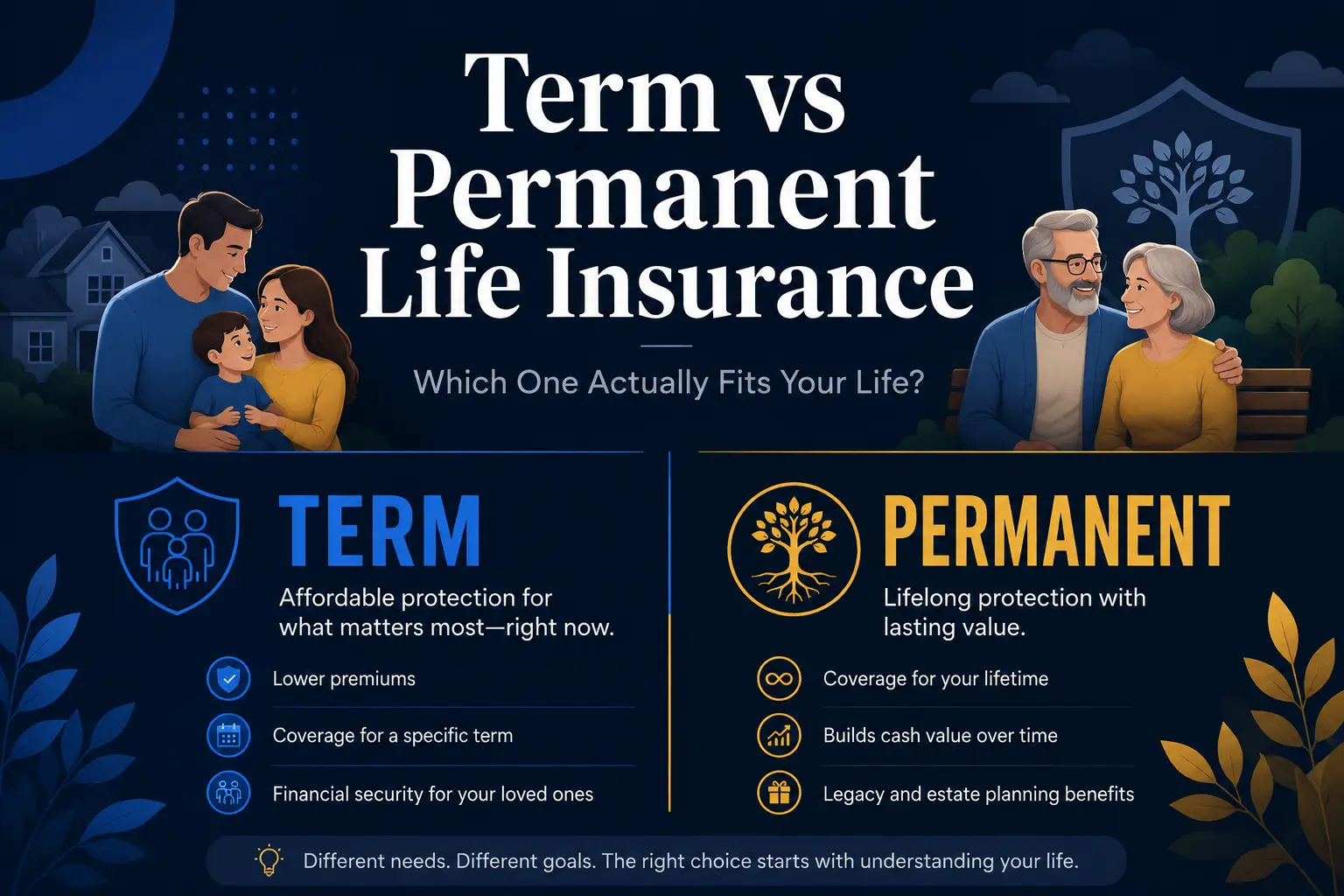

Term life insurance is a life insurance policy designed to provide financial protection for a set period of time. If the insured person dies during the term, the policy pays a death benefit to the listed beneficiaries.

