Family life insurance is a way to turn love and responsibility into a clear financial plan. If a parent or partner dies, a benefit can replace income, clear debts and keep a stable home.

The goal is not to predict the future. The goal is to reduce the financial shock so your spouse and children can grieve without facing immediate money decisions.

What a Policy Actually Covers?

Life insurance pays a death benefit to your chosen beneficiary after the insured person dies and the claim is approved. Most policies also include a contestability period and exclusions that are explained in the contract.

For many families, the benefit supports daily living costs, housing payments, child care, education and final expenses. It can also protect a surviving spouse from being forced to sell assets quickly.

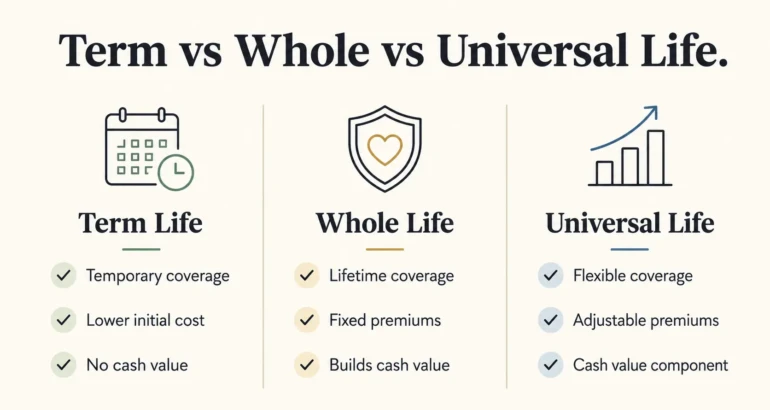

Term Life Vs Whole Life For Families

Term life insurance covers a set period and is often the most cost-effective way to buy a larger benefit during high-need years. It can match the time your children depend on your income and the years you are paying down a mortgage.

Whole life insurance is permanent coverage with a cash value component and higher premiums. It can fit families who want lifelong coverage, stable pricing and a long-term asset they can manage carefully.

| Policy Type | Best Fit For | Key Tradeoff |

|---|---|---|

| Term Life | Income replacement during child raising years | Coverage ends unless renewed |

| Whole Life | Lifelong protection and predictable premiums | Higher cost for the same death benefit |

| Universal Life | Flexible premiums and adjustable coverage | More complexity and monitoring |

| Final Expense | Small policy for burial and medical bills | Lower benefit amounts |

Once you know what each i is built to do, you can focus on the amount of coverage and how long you need it. That is where most families make the biggest gains.

