A life insurance premium is the amount you pay to keep a life insurance policy active. When premiums are paid on time and the policy is in force, the insurer provides the death benefit and any included policy features.

Premiums are set using underwriting, which is the insurer’s process for estimating risk and pricing coverage. Understanding how costs and payments work helps you avoid surprises and keep coverage stable over time.

Life Insurance Premium Meaning And Why It Matters

The premium is not a savings deposit or an investment contribution by default. It is the price of transferring financial risk to the insurer, based on the policy type and the insured person’s profile.

If a premium is missed and the policy lapses, coverage can end and reinstatement may require new underwriting. Keeping premiums affordable and predictable is a key part of selecting the right coverage amount and term length.

How Life Insurance Premiums are Calculated?

Insurers price premiums by combining actuarial data with individual underwriting details. The goal is to estimate the likelihood of a claim and the expected timing of that claim.

Pricing also reflects administrative costs, reserve requirements and the policy’s guarantees. Permanent policies can cost more because they may include cash value growth and lifetime coverage features.

Risk Assessment and Underwriting Basics

Underwriting evaluates medical history, lifestyle and financial suitability for the requested coverage. Some policies require a medical exam, while others use accelerated underwriting with data sources and health questionnaires.

The more uncertainty the insurer faces, the more likely pricing will increase or underwriting will request additional details. Clear and accurate information supports a smoother application and more stable pricing outcomes.

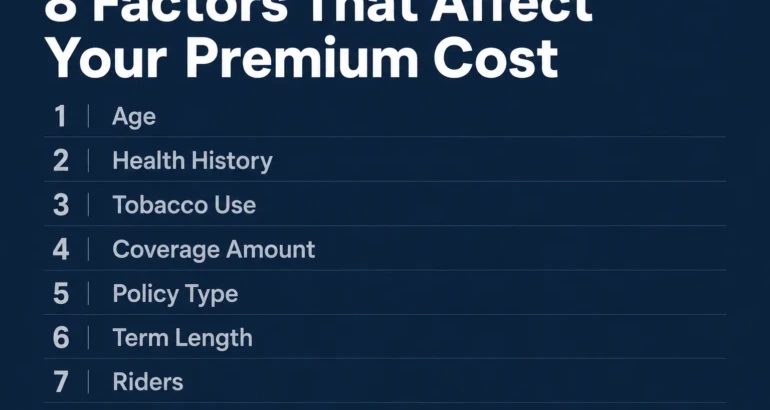

Key Factors That Affect Premium Cost

Premiums are personal, even when two people buy the same type of policy. The price reflects both the coverage design and the insured person’s risk profile.

Some factors are fixed at issue, while others can change later depending on policy structure. Reviewing these drivers helps you understand quotes and compare policies more fairly.

- Age At Application: Premiums generally rise with age because the likelihood of a claim increases over time.

- Health And Medical History: Chronic conditions, medications and past diagnoses can affect underwriting class and cost.

- Tobacco And Nicotine Use: Smoking and nicotine products often trigger higher rates, sometimes for multiple years after quitting.

- Coverage Amount: Higher death benefits usually mean higher premiums, though per-dollar cost can vary by tier.

- Policy Type: Term life tends to have lower initial premiums than whole life or universal life.

- Term Length: Longer terms can cost more because the insurer guarantees pricing for a longer period.

- Riders And Optional Benefits: Add-ons like waiver of premium or accelerated death benefit features can change the price.

- Occupation And Hobbies: Hazardous work or high-risk activities may increase premiums or limit available options.

Once you know which factors are driving a quote, you can adjust the policy design rather than guessing. That keeps changes targeted and easier to evaluate.