Unlike permanent life insurance, term coverage is built for affordability and simplicity. You choose a coverage amount and a term length, keep premiums current and the protection stays in force during that window.

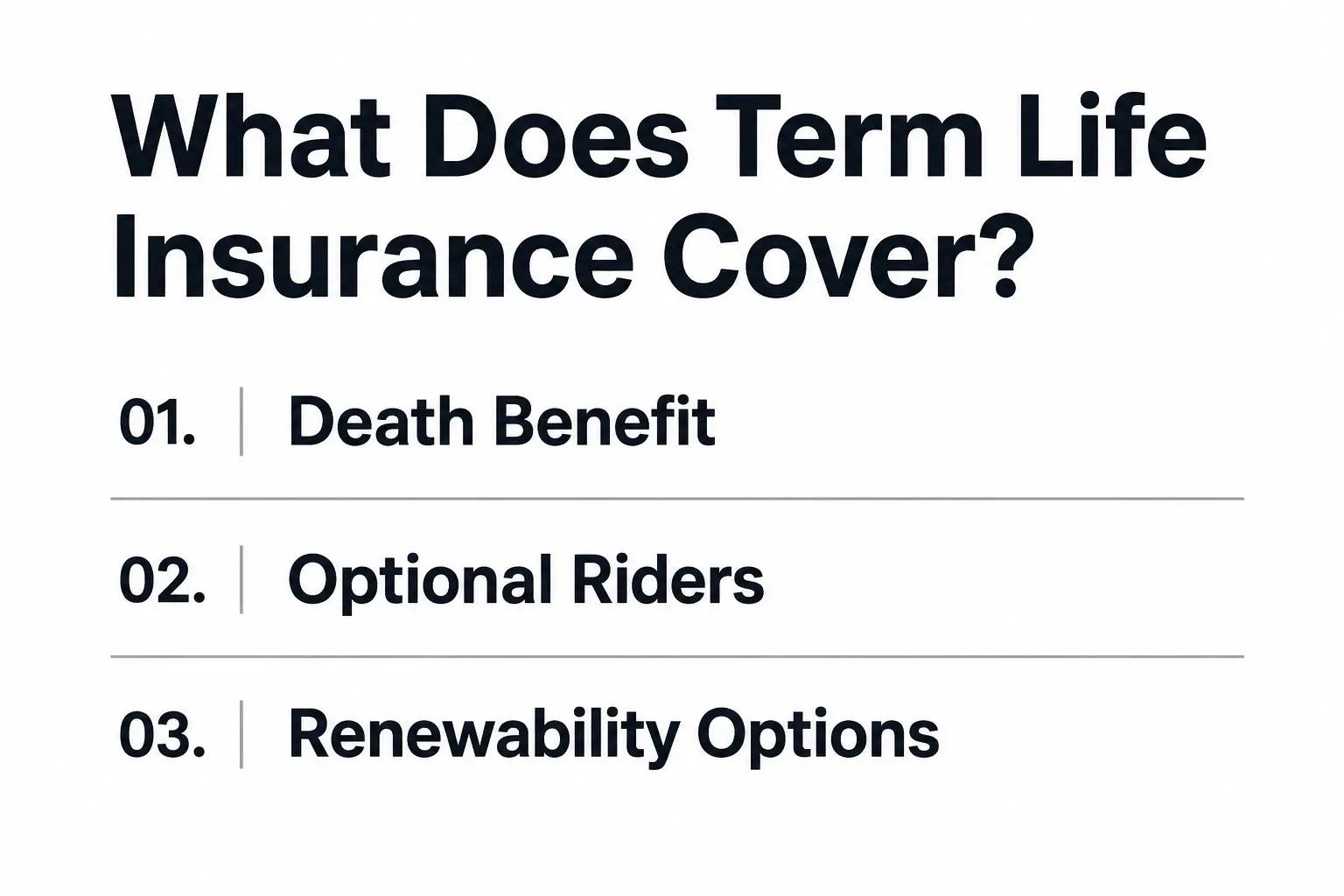

What Term Life Insurance Covers?

