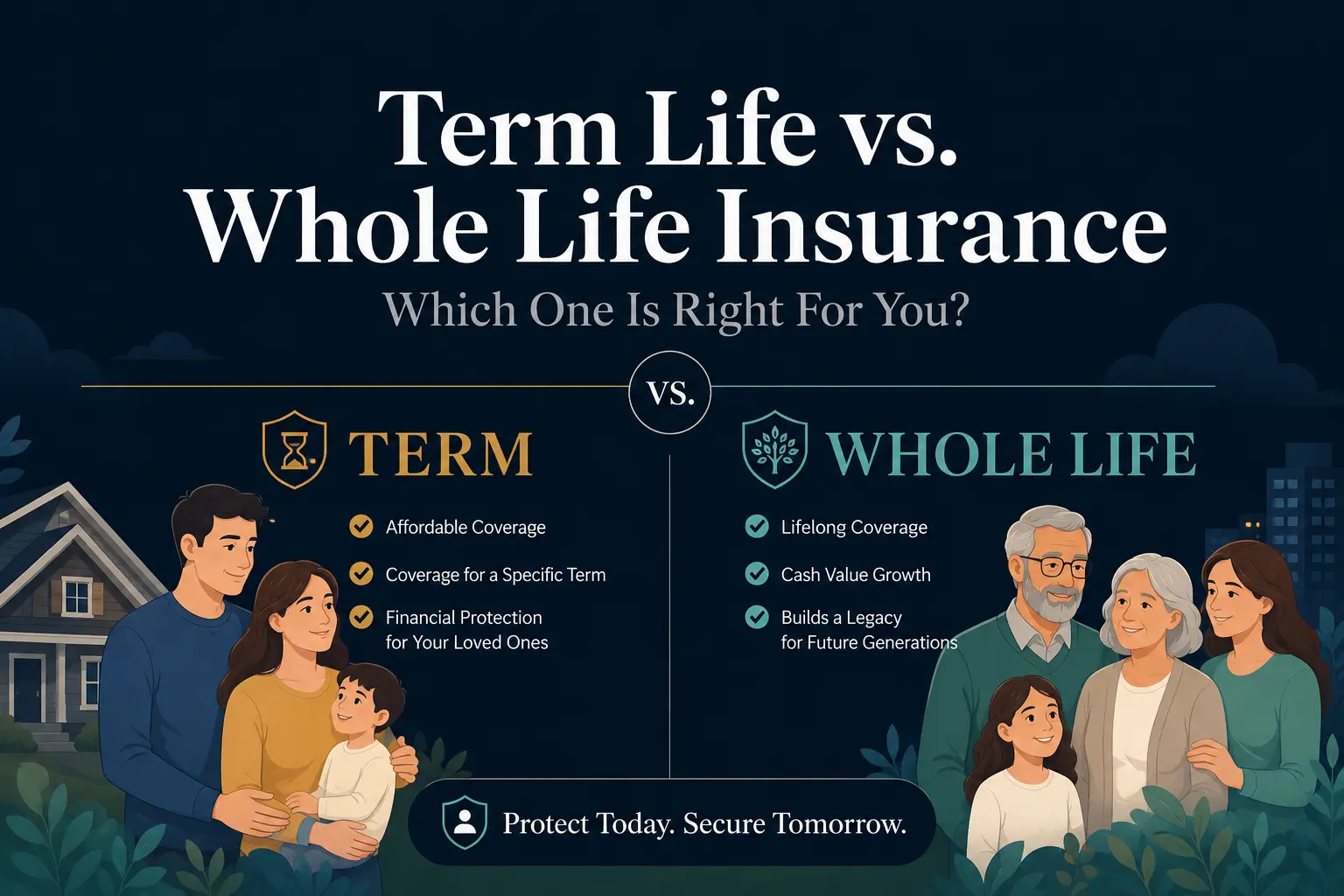

Term Life Vs Permanent Life Insurance

Most first-time buyers start by comparing term life and permanent life. The right choice depends on how long you need coverage and whether you want a cash value feature.

Term life covers a set period and is usually the most cost-effective way to buy a larger death benefit. Permanent life can last for life if premiums are paid and may build cash value, but it is typically more expensive.

