Choosing a life insurance beneficiary is one of the most important parts of setting up a policy. The right designations help your benefits reach the right people quickly and with fewer disputes.

Beneficiary rules can feel detailed, yet most problems come from a few common mistakes. This guide explains primary, secondary, and minor beneficiaries in plain language, so you can make confident updates.

What a Life Insurance Beneficiary Means?

A beneficiary is the person or entity that receives the life insurance death benefit after the insured person dies. The insurer pays the proceeds based on the beneficiary designation on file, not based on a will in most cases.

Because the designation is part of the contract, it usually overrides instructions written elsewhere. That is why accuracy matters, including names, relationships, and contact details.

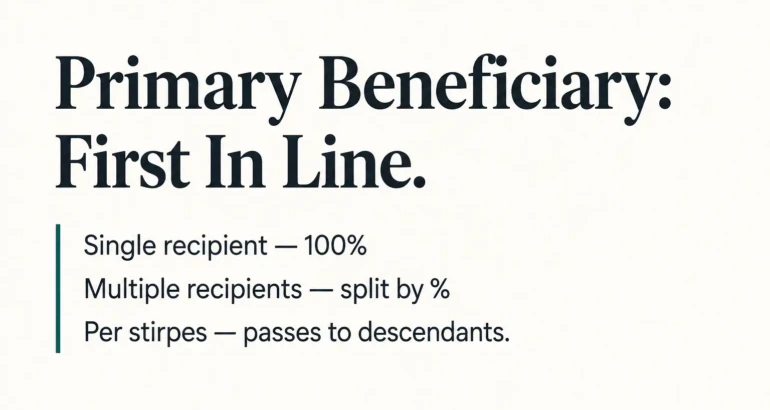

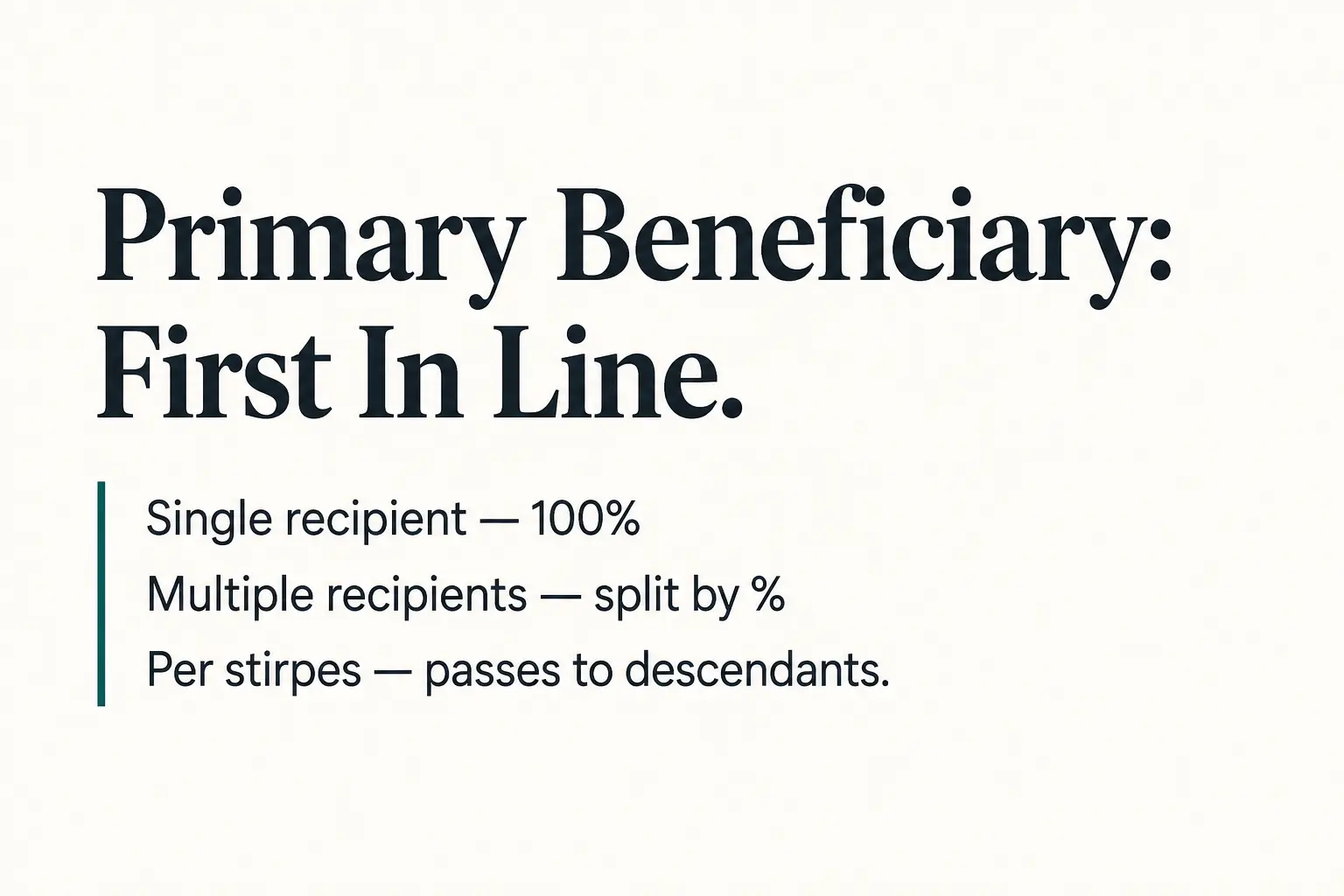

Primary Beneficiary Basics

A primary beneficiary is first in line to receive the death benefit. If the primary beneficiary is alive and eligible at the time of the claim, the insurer pays them according to the policy terms.

You can name one primary beneficiary or several. When you name multiple primary beneficiaries, you typically assign each a percentage share.

- Single primary beneficiary. One person or entity receives 100 percent of the proceeds.

- Multiple primary beneficiaries. Shares are split by percentage, such as 60 percent and 40 percent.

- Per stirpes option when available. A share can pass to a beneficiary’s descendants if that beneficiary dies first.

Clear percentages reduce delays because the carrier does not need extra interpretation. If percentages do not add up correctly, claims can stall until corrected.

Secondary Beneficiary and Contingent Beneficiary Rules

A secondary beneficiary, often called a contingent beneficiary, receives the death benefit if the primary beneficiary cannot receive it. This could happen if the primary beneficiary died before the insured, cannot be located, or is legally ineligible.

Adding a secondary beneficiary is a simple way to reduce the chance the proceeds go to the insured person’s estate. Estate payouts often require probate, which can add time and cost.

- Backup planning. A contingent beneficiary keeps benefits moving if the primary designation fails.

- Reduced probate risk. Direct payments typically avoid estate administration delays.

- Cleaner family outcomes. A clear order of payment lowers the chance of conflict.

After you set contingent beneficiaries, review them during major life changes. Births, divorces, remarriages, and deaths are common triggers for updates.