Term life insurance primarily covers the risk of death during the policy term. The payout is generally tax-free to beneficiaries and can be used for any purpose, including household expenses, debt payoff, or long-term financial needs.

Most policies pay a level death benefit, meaning the coverage amount stays the same throughout the term. Some options include decreasing term life insurance, where coverage reduces over time, often aligned to a declining loan balance.

- Death benefit. A lump-sum payment to beneficiaries if death occurs while the policy is active.

- Optional riders. Add-ons such as accelerated death benefit, waiver of premium, or child term riders may be available depending on the insurer.

- Renewability options. Some policies allow renewal after the term, usually at a higher premium based on attained age.

These features shape how flexible a policy feels, but the core purpose remains straightforward protection during a defined timeframe.

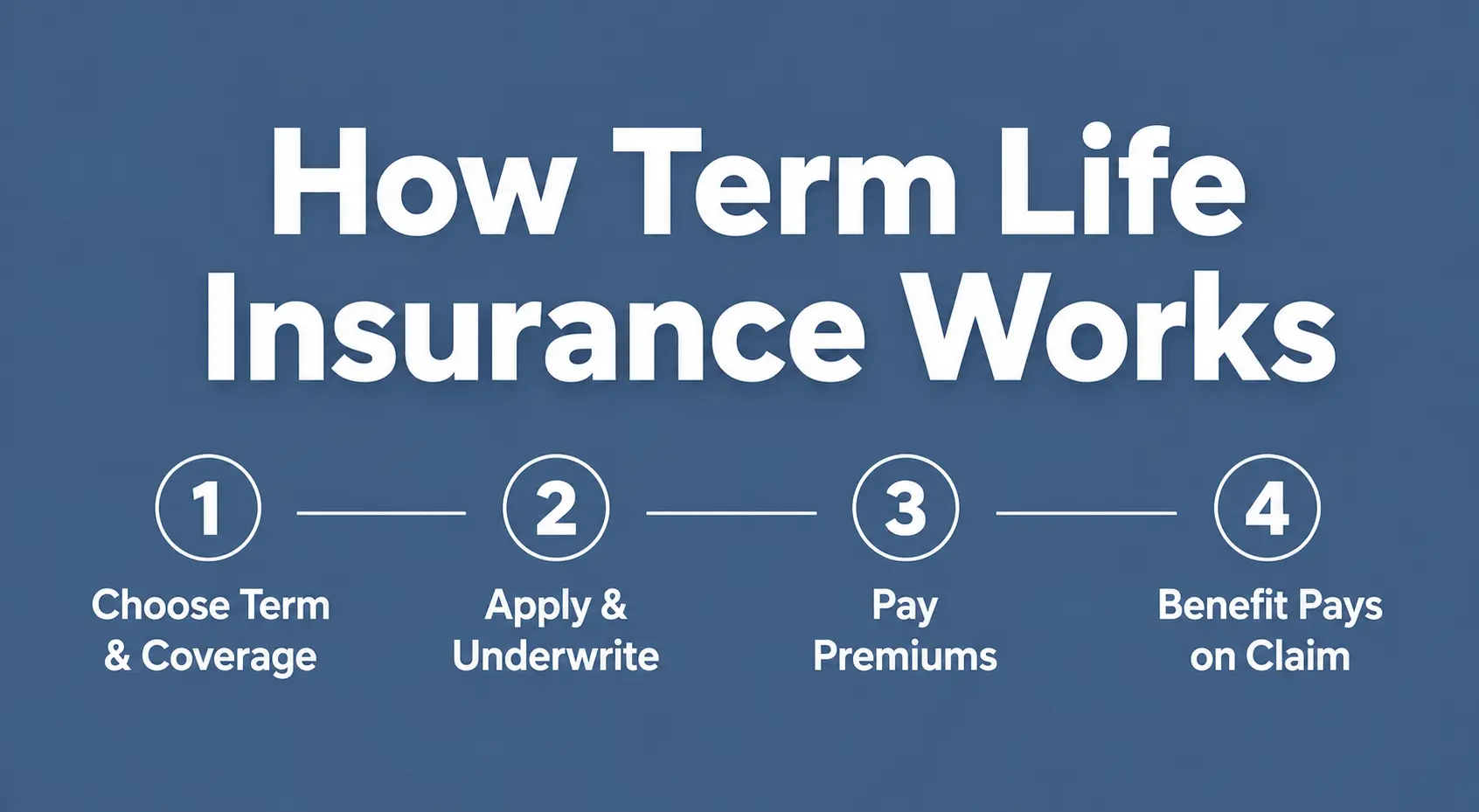

How Term Life Insurance Works in Practice?

Term life insurance works by pooling risk across many policyholders. You pay premiums to the insurer and the insurer agrees to pay the death benefit if a covered death occurs during the term.

Your premium is based on underwriting, which is the insurer’s process for evaluating risk. Health history, age, nicotine use, occupation, driving history and the requested coverage amount all affect the final rate.

- Choose term length and coverage. Select a policy term and face amount that match the years your household would be financially vulnerable.

- Apply and complete underwriting. Provide health and lifestyle information and complete a medical exam if required for fully underwritten policies.

- Pay premiums to keep coverage active. Maintain payments on schedule to avoid lapse and preserve the death benefit protection.

- Benefits pay if death occurs during the term. Beneficiaries file a claim and receive the payout after the insurer confirms eligibility.

Once issued, the key responsibility is keeping the policy in force and keeping beneficiary information current.

Key Term Life Insurance Terms You Should Know

Understanding policy language helps you compare options and avoid surprises. Term policies can look similar on the surface, but small contract details may change how the coverage behaves.

These are common terms that show up in quotes, policy summaries and contracts.

- Death benefit. The amount paid to beneficiaries on a covered death during the term.

- Premium. The amount you pay for coverage, often monthly or annually.

- Term length. The coverage period, such as 10, 20, or 30 years.

- Beneficiary. The person or entity that receives the payout.

- Conversion option. A feature that may allow switching to permanent coverage without a new medical exam within a stated period.

- Grace period. A short window after a missed premium in which coverage may remain active.

These definitions make it easier to evaluate a policy beyond the headline monthly price.

