Healthcare costs continue climbing in 2026, and many businesses are searching for smarter ways to control employee benefit expenses. One strategy gaining serious attention is self-funding health insurance.

But while self-funded plans can offer flexibility and long-term savings, they are not the right fit for every company.

That’s why understanding self funded health plan readiness is critical before making the switch.

A self-funded plan allows employers to pay employee healthcare claims directly instead of paying fixed premiums to an insurance carrier. This can create major financial advantages, but it also increases risk and administrative responsibility.

Before transitioning away from traditional insurance, businesses should evaluate several important financial and operational factors.

This 5-point checklist will help determine whether your company has the right level of self funded health plan readiness for 2026.

What Does Self Funded Health Plan Readiness Mean?

In simple terms, self funded health plan readiness refers to whether a business has the financial stability, employee population, and administrative capacity to successfully manage a self-funded healthcare model.

Instead of paying predictable premiums every month, employers become responsible for actual healthcare claims.

This means businesses must prepare for:

- Variable healthcare costs

- Cash flow fluctuations

- Regulatory compliance

- Claims management oversight

- Potential catastrophic medical expenses

Companies that are financially prepared may gain significant long-term advantages from self-funding.

1. Does Your Business Have Strong Cash Flow?

The first and most important sign of self funded health plan readiness is financial stability.

Self-funded healthcare plans require employers to pay claims directly as they occur. Some months may have low claims, while other months could include major unexpected medical expenses.

Ask yourself:

- Can your business handle sudden claim spikes?

- Do you maintain healthy cash reserves?

- Is your revenue stable throughout the year?

- Can you absorb temporary healthcare cost increases?

Without strong financial reserves, self-funding can quickly become risky.

Businesses struggling with rising healthcare affordability should also review our guide on 2026 Health Insurance Affordability Rights.

2. Do You Have a Healthy Employee Population?

Another major factor in self funded health plan readiness is employee health risk.

Companies with healthier workforces often perform better financially under self-funded models.

Positive indicators include:

- Younger employee demographics

- Low chronic illness rates

- Strong wellness participation

- Limited high-cost claims history

- Preventive care engagement

Businesses with frequent large claims may experience more financial volatility.

Reviewing historical claims data is essential before moving toward self-funding.

3. Are You Comfortable Managing More Risk?

Under traditional insurance, the carrier assumes most healthcare risk.

With self-funded plans, the employer assumes much more responsibility.

That’s why true self funded health plan readiness includes risk tolerance.

Employers must understand that:

- Healthcare costs can fluctuate unpredictably

- Catastrophic claims may occur unexpectedly

- Budgeting becomes less predictable

- Stop-loss insurance becomes essential

Many companies purchase stop-loss protection to reduce exposure to extremely large claims.

Still, self-funding requires leadership teams that are comfortable managing more financial uncertainty.

For businesses comparing affordability strategies and employee healthcare protections, our article on 2026 Health Insurance Affordability Rights provides additional insights.

4. Does Your Business Have Administrative Resources?

One often-overlooked part of self funded health plan readiness is administration.

Self-funded plans require more active oversight than fully insured plans.

Employers may need:

- Third-party administrators (TPAs)

- Claims monitoring systems

- Compliance support

- Employee communication strategies

- Healthcare reporting analysis

Larger companies often have HR departments capable of managing these responsibilities more effectively.

Smaller businesses may need outside consulting support.

Without proper administration, self-funded plans can become difficult to manage efficiently.

5. Are You Focused on Long-Term Healthcare Strategy?

Businesses with strong self funded health plan readiness usually think beyond short-term savings.

Self-funding works best for employers focused on:

- Long-term healthcare cost control

- Employee wellness improvements

- Data-driven healthcare decisions

- Customized benefit structures

- Preventive care investment

Over time, businesses gain more visibility into employee healthcare spending patterns, which can help reduce unnecessary costs.

Companies exploring modern healthcare cost strategies should also review 2026 Health Insurance Affordability Rights to better understand affordability trends affecting employees in 2026.

The Biggest Advantages of Self-Funding

Businesses with strong self funded health plan readiness may benefit from:

- Lower long-term healthcare costs

- Greater claims transparency

- Custom plan flexibility

- Potential tax advantages

- Improved healthcare spending control

For healthier employee groups, self-funding can create meaningful savings over time.

The Biggest Risks of Self-Funding

Despite its advantages, self-funding also carries risks.

Potential challenges include:

- Large unexpected medical claims

- Financial unpredictability

- Increased administrative complexity

- Cash flow pressure

- Compliance obligations

That’s why evaluating self funded health plan readiness carefully is essential before making changes.

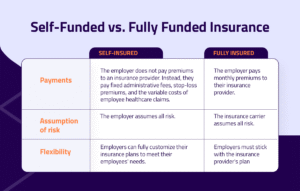

Fully Insured vs Self-Funded Plans

Businesses uncertain about self funded health plan readiness often compare self-funded models with fully insured plans.

Fully Insured Plans

- Predictable monthly premiums

- Lower financial risk

- Simpler administration

Self-Funded Plans

- Greater flexibility

- Variable healthcare costs

- Potential long-term savings

The best option depends on company size, financial strength, and healthcare goals.

How Stop-Loss Insurance Helps

Stop-loss insurance plays a major role in self funded health plan readiness.

This protection limits employer exposure to catastrophic claims by reimbursing costs above certain thresholds.

Two common types include:

- Individual stop-loss coverage

- Aggregate stop-loss coverage

Without stop-loss protection, one major medical event could significantly impact business finances.

Should Small Businesses Consider Self-Funding?

In the past, self-funding was mostly limited to large corporations.

However, newer healthcare models are making self-funded options more accessible for mid-sized businesses.

Still, smaller employers should evaluate self funded health plan readiness carefully because limited cash reserves increase financial vulnerability.

Businesses concerned about rising employee healthcare costs may also benefit from reviewing 2026 Health Insurance Affordability Rights before changing coverage structures.

Final Thoughts

Understanding self funded health plan readiness is essential before moving away from traditional fully insured healthcare plans.

While self-funding can provide long-term savings, flexibility, and greater cost transparency, it also introduces higher financial responsibility and administrative complexity.

Businesses with strong cash flow, healthier employee populations, and long-term healthcare strategies may benefit significantly from self-funded plans.

Carefully evaluating your company’s financial stability, risk tolerance, and operational resources can help determine whether self-funding is the right move for 2026 and beyond.

FAQs About Self Funded Health Plan Readiness

What is self funded health plan readiness?

It refers to whether a business has the financial and operational ability to manage a self-funded healthcare plan successfully.

Why do businesses choose self-funded health plans?

Many businesses want greater control over healthcare spending and potential long-term cost savings.

Is self-funding risky for small businesses?

Yes, smaller businesses may face greater financial risk if they lack strong cash reserves or stop-loss protection.

What is stop-loss insurance?

Stop-loss insurance protects self-funded employers from catastrophic healthcare claims.

How do you know if your business is ready for self-funding?

Strong cash flow, healthy employees, administrative resources, and long-term planning are major indicators of self funded health plan readiness.

Are self-funded plans cheaper than fully insured plans?

They can be more cost-effective for healthier employee groups, but costs may fluctuate more from year to year.