Child life insurance is a life insurance policy purchased on a child, with the parent or guardian as the policy owner. It pays a death benefit if the insured child dies while the policy is active and it can sometimes build cash value over time.

The goal is usually protection for unexpected costs and the option to keep coverage as the child grows. Understanding how these policies are structured helps you decide whether they fit your family plan.

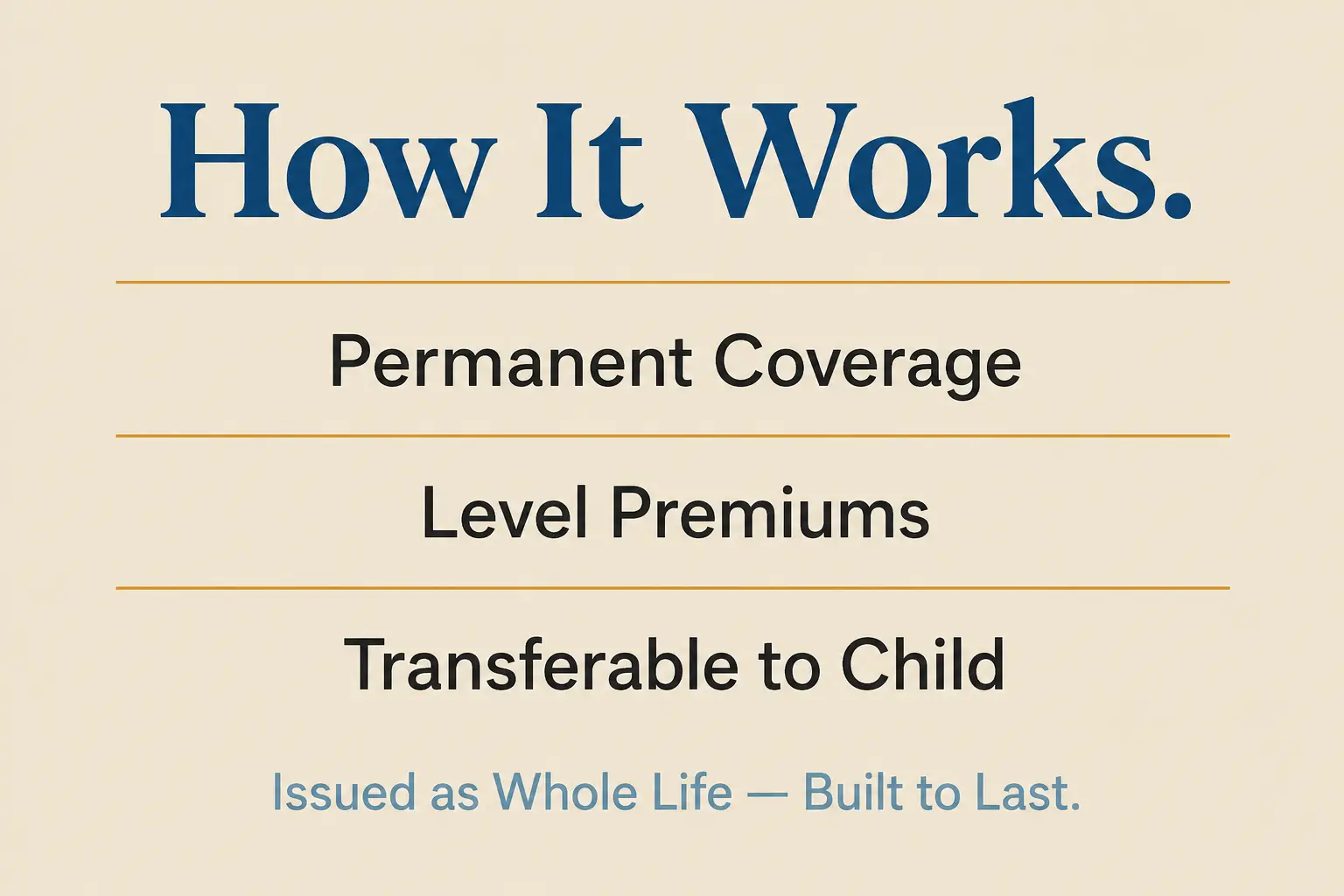

How Child Life Insurance Works?