- Term life insurance: Lower premiums for a fixed number of years, straightforward protection, good fit for time-bound responsibilities.

- Whole life insurance: Lifelong coverage with level premiums and cash value growth, higher cost, more guarantees.

- Universal life insurance: Flexible premiums and adjustable death benefit, cash value tied to interest crediting, requires monitoring.

Once you know whether you want pure protection or a policy with long-term features, you can focus on coverage amount and affordability.

How Much Coverage to Buy?

Coverage should be tied to obligations and the time your household needs financial support. A practical approach is to list major needs and subtract assets that would be available.

Start with income replacement, then add specific costs like mortgage payoff, childcare, education funding and final expenses. Subtract savings, existing insurance through work and investments that dependents could use.

- Income replacement: Consider a number of years your household needs support while kids grow or a partner retrains.

- Debt and housing: Include mortgage balance, car loans and any co-signed or shared debt.

- Family care: Estimate childcare, eldercare and health coverage transition costs.

- Final expenses: Include funeral costs and immediate bills to avoid burdening family members.

Keep the first policy simple and scalable. If needs grow later, you can add coverage or buy a second policy rather than overbuying now.

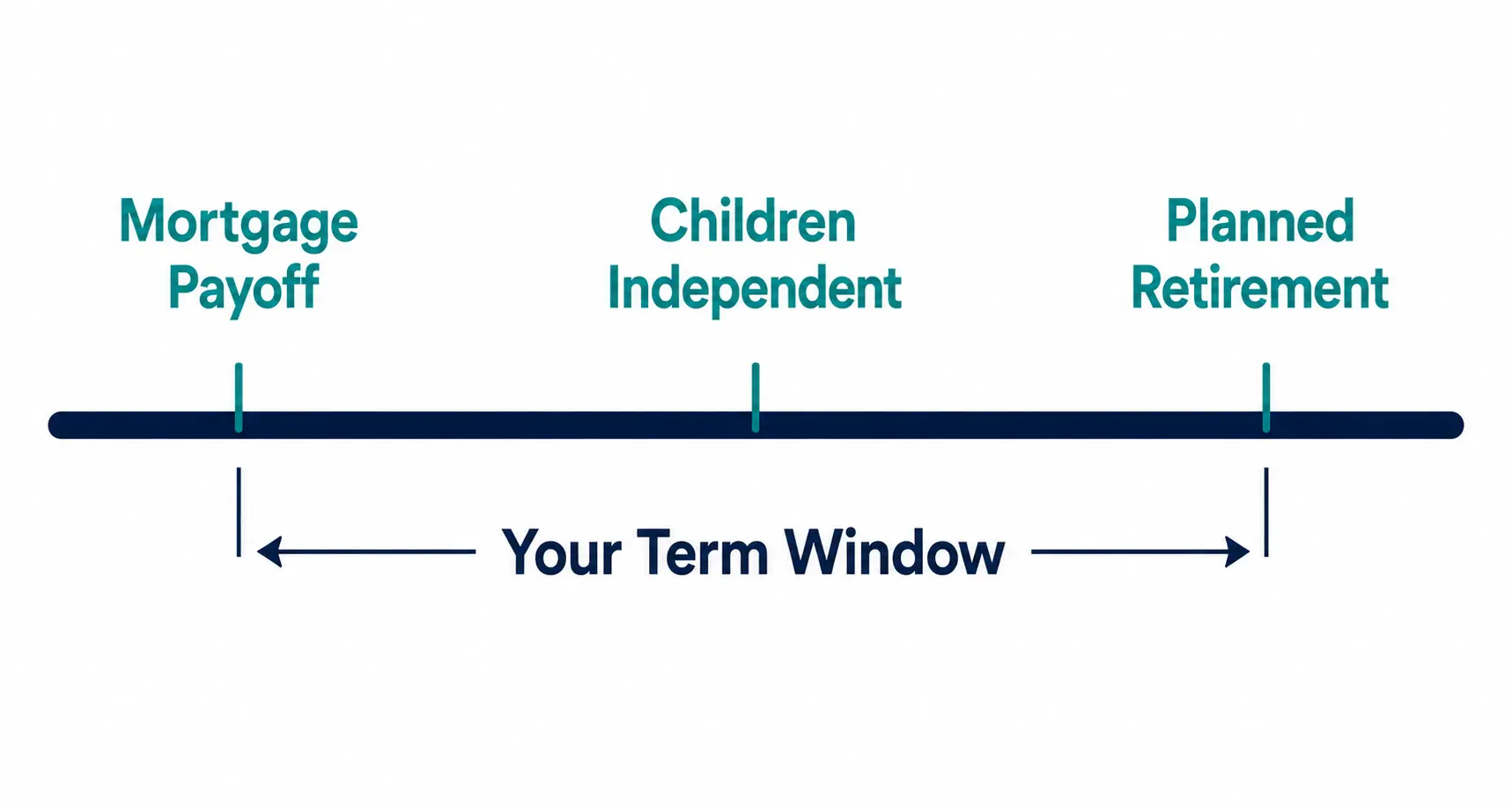

Choosing The Right Term Length

Term length should match the window when financial risk is highest. Many people align it with the years left on a mortgage, the time until children are independent or the years until planned retirement.

A longer term costs more, but it can lock in insurability for longer. A shorter term is cheaper, but you may face higher prices if you need to renew later.

- Identify your longest major obligation. Use mortgage payoff, dependent support or expected retirement date as the anchor.

- Stress test the timeline. Add a buffer for job changes, medical events or delayed retirement.

- Balance premium and certainty. Choose the shortest term that still covers your true risk window.

This keeps the policy aligned with real responsibilities while avoiding paying for coverage long after it is needed.