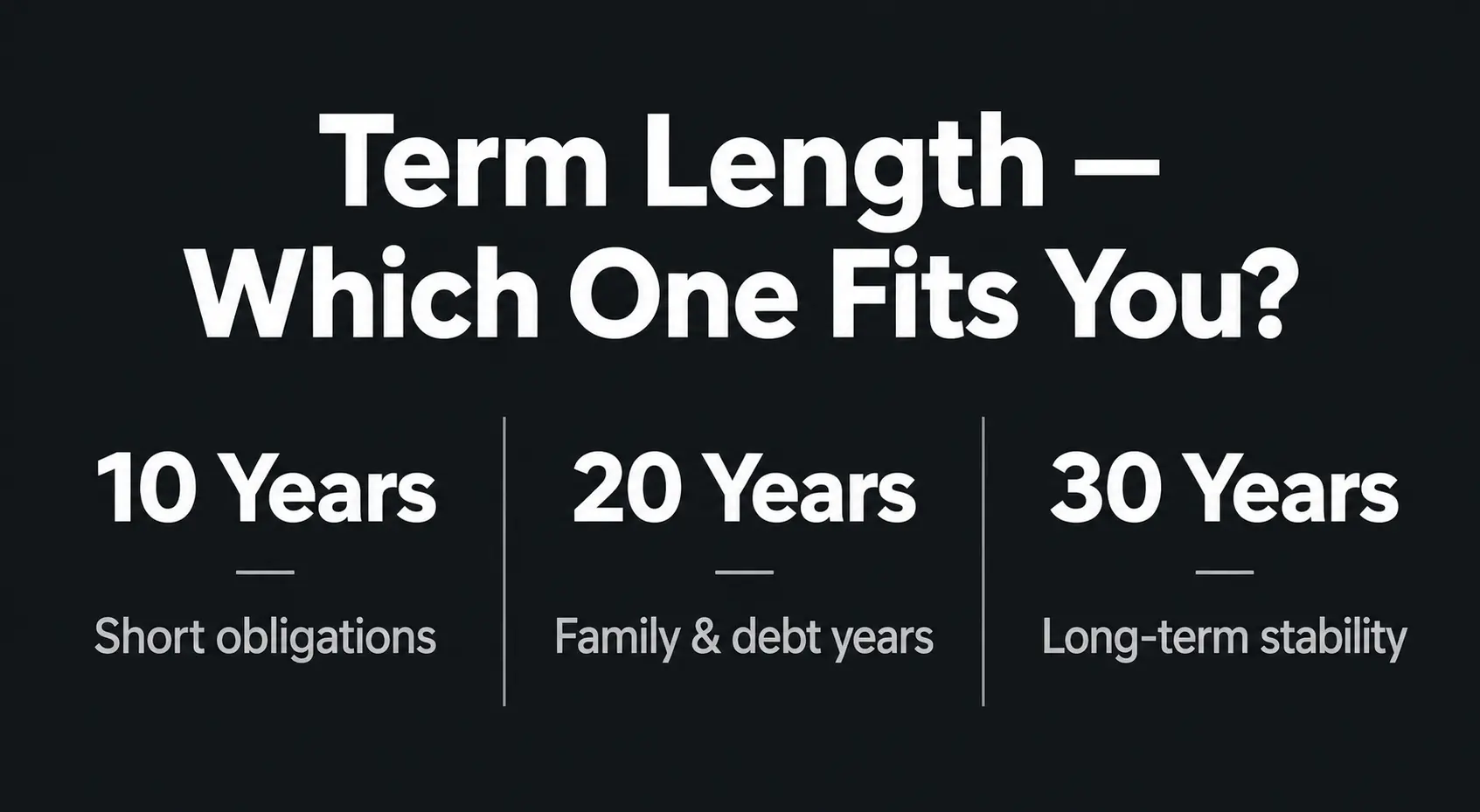

Term Length Options and How to Choose One

Term length should match the years your financial obligations are highest. Many people align coverage with mortgage duration, children’s dependency years, or the time until retirement savings are more established.

Longer terms usually cost more than shorter terms because the insurer is covering a longer risk window. Picking a term that is too short can create pressure to renew later at higher rates.

- 10-year term. Often used for short obligations or a bridge period while income rises.

- 20-year term. Common for families balancing child-rearing years and major debts.

- 30-year term. Often used when long-term budget stability is the priority.

After narrowing a term, confirm whether the policy is level term life insurance and whether it includes renewability or conversion privileges.

How Much Coverage You Might Need?

Coverage needs depend on what you want the death benefit to replace or fund. A solid approach is to add up obligations and goals, then subtract available resources such as savings or existing employer life insurance.

Focus on the costs that would be hardest for survivors to manage without your income. Keep the estimate practical so the premium fits your budget long-term.

- Income replacement. A cushion for everyday expenses and ongoing bills.

- Debt and housing. Mortgage, rent and other major balances that could strain cash flow.

- Family care. Childcare, elder care, or other support needs that may increase after a loss.

- Final expenses. Funeral and related end-of-life costs.

Once you land on a range, compare quotes at two or three coverage levels to see what keeps premiums comfortable.