Most child life insurance is permanent coverage, often whole life, issued with smaller face amounts than adult policies. Premiums are typically level, meaning the cost stays the same as long as you keep paying on schedule.

In many contracts, the policy can be transferred to the child when they reach adulthood. Some policies also guarantee the option to buy more coverage later without new medical underwriting.

Common Policy Features

Child policies vary by insurer, but several features show up often. Reading the policy summary and the full contract matters because small details can change the value.

- Small death benefit. Coverage is often designed to handle final expenses and related costs rather than replace income.

- Level premiums. Payments are usually fixed, which can make budgeting predictable.

- Cash value component. Some policies build a savings-like value that grows slowly and may be accessed under rules and fees.

- Guaranteed insurability options. Certain contracts allow future increases at set ages or life events.

Once you know which features are included, you can compare them against what your household actually needs.

Types of Child Life Insurance

Child coverage is commonly offered in two formats. The differences affect long-term cost, flexibility and what happens if the child develops health conditions later.

Child Rider On a Parent Policy

A child rider is an add-on to a parent’s life insurance policy that covers children for a small amount. It is often inexpensive and may cover multiple children under one rider, depending on insurer rules.

The rider typically ends at a set age and some insurers allow conversion to a permanent policy. Conversion terms and pricing are contract-specific, so it is important to verify them before buying.

Standalone Whole Life Policy For a Child

A standalone child whole life policy is its own permanent contract with a fixed premium and a cash value feature. It can be kept for life as long as premiums are paid and ownership can be transferred later.

This route usually costs more than a rider, but it may offer stronger guarantees. The tradeoff is tying up dollars that could be used for other priorities.

Pros of Child Life Insurance

Child life insurance can solve a few specific problems well. The benefit depends on your goals, the policy type and whether you already have strong protection elsewhere.

- Helps with unexpected expenses. A death benefit can offset funeral costs, time away from work and counseling or travel needs.

- Locks in insurability. Some policies allow future coverage increases even if health changes later.

- Provides lifelong coverage. Permanent policies can remain in force into adulthood with consistent premiums.

- Creates a modest cash value. Cash value can act as a conservative asset, though growth is often slow.

These advantages are most meaningful when they align with a clear financial plan, not just a general desire to do something for your child.

Cons and Risks To Consider

The drawbacks often come down to opportunity cost and expectations. Many families discover that the same monthly budget could strengthen protections that matter more.

- Lower priority than adult coverage. If a parent dies, the financial impact is usually far larger than the loss of a child’s future income.

- Cash value may underperform alternatives. Returns can be modest after fees and early surrender may produce less than you paid in.

- Long commitment. Permanent policies reward long holding periods and cancelling later can be costly.

- Potential for overselling. Some sales pitches frame it as an investment, which can lead to unrealistic expectations.

These risks do not mean child life insurance is always a poor choice. They mean it should be bought for the right reasons and with full clarity.

What It Typically Covers and What It Does Not?

A child life policy pays when the insured child dies, assuming premiums are current and the claim meets policy conditions. It does not pay for medical bills, disability, or routine childhood needs.

Coverage also does not replace the protections created by health insurance, emergency funds, or income replacement planning for parents. Keeping the purpose narrow helps prevent disappointment later.

How To Evaluate a Policy Offer?

Choosing child life insurance is less about finding a trendy product and more about making the math and the guarantees work. A good evaluation compares cost, contract terms and what you give up by funding it.

- Confirm the need. Identify the specific risk you are covering, such as final expenses or guaranteed future insurability.

- Compare rider versus standalone. Check cost differences, conversion rights and how long coverage lasts.