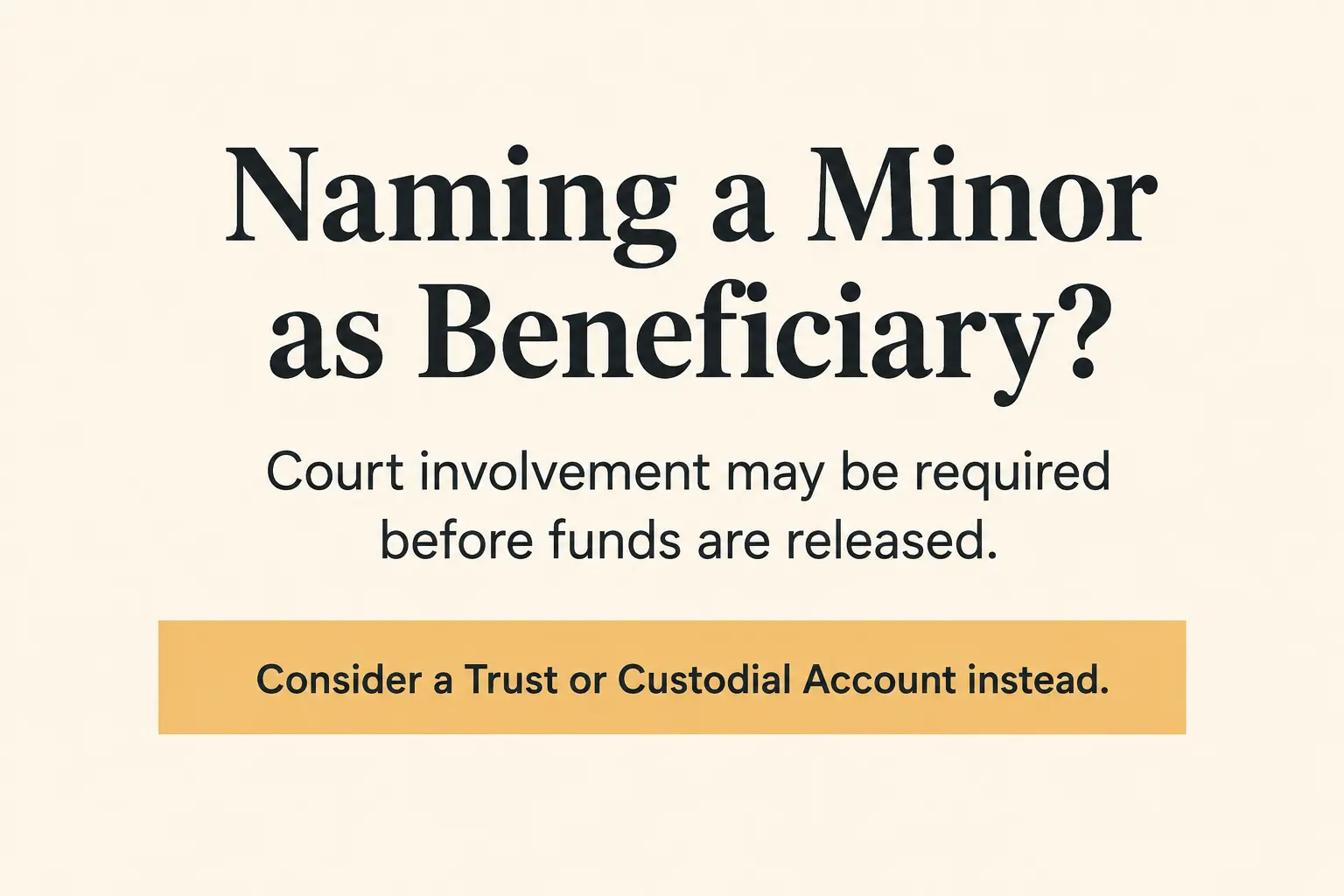

Minor Beneficiaries and Legal Limits

Many states restrict direct life insurance payouts to minors. Even when minors are allowed as named beneficiaries, insurers often require a legal guardian or court appointed conservator to receive and manage the money.

This extra legal step can delay payment and add expenses. It can also create a result you did not intend if the court appoints someone you would not have chosen.

- Guardianship or conservatorship requirements. A court process may be needed before funds are released.

- Age of majority rules. A minor gains control at the state’s legal age, which may not match your wishes.

- Higher dispute risk. Family members may disagree about who should manage the benefit.

A better approach is usually to direct the benefit to a legal structure that can hold funds for a child. That keeps your plan private and more predictable.

Options To Protect a Child’s Inheritance

There are several ways to structure life insurance proceeds for a child without naming the child as the direct payee. The right method depends on your state law, the policy type, and your broader estate plan.

Many people coordinate beneficiary choices with an attorney and their insurer’s beneficiary form. Alignment matters because the policy contract controls payout instructions.

- Trust As Beneficiary. A properly drafted trust can control timing, allowed uses, and who manages the money.

- Custodial Account Under State Law. UTMA or UGMA arrangements may allow a custodian to manage funds until the child reaches the statutory age.

- Adult Guardian With Written Plan. Some families name a trusted adult beneficiary and document expectations, though this relies on that person’s follow through.

Each option has tradeoffs in cost, flexibility, and control. A short review now can prevent a long legal process later.