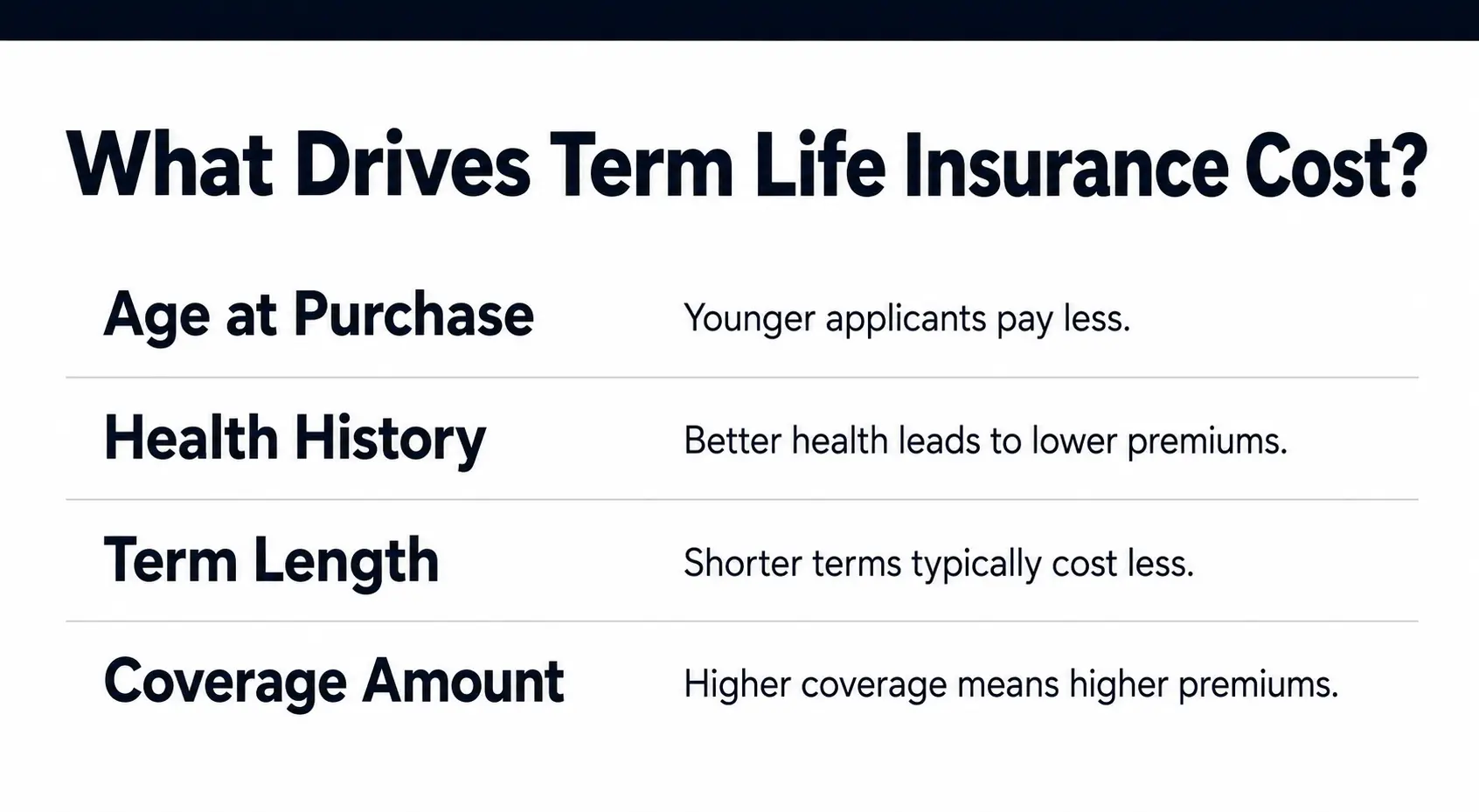

What A Term Life Insurance Policy Costs?

Pricing is driven mainly by age and health at the time you apply. Insurers also consider factors such as blood pressure, cholesterol, prescription history, build, family medical history and tobacco use.

