Buying life insurance is a smart step toward protecting your family’s future, but many people stop at the basic policy and never look deeper into the details. One of the most overlooked parts of coverage is understanding life insurance policy riders explained clearly and simply.

Riders are optional add-ons that can strengthen your policy and make it better suited to your personal needs. They can provide extra protection during illness, disability, accidents, and other unexpected life events.

Without understanding life insurance policy riders explained, many policyholders miss valuable benefits that could make a major difference later.

This guide breaks down the fine print so you can make smarter decisions and choose coverage that truly works for your life.

💡 What Are Life Insurance Policy Riders?

Before diving deeper into life insurance policy riders explained, let’s start with the basics.

A rider is an optional feature you can add to your life insurance policy for extra protection. Think of it like customizing your insurance plan based on your lifestyle, financial goals, and family responsibilities.

Instead of relying only on the standard death benefit, riders help cover special situations such as:

- Serious illness

- Disability

- Accidental death

- Long-term care needs

- Premium payment protection

- Child or spouse coverage

This is why understanding life insurance policy riders explained is so important before buying a policy.

🛡️ Why Life Insurance Policy Riders Explained Matters

Many people focus only on premiums and coverage amounts, but the real strength of a policy often comes from the riders attached to it.

Knowing life insurance policy riders explained helps you:

- Avoid financial gaps in coverage

- Customize protection for your family

- Prepare for unexpected health issues

- Improve long-term financial planning

- Get more value from your insurance investment

Sometimes a small additional premium can create major protection.

That is why riders deserve serious attention.

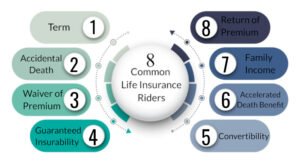

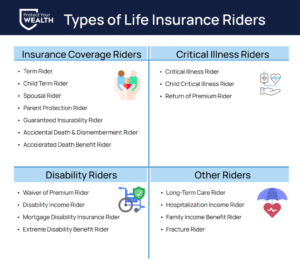

❤️ Common Life Insurance Policy Riders Explained

Let’s look at the most popular examples of life insurance policy riders explained in practical terms.

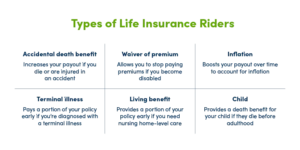

Critical Illness Rider

A critical illness rider provides a lump sum payment if you are diagnosed with a serious illness such as:

- Cancer

- Heart attack

- Stroke

- Kidney failure

- Major organ transplant

This money can help cover treatment costs, income loss, or recovery expenses.

For many families, this rider creates powerful financial relief during medical emergencies.

This is one of the most valuable examples of life insurance policy riders explained.

Disability Income Rider

If an illness or injury prevents you from working, a disability income rider can provide regular income support.

This helps cover:

- Monthly bills

- Mortgage payments

- Living expenses

- Family responsibilities

Since income loss can happen before death, this rider protects your financial stability during life—not just after it.

That makes it a key part of life insurance policy riders explained.

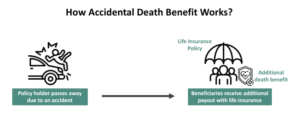

Accidental Death Benefit Rider

This rider provides an additional payout if death occurs because of an accident.

For example:

If your base life insurance policy offers $500,000 and the accidental death rider adds another $500,000, your family may receive a total of $1,000,000.

500,000+500,000=1,000,000500{,}000 + 500{,}000 = 1{,}000{,}000

This rider can be especially useful for people in high-risk professions or frequent travelers.

It is another important part of life insurance policy riders explained.

Waiver of Premium Rider

A waiver of premium rider allows you to stop paying premiums if you become permanently disabled and cannot work.

Your policy remains active even if your income stops.

This prevents the risk of losing life insurance coverage during financial hardship.

It is often one of the smartest options in life insurance policy riders explained because it protects your protection itself.

Child Term Rider

This rider provides temporary life insurance coverage for your children under a single parent policy.

While difficult to think about, it can help cover:

- Funeral expenses

- Medical costs

- Emergency family support

It offers affordable peace of mind for parents and is often included in life insurance policy riders explained discussions.

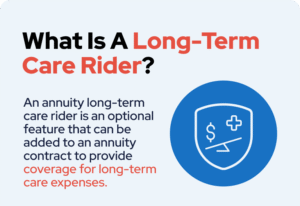

Long-Term Care Rider

Some policies allow you to access part of your death benefit early if you need long-term care due to serious illness or aging.

This can help pay for:

- Nursing care

- Assisted living

- Home healthcare

- Extended medical support

This rider adds living benefits to traditional life insurance and is becoming increasingly popular.

👨👩👧👦 How to Choose the Right Riders

Understanding life insurance policy riders explained is only the first step. The next step is choosing the right ones for your life.

Ask yourself:

- Do I have dependents who rely on my income?

- Would a serious illness create major financial stress?

- Do I work in a high-risk job?

- Do I need disability protection?

- Would long-term care planning help my retirement strategy?

The best riders depend on your real-life risks—not just what sounds good on paper.

💰 Are Riders Worth the Extra Cost?

One of the biggest questions in life insurance policy riders explained is whether riders are worth paying for.

The answer depends on value, not just price.

A small increase in monthly premium may provide:

- Large emergency financial support

- Protection during illness

- Long-term family security

- Better retirement planning options

Compared to the financial risk of being unprepared, riders are often extremely cost-effective.

The key is choosing useful riders—not unnecessary ones.

🔍 Comparing Policies Before You Buy

Not every insurance company offers the same riders.

A strong understanding of life insurance policy riders explained should include comparing:

- Rider availability

- Premium costs

- Policy flexibility

- Eligibility rules

- Waiting periods

- Claim conditions

Before making a final decision, compare trusted providers carefully.

If you want help exploring policies and rider options, visit

👉 https://quotemaestro.com/

This helps simplify the process and makes choosing the right policy easier.

Final Thoughts: The Fine Print Can Make the Biggest Difference

Most people focus on the main life insurance policy.

Smart buyers also focus on the details.

Understanding life insurance policy riders explained helps you move beyond basic protection and build stronger financial security for your family.

Riders turn standard coverage into personalized protection.

They help prepare for illness, accidents, disability, and life’s unexpected challenges.

Sometimes the smallest line in the fine print creates the biggest peace of mind.

That is why understanding riders matters so much.

❓ FAQs About Life Insurance Policy Riders Explained

1. What are life insurance policy riders explained in simple terms?

Life insurance policy riders explained means understanding optional add-ons that improve your policy by providing extra protection for illness, disability, accidents, and other special situations.

2. Which rider is most important in life insurance policy riders explained?

It depends on your needs, but common important riders include critical illness, disability income, waiver of premium, and accidental death benefit riders.

3. Do riders increase policy cost?

Yes, most riders add a small extra premium, but they can provide significant financial value and stronger long-term protection.

4. Is the waiver of premium important in life insurance policy riders explained?

Yes. It helps keep your policy active if you become disabled and cannot afford premium payments.

5. Can I add riders later to my life insurance policy?

Some insurers allow riders to be added later, but many are easier and cheaper to include when you first buy the policy.

6. Where can I compare life insurance policy riders explained and policy options?

You can compare trusted providers and rider options by visiting

👉 https://quotemaestro.com/

This helps you choose stronger and smarter life insurance protection.