How Beneficiary Designations Interact With Your Estate Plana?

Life insurance beneficiaries are usually separate from your will. If the beneficiary is properly named, the insurer pays directly to them, and the proceeds typically do not flow through probate.

However, estate planning still matters because beneficiary decisions can conflict with other documents. Consistency across your accounts, retirement plans, and insurance policies reduces confusion for survivors.

- Will. Often does not override a valid beneficiary form for life insurance.

- Trust documents. Must match the beneficiary naming format the insurer requires.

- Divorce orders. Court orders can affect who must remain the beneficiary in some situations.

If you are unsure, request a copy of your current beneficiary confirmation from your insurer. Keeping records helps avoid surprises during a claim.

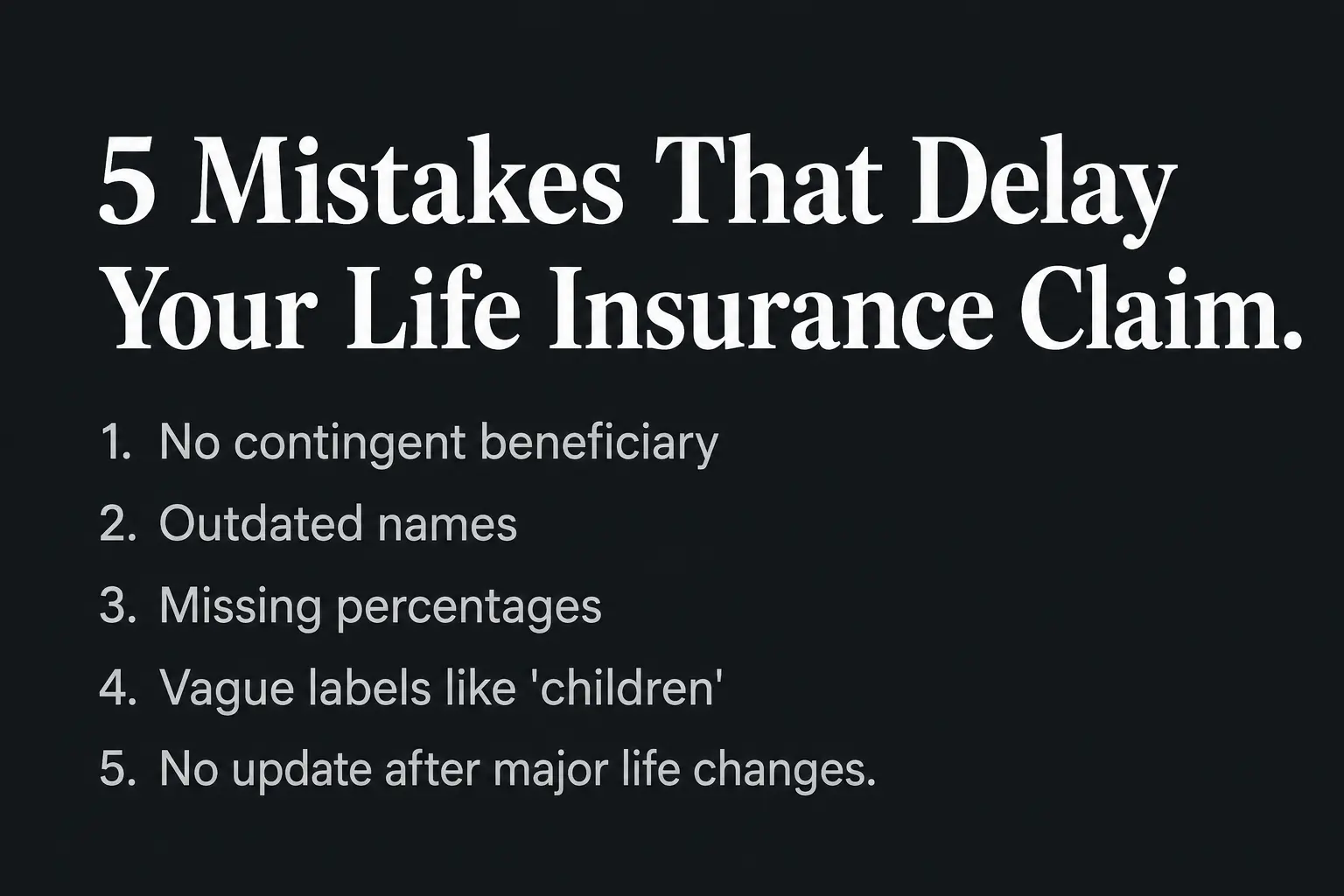

Common Beneficiary Mistakes That Cause Delays

Most claim delays are not caused by the insurer. They usually come from unclear or outdated beneficiary information, or from missing documentation that is needed to verify identity and eligibility.

A quick audit of your designation can eliminate many of these issues. Focus on clarity, completeness, and backup planning.

- No contingent beneficiary. If the primary beneficiary cannot receive the benefit, the claim may route to the estate.

- Outdated names. Marriage or divorce can leave a mismatch between legal name and the policy record.

- Missing percentages. Multiple beneficiaries without percentages can require carrier interpretation or default rules.

- Using vague labels. Terms like children or heirs can be unclear and create disputes.

- Not updating after major changes. A new child, death, or remarriage should trigger a review.

After you fix issues, confirm the update in writing. It is also wise to store the confirmation with your other important documents.

Beneficiary Types and Payout Outcomes

Beneficiary choices shape both speed and control of payout. The table below summarizes how primary, secondary, and minor beneficiary situations commonly affect the claim process.

| Beneficiary Setup | What Happens At Claim Time | Common Risk To Watch |

|---|---|---|

| Single Primary Adult | Insurer pays directly after required documents are approved | Delay if name or ID details do not match records |

| Multiple Primary Adults With Percentages | Insurer splits proceeds based on stated shares | Dispute if percentages are missing or unclear |

| Primary Plus Secondary Beneficiary | Secondary receives proceeds if primary cannot receive | Outdated secondary designation after life events |

| Minor Named Directly | Court process may be required before funds are released | Higher cost, longer timeline, and less control |