Policy design matters too. A longer term, higher face amount and added riders generally increase premium, while shorter terms and smaller death benefits reduce cost.

| Cost Driver | Why it Matters | How to Potentially Lower Cost |

|---|---|---|

| Age At Purchase | Risk increases with age, so premiums typically rise as you get older | Apply earlier if coverage is needed and budget allows |

| Health And Medical History | Underwriting uses health data to set risk class and pricing | Manage controllable factors and provide accurate records |

| Term Length | Longer terms cover more years of risk and usually cost more | Match term to obligations rather than defaulting to the longest |

| Coverage Amount | Higher death benefits increase the insurer’s potential payout | Choose a benefit tied to needs, not a round number alone |

Beyond price, check for policy strength factors like conversion windows, renewability terms and exclusions so the coverage performs when it matters.

Medical Exam and No Exam Term Life Insurance

Some term policies require a medical exam, while others offer simplified issue or no exam underwriting. Fully underwritten policies often provide the lowest rates for healthy applicants because pricing is based on more detailed health data.

No exam options can be faster, but they may cost more due to the insurer relying on other data sources and pricing conservatively. Approval limits can also be lower compared to exam-based coverage.

- Fully underwritten. Often includes a paramed exam and lab work, with potentially better pricing for strong health profiles.

- Simplified issue. Uses health questions and databases, sometimes with quicker decisions.

- Guaranteed issue. Limited availability and typically higher cost, designed for cases where underwriting is not possible.

Choosing the underwriting path is about balancing speed, cost and the amount of coverage you need.

