Most people assume that having health insurance automatically gives them the lowest price. Surprisingly, that’s not always true. In many cases, negotiating cash prices with insurance can actually save you money—especially for certain procedures, tests, or prescriptions.

Understanding how negotiating cash prices with insurance works can help you avoid overpaying and give you more control over your healthcare expenses.

What Is Negotiating Cash Prices With Insurance?

Negotiating cash prices with insurance means asking healthcare providers for their self-pay or “cash rate” even if you already have insurance coverage. Many providers offer discounted rates for upfront payments, which can sometimes be lower than what insurance companies negotiate.

This approach to negotiating cash prices with insurance is especially useful when:

- Your deductible hasn’t been met

- The procedure is not fully covered

- You are dealing with out-of-network providers

- The insured rate is higher than the cash rate

Why Negotiating Cash Prices With Insurance Works

There are several reasons why negotiating cash prices with insurance can lead to lower costs:

1. Avoiding Administrative Costs

Insurance billing involves paperwork, delays, and administrative overhead. Providers may offer lower prices when negotiating cash prices with insurance because it simplifies the process.

2. Immediate Payment Incentives

Doctors and hospitals often prefer immediate payment. This makes negotiating cash prices with insurance attractive because it guarantees faster cash flow.

3. Pricing Transparency

When you ask about cash rates, you often get clearer pricing. This transparency is a major benefit of negotiating cash prices with insurance.

When You Should Consider Negotiating Cash Prices With Insurance

Knowing when to use negotiating cash prices with insurance is key to maximizing savings.

✅ Before Meeting Your Deductible

If your deductible is high, you may pay out-of-pocket anyway. In this case, negotiating cash prices with insurance can reduce your total cost.

✅ For Routine or Elective Procedures

Many non-emergency services have flexible pricing, making them ideal for negotiating cash prices with insurance.

✅ For Out-of-Network Care

Out-of-network services can be expensive. Negotiating cash prices with insurance can help you avoid excessive charges.

✅ For Prescription Medications

Sometimes pharmacies offer lower cash prices than insurance copays, making negotiating cash prices with insurance worthwhile.

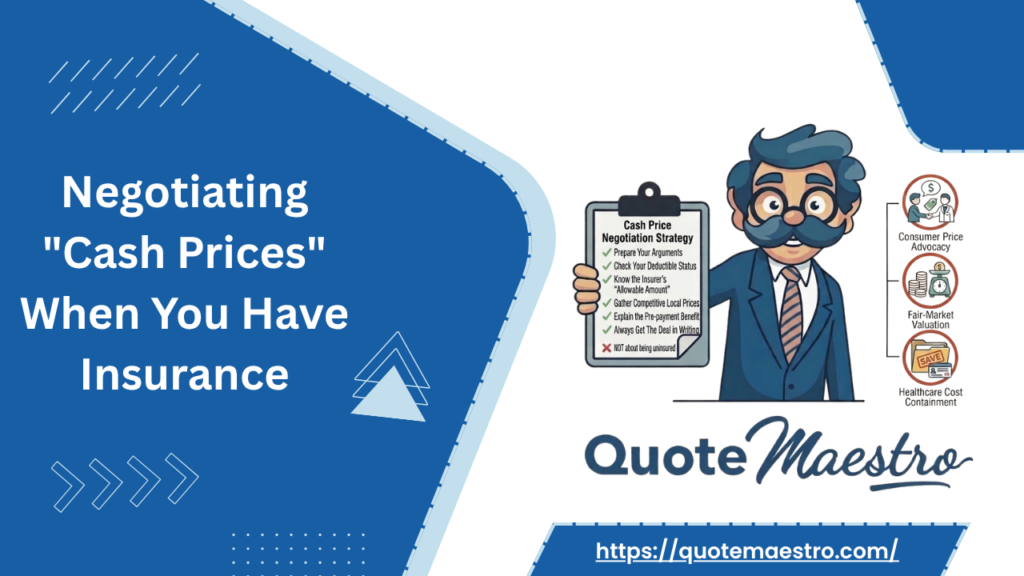

Step-by-Step Guide to Negotiating Cash Prices With Insurance

Here’s how to effectively use negotiating cash prices with insurance:

1️⃣ Ask for the Cash Price First

Always ask providers: “What is your cash or self-pay price?” This is the foundation of negotiating cash prices with insurance.

2️⃣ Compare With Insurance Costs

Check your Explanation of Benefits (EOB) to compare insured rates vs cash rates when negotiating cash prices with insurance.

3️⃣ Request Discounts

Don’t hesitate to ask for discounts. Many providers are open to reducing costs during negotiating cash prices with insurance.

4️⃣ Get Everything in Writing

Before proceeding, confirm pricing details in writing when negotiating cash prices with insurance.

5️⃣ Decide Whether to Use Insurance

Sometimes it’s better not to file a claim at all. Strategic decisions are key in negotiating cash prices with insurance.

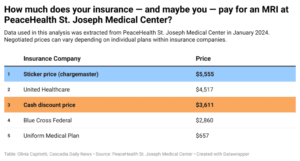

Real-Life Example of Negotiating Cash Prices With Insurance

Imagine a patient needing an MRI. Through insurance, the cost after deductible is $1,200. However, by asking for a cash rate, the provider offers the same MRI for $600 upfront.

This is a perfect example of how negotiating cash prices with insurance can cut costs in half.

Risks of Negotiating Cash Prices With Insurance

While negotiating cash prices with insurance can save money, there are some risks:

- Payments may not count toward your deductible

- You may lose insurance protections

- Emergency care cannot always be negotiated

- Some providers may not offer cash discounts

Understanding these risks ensures you use negotiating cash prices with insurance wisely.

Tips to Maximize Savings

To get the best results from negotiating cash prices with insurance, follow these tips:

- Always compare multiple providers

- Ask about bundled pricing

- Negotiate before receiving treatment

- Keep records of all agreements

- Use tools like https://quotemaestro.com/ to compare coverage and plan details

These strategies make negotiating cash prices with insurance more effective.

Future of Negotiating Cash Prices With Insurance

Healthcare pricing is slowly becoming more transparent. As a result, negotiating cash prices with insurance may become more common.

Trends include:

- More providers offering upfront pricing

- Increased consumer awareness

- Digital tools for cost comparison

- Growth of cash-based healthcare models

This shift means negotiating cash prices with insurance could become a standard practice.

FAQs: Negotiating Cash Prices With Insurance

❓ What is negotiating cash prices with insurance?

Negotiating cash prices with insurance means asking providers for a discounted self-pay rate even if you have insurance.

❓ Is it legal to pay cash instead of using insurance?

Yes, negotiating cash prices with insurance is completely legal and often encouraged for cost savings.

❓ Will cash payments count toward my deductible?

Usually not. This is an important factor when considering negotiating cash prices with insurance.

❓ Where can I compare insurance plans and costs?

You can explore options and better understand costs at https://quotemaestro.com/ to support negotiating cash prices with insurance decisions.

Final Thoughts on Negotiating Cash Prices With Insurance

Most people don’t realize they have the power to question and negotiate healthcare costs. By learning how negotiating cash prices with insurance works, you can take control of your medical expenses and potentially save hundreds—or even thousands—of dollars.

With the right approach, negotiating cash prices with insurance becomes a powerful strategy for smarter healthcare spending.