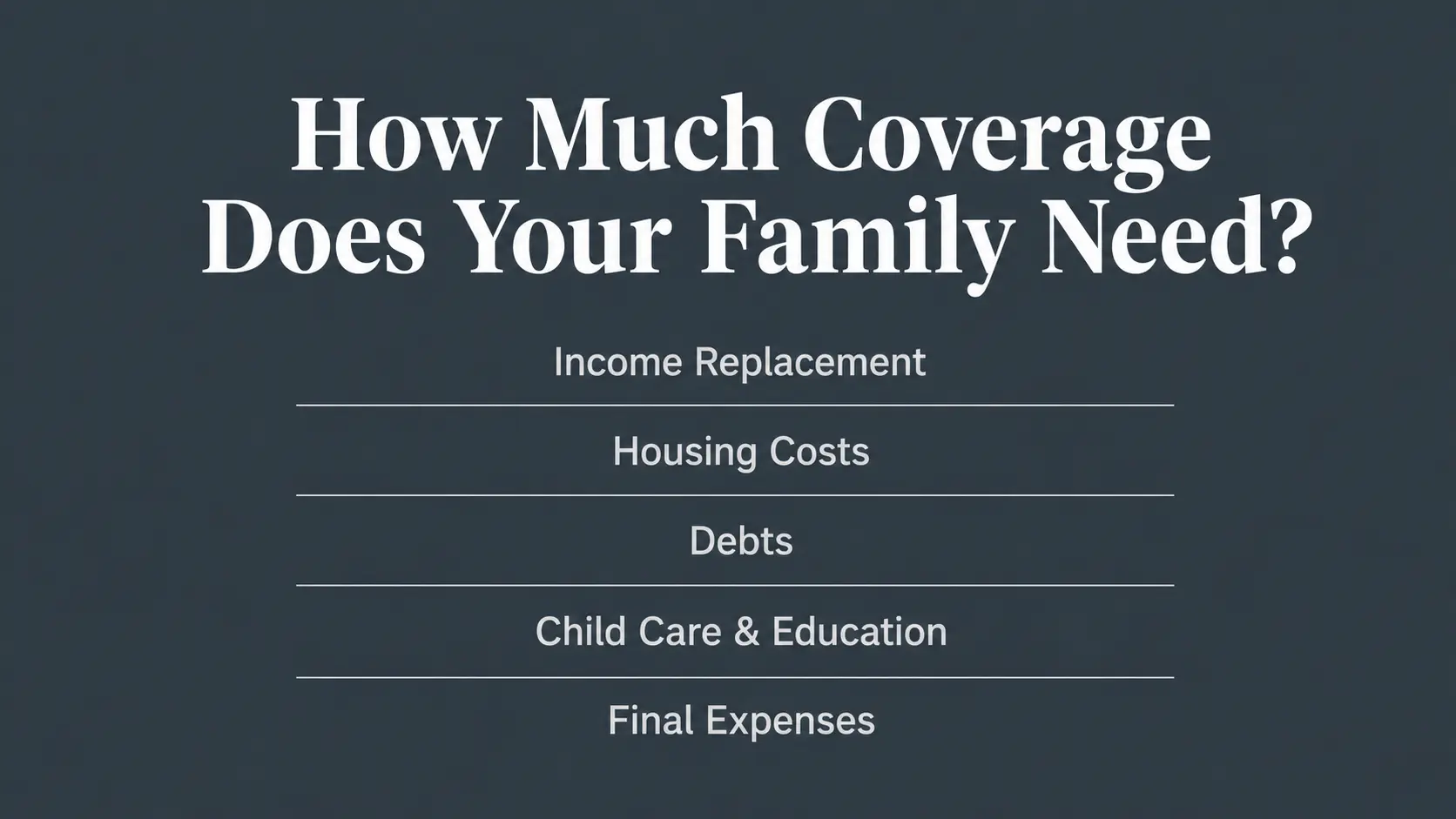

How Much Coverage Your Spouse and Children Need?

A practical method is to cover income needs, debts and family goals, then subtract resources your family already has. The right number is personal, but the process should be consistent and easy to revisit.

Focus on the financial gap your spouse would face if your paycheck stopped. Include both paid work and unpaid work you do at home that would need to be replaced.

- Income replacement. Estimate how many years your family needs support and how much monthly income your spouse would need.

- Housing costs. Include mortgage balance, rent, property taxes and repairs that would otherwise come from your income.

- Debt and obligations. Account for student loans, car loans, credit cards and any co-signed responsibilities.

- Child care and education. Add costs for care, after-school programs and education funding goals.

- Final expenses. Plan for funeral costs and medical bills that can arrive quickly.

After listing needs, look at savings, investments, employer benefits and potential survivor benefits. This helps you avoid underinsuring while also preventing you from paying for coverage you do not need.

Choosing a Beneficiary and Setting Up The Payout

Your beneficiary choice is as important as the policy itself. Most people name a spouse as primary beneficiary and name contingent beneficiaries in case the spouse dies first.

If your children are minors, consider how the benefit would be managed until they are adults. Many families use a trust or guardianship structure so the money is protected and used as intended.

- Primary and contingent beneficiaries. Keep designations current after marriage, divorce, births and deaths.

- Per stirpes and per capita choices. Understand how the benefit is divided if a beneficiary dies before you.