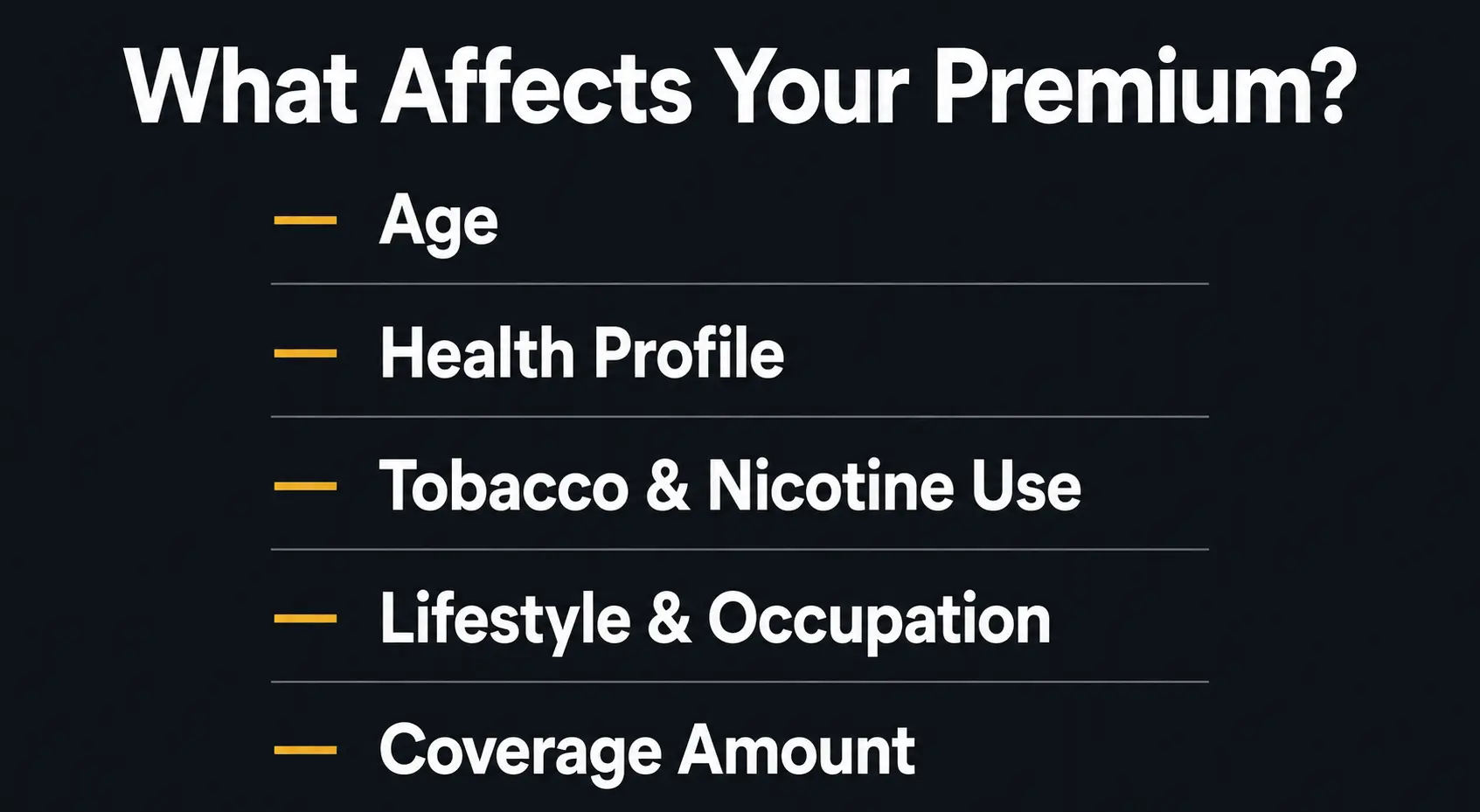

What Affects Life Insurance Premiums?

Insurers price policies using mortality risk factors. The biggest drivers are age, health history, tobacco use, family medical history, driving record and the amount and type of coverage.

Underwriting can be fully underwritten with a medical exam or simplified with limited health questions. Fully underwritten policies often offer the best rates when health is good.

- Age: Rates usually increase as you get older, so buying earlier can reduce long-term cost.

- Health profile: Blood pressure, cholesterol, BMI and prescription history can move you into a different rate class.

- Tobacco and nicotine: Nicotine use can raise premiums sharply, including vaping and certain substitutes.

- Lifestyle and occupation: High-risk hobbies or dangerous work may require extra rating or exclusions.

Knowing what affects pricing helps you decide whether to apply now or work on health improvements before submitting an application.