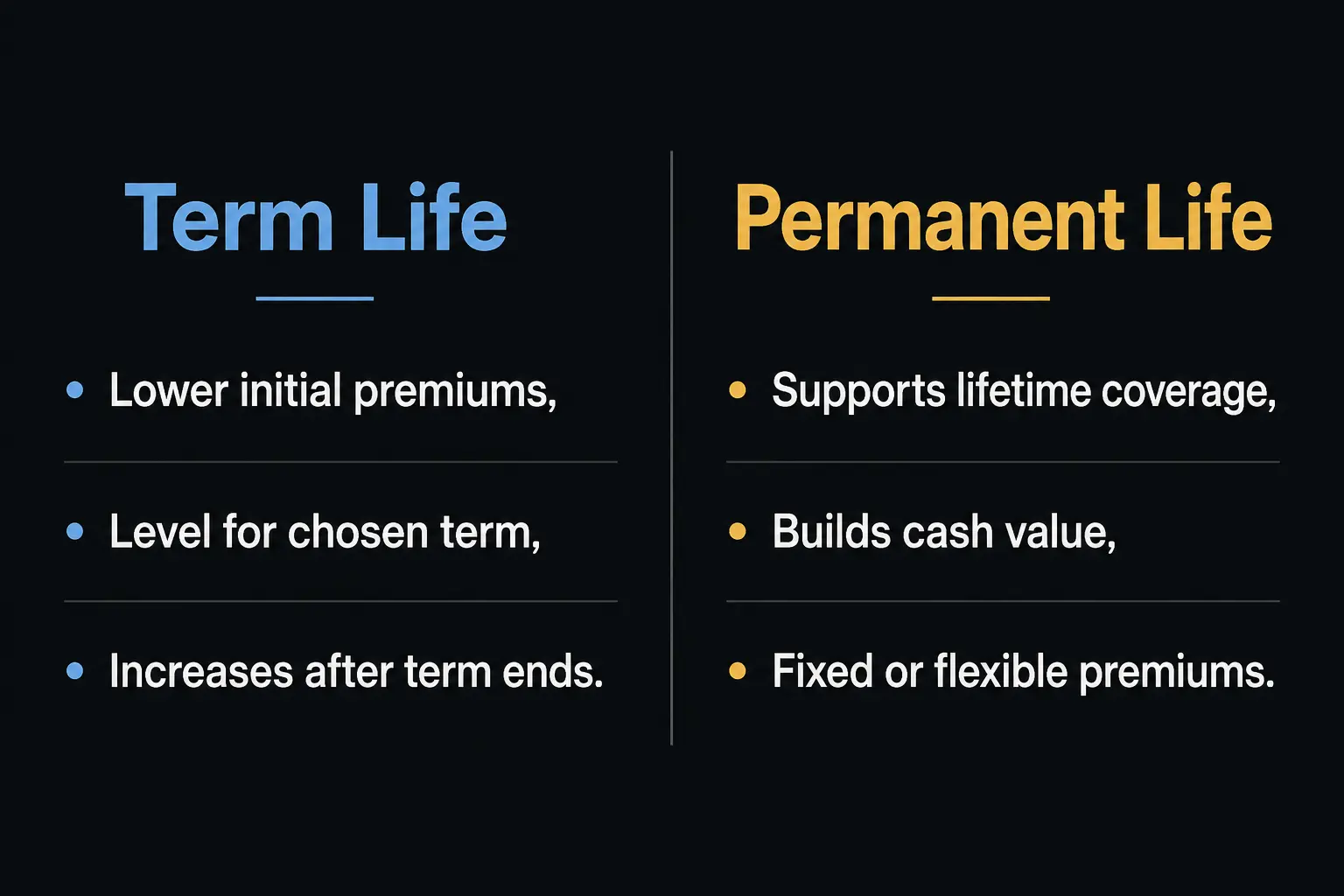

Term Life Vs Permanent Life Premiums

Term life insurance premiums are usually level for the chosen term, such as 10, 20, or 30 years. After the level period ends, premiums typically increase if coverage continues, depending on the policy’s structure.

Permanent life insurance premiums are designed to support lifetime coverage and can build cash value. Whole life often offers fixed premiums, while universal life may offer flexible premiums within policy limits and funding requirements.