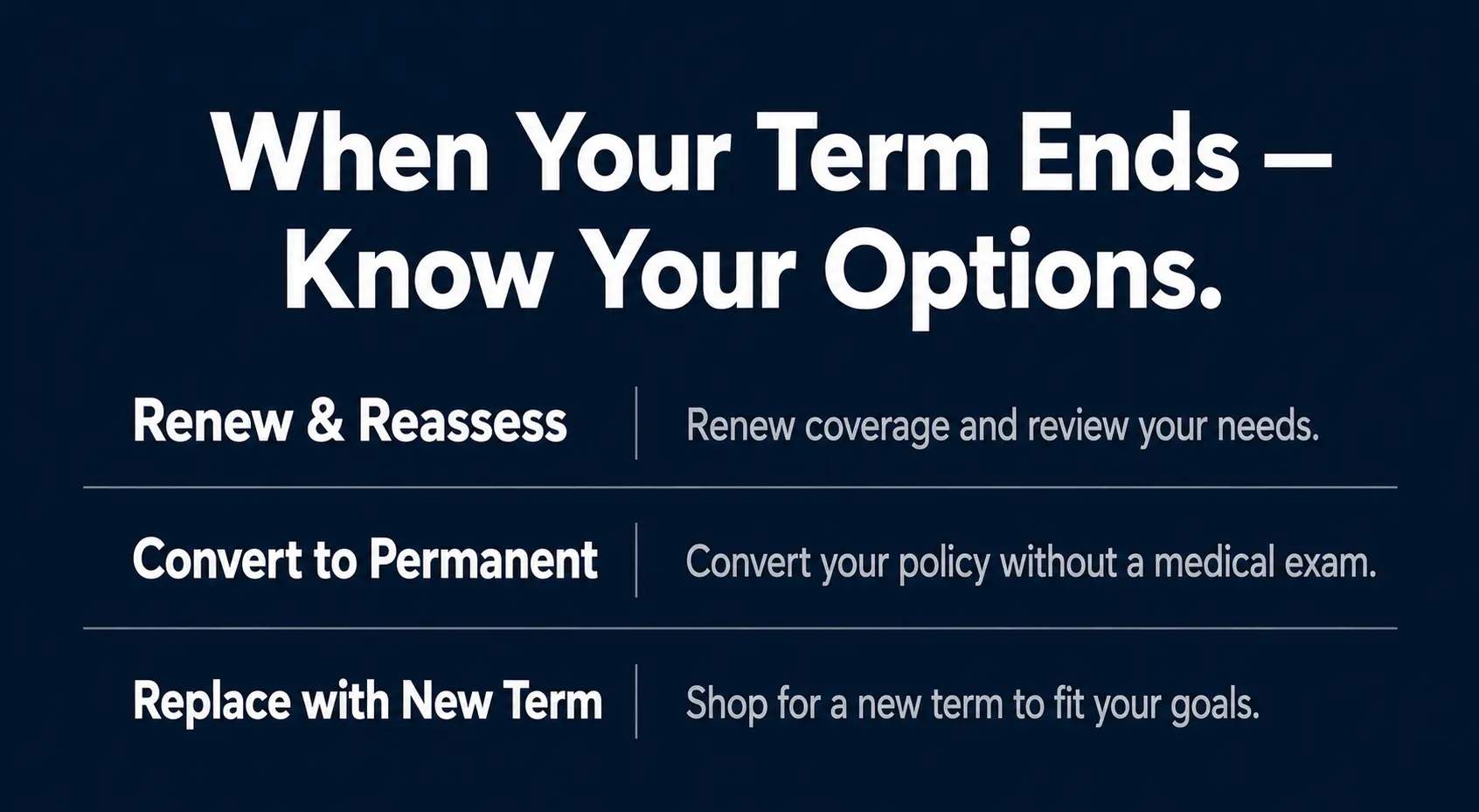

Policy Renewals, Conversion and What Happens When The Term Ends?

When a term ends, coverage typically stops unless the policy is renewed or converted. Renewal generally continues coverage year to year, but premiums usually increase sharply because pricing is based on current age.

Conversion allows a switch to permanent life insurance within the conversion period stated in the contract. Conversion can help if health changes make a new policy difficult, but permanent premiums are usually higher than term premiums.

- Renew and reassess. Useful for short-term needs, but review the long-term cost impact.

- Convert within the allowed window. Helpful when lifetime coverage becomes necessary due to estate or dependent care planning.

- Replace with a new term policy. Consider if health and age still support favorable underwriting.

Reading the renewal and conversion language before you buy makes the end-of-term decision far less stressful.

Common Exclusions and Claim Considerations

Term life insurance pays most claims, but exclusions and contestability rules matter. Many policies include a suicide exclusion for a limited initial period and may deny claims for material misrepresentation on the application.

The contestability period is a set time after the policy starts when the insurer can investigate application details more closely. Accurate disclosure and consistent medical history reporting reduce the chance of claim delays.

- Contestability period. Claims may be reviewed for application accuracy early in the policy term.

- Suicide exclusion. Typically limited to the first years as stated in the contract.