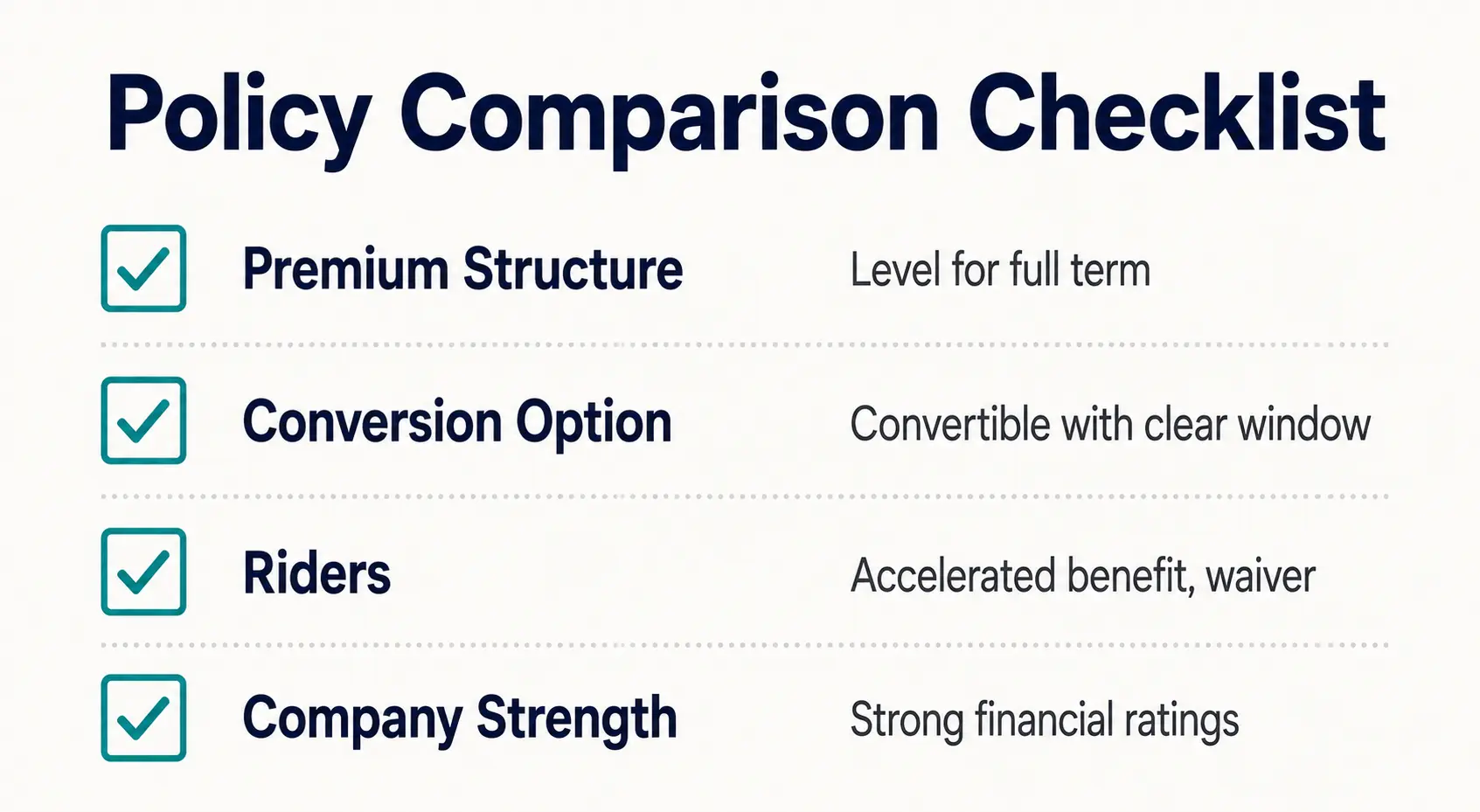

Comparing Quotes and Policy Features

Price matters, but policy structure matters too. Compare the insurer’s financial strength, premium schedule, conversion options and riders that may add value.

Pay attention to whether the premium is level for the full term and what happens at the end of the term. Also check how easily the policy can be converted to permanent coverage without a new medical exam.

| What to Compare | Why it Matters | What to Look For |

|---|---|---|

| Premium Structure | Predictable costs make budgeting easier | Level premium for the full term |

| Conversion Option | Protects insurability if health changes | Convertible term with clear conversion window |

| Riders | Adds flexibility for life events | Accelerated death benefit, waiver of premium if needed |

| Company Strength | Claims-paying ability over decades | Strong financial ratings and stable history |

After narrowing options, review the contract language carefully so the coverage behaves the way you expect under stress.

Understanding Beneficiaries and Ownership

The beneficiary receives the death benefit, while the owner controls the policy. You can name primary and contingent beneficiaries to prevent delays if a beneficiary is not alive at the time of claim.

Keep beneficiary designations consistent with your broader plan for dependents and property. Update beneficiaries after marriage, divorce, births or major financial changes.

- Primary beneficiary: First in line to receive the proceeds.

- Contingent beneficiary: Receives the proceeds if the primary beneficiary cannot.

- Minor children: May require a guardian arrangement to avoid court involvement.

Clear ownership and beneficiary choices reduce confusion and speed up claims when your family needs funds quickly.