Level Premiums and Increasing Premiums

A level premium means the scheduled premium stays the same during the guaranteed period. This supports budgeting and reduces the risk that cost changes will force a coverage decision later.

Increasing premium structures can start lower but may become costly over time. Understanding when increases happen and how much they can rise is important before committing to long-term coverage.

Payment Frequency and Billing Options

Premiums can usually be paid monthly, quarterly, semiannually, or annually. Paying more frequently can feel easier, but it may cost more overall due to modal factors, which are pricing adjustments for billing frequency.

Many insurers offer automatic bank draft or card payments to reduce the chance of missed payments. Some policies also allow employer payroll deduction or direct billing through an agent, depending on the carrier.

Common Payment Methods and What To Watch

Payment convenience matters because missed premiums can trigger late fees, loss of discounts, or even lapse. Choose a method that matches your cash flow and makes on-time payment simple.

- Automatic Draft: Helps prevent missed due dates, but requires monitoring for account changes or insufficient funds.

- Card Payments: Useful for tracking, but expired cards can cause failed payments if not updated quickly.

- Annual Billing: Often lowers total cost, though it requires a larger upfront payment.

- Payroll Deduction: Convenient when available, but changes in employment may require a fast switch to direct billing.

Before choosing a billing method, confirm the due date, grace period length and whether the insurer charges extra for monthly billing. Those details can affect affordability as much as the base premium.

Grace Periods, Lapse and Reinstatement

Most policies include a grace period, which is a short window after the due date when coverage may remain in force even if the premium has not been paid. If payment is made within that period, the policy continues without interruption.

If the grace period ends without payment, the policy can lapse and coverage may stop. Reinstatement may be possible, but it often requires back premiums, interest and proof of insurability.

How Discounts and Underwriting Classes Influence Pricing?

Premium quotes are typically based on an underwriting class, such as preferred, standard, or substandard ratings. Better classes usually mean lower premiums and the criteria differ across insurers.

Some carriers also offer household, electronic delivery, or multi-policy discounts. Discount rules are carrier-specific, so a lower base rate does not always mean a lower total cost.