- Review guarantees in writing. Verify premium schedule, guaranteed cash value table and any insurability options.

- Check fees and access rules. Ask how loans, withdrawals and surrender charges work and how they affect the death benefit.

- Prioritize core protections first. Ensure parents have adequate term life and disability coverage before allocating extra dollars.

After this review, the decision is usually clearer because you are choosing between defined tradeoffs rather than marketing claims.

Child Life Insurance Versus Common Alternatives

Many families want to protect their child and also build a stronger financial foundation. Alternatives may deliver more flexibility or higher expected growth, depending on your risk tolerance and time horizon.

| Option | Primary Purpose | Main Tradeoff |

|---|---|---|

| Child Life Insurance | Death benefit plus potential lifelong coverage | Higher long-term cost and slower cash value growth |

| Child Rider On Parent Policy | Low-cost basic coverage for children | Lower benefit amount and coverage may end at a set age |

| Emergency Fund | Cash for unexpected expenses | Requires discipline and does not create insurance benefits |

| Education Savings Account | Save for school with structured contributions | Funds are earmarked and may have limits or restrictions |

Choosing among these options is easier when you separate protection goals from savings goals and fund each with the right tool.

Alternatives That Often Make Sense First

If your priority is household stability, certain moves typically provide more immediate impact than a child whole life policy. These options can be combined and they often cost less per unit of real protection.

- Term life insurance for parents. Adequate coverage can replace income, pay debts and fund childcare if a parent dies.

- Disability insurance. Protects against income loss from illness or injury, which is statistically more likely than early death.

- High-deductible planning and emergency savings. Cash reserves can cover deductibles, travel and time off work without borrowing.

- Education-focused savings. Structured saving for school can target a goal more directly than building insurance cash value.

- Custodial accounts and diversified investing. Flexible, long-term investing can be more growth-oriented, with risk managed through time and diversification.

Once these foundations are strong, child life insurance can be evaluated as a supplemental choice rather than a substitute.

When Child Life Insurance Can Be a Reasonable Fit?

Child life insurance tends to be most practical in narrow situations. It can be considered when parents have already secured their own coverage and want a small permanent policy for guaranteed future access.

It may also fit families who value a fixed premium and a conservative cash value feature and who expect to keep the policy for decades. The key is buying a benefit you would still want even if cash value growth is modest.