- Material misrepresentation. Incorrect or withheld information can affect claim approval.

Clear paperwork and honest application answers help ensure the death benefit reaches beneficiaries smoothly.

How to Compare Term Life Insurance Quotes?

Comparing quotes is more than lining up monthly premiums. Two policies with the same face amount and term can differ on conversion options, included riders and how the insurer defines certain terms.

Focus on the details that affect long-term value and claim reliability. Look at the insurer’s financial strength and the policy contract language, not only the illustration or marketing summary.

- Same inputs. Compare quotes with the same term, coverage amount and underwriting type.

- Rate class. Verify the health class used, since it can change price dramatically.

- Conversion terms. Check deadlines, eligible products and whether partial conversion is allowed.

- Rider costs. Confirm which riders are included and which add premium.

- Payment flexibility. Review monthly versus annual billing, grace period rules and lapse protections.

This comparison approach keeps the decision focused on coverage quality and long-term fit rather than a single low price.

Conclusion

Term life insurance is a straightforward way to protect loved ones with a set coverage amount for a defined period. It works by paying a death benefit if death occurs during the term, as long as premiums are kept current.

The best policy is the one that matches your obligations, budget and timeline while offering solid contract features like conversion or renewability when needed. Careful comparison of term length, coverage amount and underwriting type helps you buy protection that stays reliable for the years you depend on it.