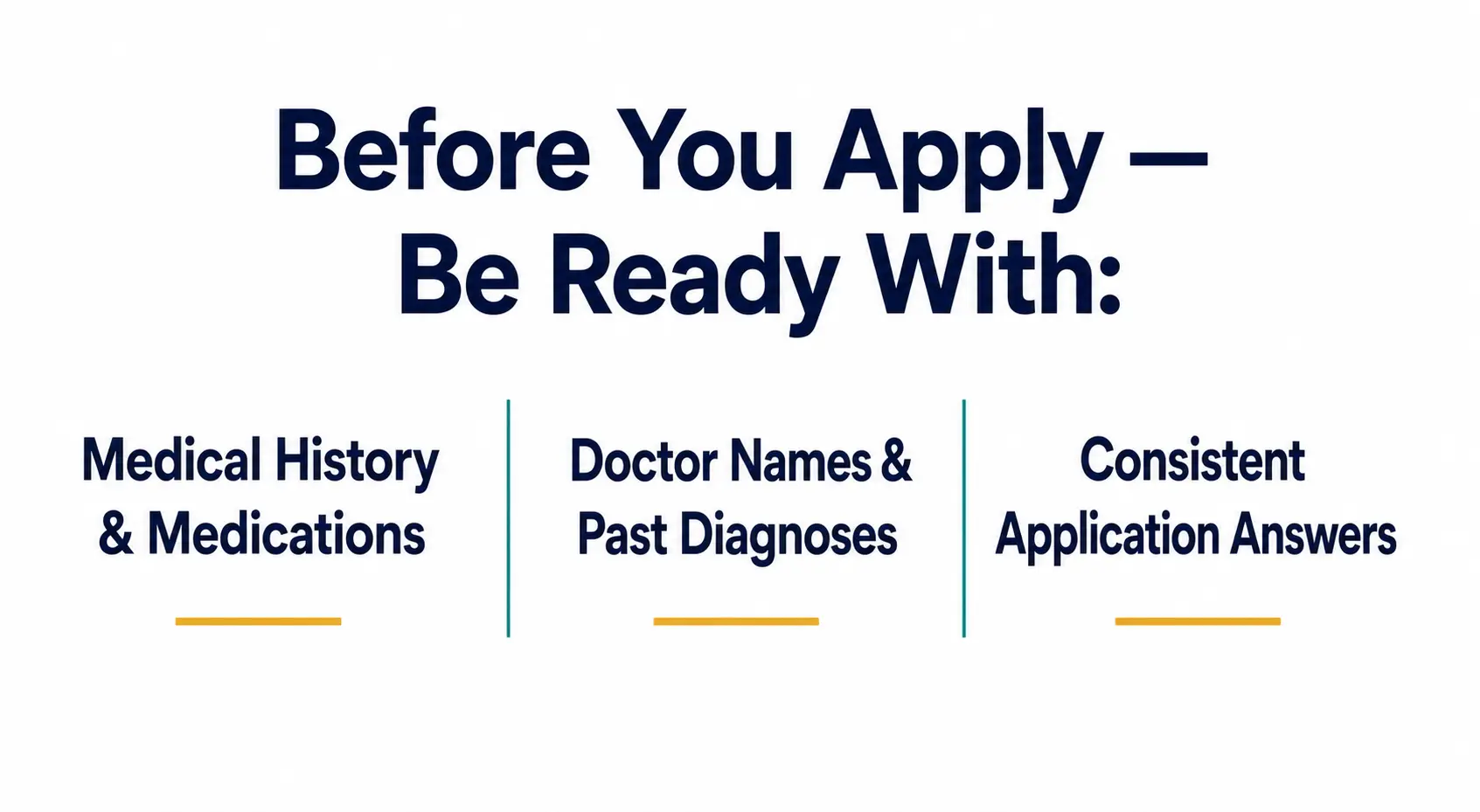

Preparing For The Application and Medical Exam

Applications move faster when your information is complete and consistent. Insurers may request identity verification, medical history, prescription checks and attending physician statements.

If a medical exam is required, basic preparation can improve the accuracy of results. Avoid heavy exercise right before the exam, stay hydrated and be ready to confirm medications and medical history.

- Gather key details. Have your doctor names, medications and past diagnoses ready to reduce back-and-forth.

- Schedule wisely. Choose a time when you are rested and can follow normal routines.

- Answer consistently. Match your application answers to your medical records as closely as possible.

This preparation reduces delays and helps avoid rating surprises caused by missing context or inconsistent disclosures.