- Trust planning. A properly drafted trust can control timing, spending rules and oversight for minor children.

Clear beneficiary designations also reduce delays. They can help the claim process move smoothly during a stressful time.

What a Family Policy Should Include?

Many policies offer riders that can make coverage more family-friendly. Riders vary by insurer and state, so you want to confirm what is included and what costs extra.

Add-ons should solve real problems rather than add complexity. Choose features that protect your household budget and your ability to stay insured.

- Waiver of premium. Premiums may be waived if you become disabled and meet the policy terms.

- Accelerated death benefit. May allow access to part of the benefit for certain serious illnesses.

- Child rider. Can provide a small benefit for children and may be convertible later.

- Conversion option. Lets you convert term coverage to permanent coverage within set rules.

Keep the policy understandable for your spouse. If they have to manage it alone later, simplicity can be a real form of protection.

How Life Insurance Fits With Other Protection?

Life insurance works best as part of a broader safety net. Health insurance, disability insurance and an emergency fund reduce the chance that your policy is used for problems it was not designed to solve.

Disability risk is often higher than premature death risk during working years. If you are building family life insurance, consider how your income is protected if you cannot work.

- Disability coverage. Replaces part of income if illness or injury prevents work.

- Emergency savings. Covers deductibles and short-term gaps without debt.

- Estate basics. A will, guardianship choices and updated beneficiaries support the life policy.

When these pieces work together, your spouse gets options instead of pressure. That flexibility can protect your children from sudden lifestyle changes.

Common Mistakes Families Should Avoid

Most mistakes come from buying a policy and never updating it. Family needs shift as income changes, children grow and debts go down.

Another risk is relying only on employer coverage. Job changes can interrupt coverage and group plans may not be enough to protect a household long term.

- Buying too little coverage. A small policy may cover funeral costs but not replace income.

- Not covering both spouses. Stay-at-home work has real replacement costs that should be insured.

- Skipping policy reviews. Major life events can make your current amount outdated.

- Choosing the longest term by default. Match term length to when key obligations end.

A quick annual review can prevent these issues. It also helps you keep beneficiaries and contact details correct.

How To Buy The Right Policy With Confidence?

Buying life insurance becomes simpler when you treat it as a planning exercise rather than a product purchase. Decide what you want the policy to do, then compare options that meet that goal.

Use a process that your spouse can understand and repeat. That makes it easier to maintain your plan over the years.

- Set your protection goal. Decide whether you are replacing income, paying off debts, or covering multiple needs.

- Pick a coverage length. Align the term with mortgage payoff dates, child dependency and retirement plans.

- Estimate the benefit amount. Add key expenses and goals, then subtract savings and other resources.

- Compare underwriting paths. Decide between fully underwritten and simplified options based on health and timing.

- Confirm ownership and beneficiaries. Ensure the policy owner, payor and beneficiaries match your family plan.

After you choose a policy, store documents where your spouse can access them. Include the insurer name, policy number and claim instructions.

Conclusion

Family life insurance protects your spouse and children by turning a worst-day risk into a manageable financial plan. The right policy replaces income, covers major obligations and preserves stability at home.

Focus on term length, benefit amount and beneficiary setup, then review your coverage as your family changes. With a clear plan, your family gets time and space to heal without financial chaos.

Frequently Asked Questions About Family Life Insurance

1. What is the best age to buy family life insurance?

The best age to buy family life insurance is usually when you start sharing financial responsibilities, such as getting married, having children, buying a home, or depending on one income. Buying earlier can often help you get lower premiums and more coverage options.

2. Can one life insurance policy cover the whole family?

Some insurers offer family life insurance plans or riders that can cover a spouse and children under one policy. However, many families still choose separate policies for each parent because each person may have different income, responsibilities and coverage needs.

3. What happens if a life insurance beneficiary is a minor child?

If a minor child is named directly as a beneficiary, the court may need to appoint someone to manage the money until the child becomes an adult. Many families use a trust or name a responsible adult arrangement to help manage the payout properly.