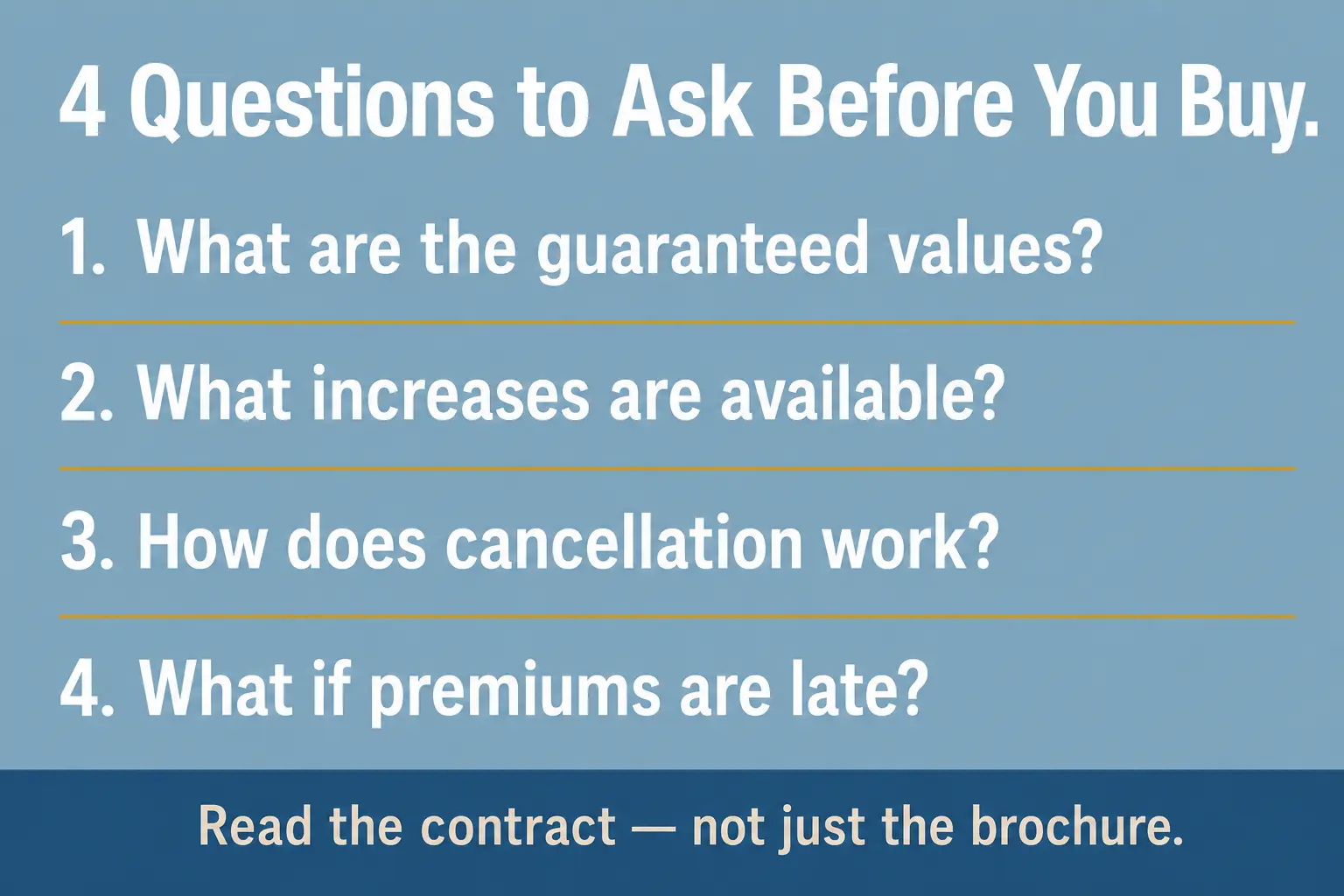

Key Questions To Ask Before You Buy

Good questions reduce regret and make comparisons fair. Ask for written answers and review the policy schedule, not only marketing materials.

- What are the guaranteed values? Confirm guaranteed cash values and death benefit guarantees, separate from non-guaranteed projections.

- What increases are available? Identify dates, amounts and rules for guaranteed purchase options.

- How does cancellation work? Check surrender charges, surrender value and how long they apply.

- What happens if premiums are late? Understand grace periods, automatic loan provisions and lapse risk.

These questions keep the decision grounded in contract terms and household priorities.

Conclusion

Child life insurance is a policy owned by a parent or guardian that provides a death benefit on a child and may offer lifelong coverage and limited cash value. Its strengths are predictable premiums and potential insurability protections, while its weaknesses are opportunity cost and slow early value.

A solid approach is to protect the income earners first, build cash reserves and then decide whether child life insurance adds meaningful value. When it matches a clear need and the policy guarantees are understood, it can be a thoughtful supplement to a broader family plan.

FAQ’s

1. Is child life insurance worth it?

Child life insurance can be worth it for families who want a small death benefit, fixed premiums and the option to keep coverage as the child grows. However, it should usually come after parents have enough life insurance, emergency savings and basic financial protection in place.

2. What is the main benefit of child life insurance?

The main benefit is that it can lock in coverage early and may allow the child to keep life insurance into adulthood. Some policies also offer guaranteed insurability options, which can help if the child develops a health condition later.

3. Is a child rider better than a standalone child life policy?

A child rider is often cheaper and can provide basic coverage for multiple children under a parent’s policy. A standalone child life policy usually costs more but may offer permanent coverage, cash value and stronger long-term guarantees.