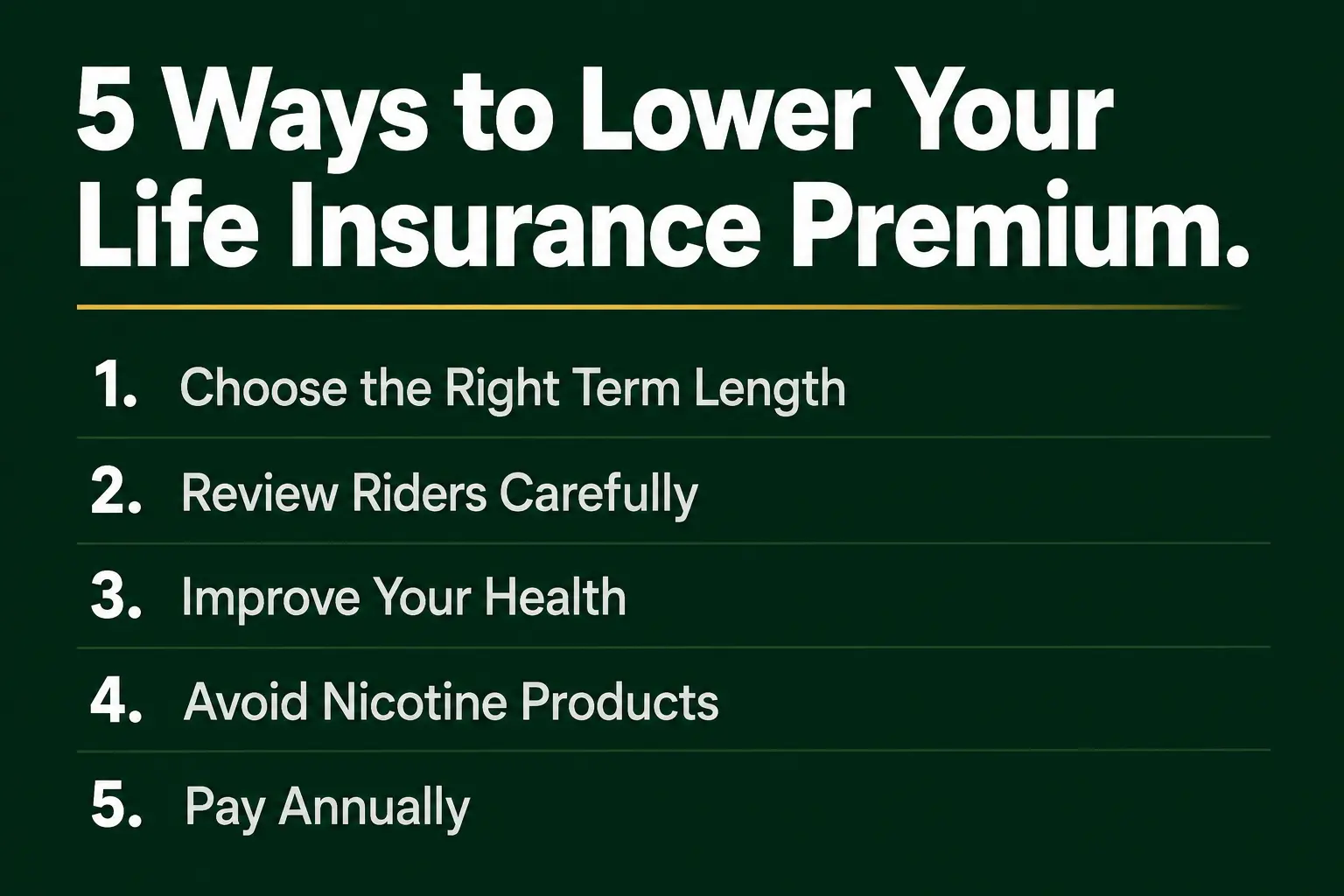

Ways To Lower Your Life Insurance Premium

Lowering a premium usually means changing either risk factors or policy design. The best approach keeps the death benefit aligned with your financial goals and avoids cutting coverage so far that it no longer protects your household.

Small design adjustments can reduce cost without sacrificing the core purpose of the policy. Comparing different term lengths and riders often reveals the biggest price differences.

- Choose An Appropriate Term Length: Match the term to major obligations like a mortgage or income replacement needs.

- Review Riders Carefully: Remove optional riders that do not support your priorities.

- Improve Health Where Possible: Managing weight, blood pressure and cholesterol can support a better underwriting class at renewal or new purchase.

- Avoid Nicotine Products: Quitting can improve eligibility for better rates over time, depending on insurer guidelines.

- Consider Annual Payments: Paying annually can reduce total cost compared with monthly billing in many cases.

After making changes, re-check that beneficiaries, coverage amount and policy ownership still match your intent. Cost should support coverage, not undermine it.

Premium Basics at A Glance

A simple comparison helps clarify what you are paying for and what can change later. Use it as a quick reference when reviewing quotes and policy documents.

| Premium Element | What It Means | What It Can Affect |

|---|---|---|

| Policy Type | Term or permanent coverage design | Price level, cash value features, duration of coverage |

| Underwriting Class | Risk rating based on health and lifestyle | Monthly cost, eligibility for preferred rates |

| Billing Frequency | Monthly, quarterly, semiannual, or annual payments | Total cost over the year and payment convenience |

| Optional Riders | Added benefits beyond the base policy | Premium amount, coverage scope, claim features |

Use the table to separate the base premium from the costs created by add-ons and billing choices. That makes it easier to compare policies on equal terms.

Conclusion

A life insurance premium is the price you pay to keep coverage active and protect the people who depend on you. The cost is driven by underwriting, policy type, coverage amount and the way you choose to pay.

Focus on a premium you can sustain for years, not just the lowest first quote. When you understand payment options, grace periods and the tradeoffs between term and permanent coverage, you can select a policy that stays in force when it matters most.