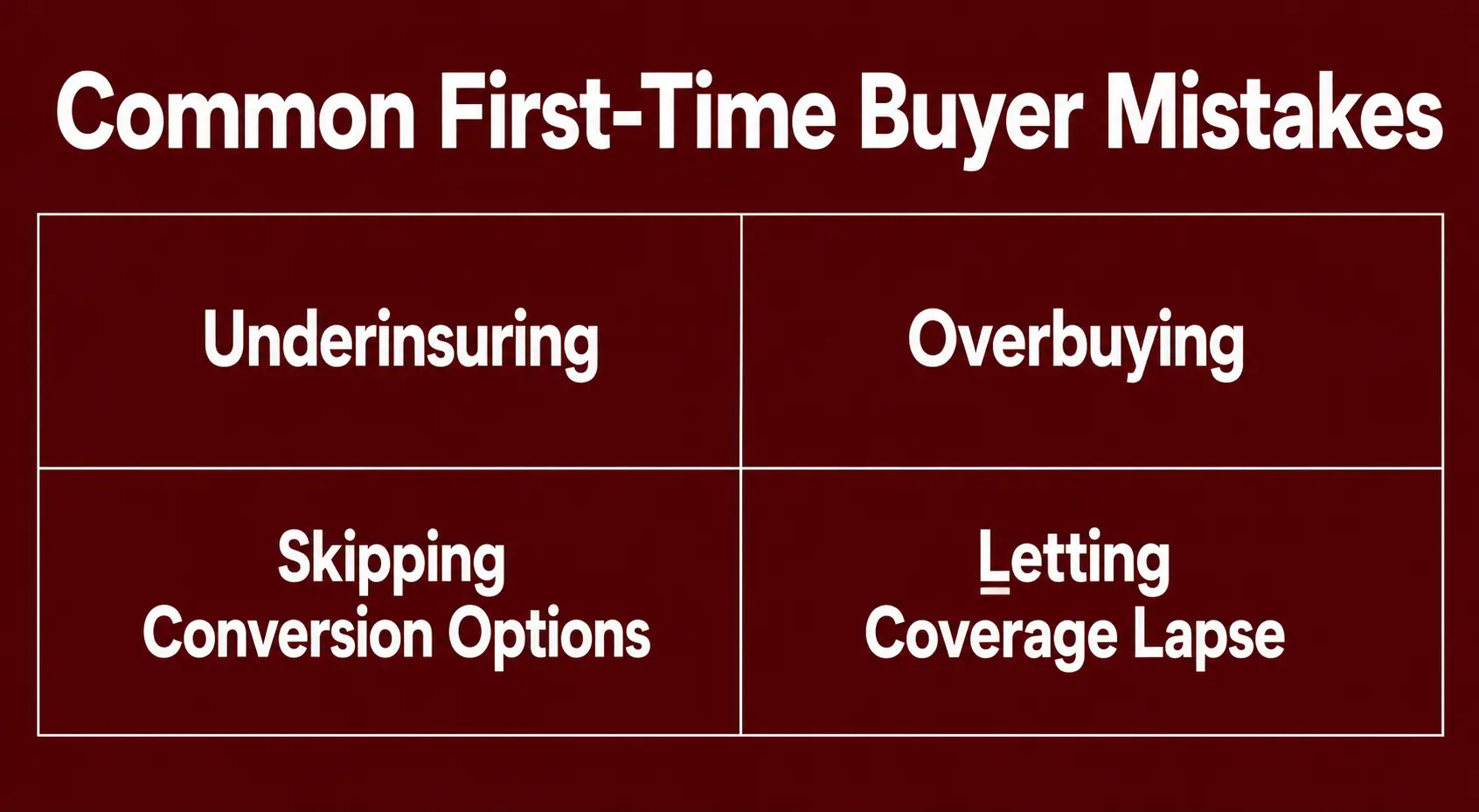

Avoiding Common First-Time Buyer Mistakes

Many problems come from buying based on price alone or assuming work coverage is enough. Another frequent issue is choosing a term that expires while dependents still need support.

It also helps to avoid policies that you do not understand. If the policy includes cash value or flexible premiums, make sure you know how it performs under lower funding or market changes.

- Underinsuring: Small policies may not cover housing and child-related costs, leaving a gap.

- Overbuying: Excess coverage can strain budgets and lead to lapses, which defeats the purpose.

- Ignoring conversion: Skipping conversion options can limit choices if health worsens.

- Letting coverage lapse: Missed premiums can cancel protection, so set up reminders or autopay.

Good coverage is coverage you can keep. A stable policy with a manageable premium is often better than an ambitious plan that becomes hard to maintain.

Conclusion

Buying life insurance for the first time is mainly about matching coverage to real obligations, choosing the right policy type and locking in a term length that fits your risk window. Focus on clear numbers, solid contract features and an insurer you trust.

When you compare quotes thoughtfully, prepare for underwriting and keep beneficiary details current, life insurance becomes a reliable safety net rather than a confusing purchase. Start with the protection your household truly needs and refine it as your life changes.