Use this summary as a checklist when you review your policy records. Small adjustments often create big improvements in speed and certainty.

How To Choose Primary and Secondary Beneficiaries?

Start with your core intent for the death benefit. Many people aim to replace income, cover debt, or provide stability for dependents, and the best beneficiary structure supports that intent.

Then focus on clarity and resilience. A good setup works even if a beneficiary dies first, changes their name, or becomes difficult to locate.

- List Your Priority Recipients. Identify who should receive funds first and why, then decide if one person or multiple recipients fit your plan.

- Add Backup Recipients. Name at least one contingent beneficiary to reduce the chance of an estate payout and probate delays.

- Assign Percentages Clearly. Use exact shares for each beneficiary and confirm the total equals 100 percent.

- Confirm Legal Names And Details. Match spelling, full legal name, and relationship information to avoid claim verification problems.

- Plan For Minors Properly. Use a trust or other permitted structure if you want funds to support a child without court involvement.

Once your choices are set, request written confirmation from the insurer. A designation is only effective when it is accepted and recorded.

When To Review and Update Your Beneficiaries?

Beneficiary reviews work best when they are routine. A simple schedule reduces the risk that old information stays on file for years.

Review your beneficiary designations after key life events, or at least during annual financial checkups. Keep your contact details current so the insurer can reach beneficiaries if needed.

- Marriage or divorce. Confirm the intended recipient and update names and relationships.

- Birth or adoption. Reassess percentages and backup plans for children.

- Death of a beneficiary. Replace them promptly and confirm the change is recorded.

- Large asset or debt changes. Adjust coverage goals and align beneficiary structure accordingly.

Frequent, small updates are easier than a major correction during a stressful claim. Keeping documentation organized supports a smoother payout.

Conclusion

Primary beneficiaries receive the life insurance payout first, and secondary beneficiaries protect your plan when the primary designation cannot work. Minor beneficiaries add legal complexity, so it is often better to use a trust or other approved structure to manage timing and control.

A clean beneficiary setup is clear, current, and resilient to life changes. Review your designations regularly, confirm they are accepted by the insurer, and keep records where your family can find them.