Choosing the right employee health coverage is one of the biggest financial decisions a business can make. Rising healthcare costs, changing regulations, and growing employee expectations are forcing employers to look more carefully at how they structure their benefits.

That’s why understanding fully insured vs self funded health plans has become increasingly important in 2026.

While both plan structures provide health coverage to employees, they operate very differently financially. One offers predictable monthly costs, while the other provides greater flexibility and potential long-term savings — but with higher risk.

In this guide, we’ll explain the major differences between fully insured and self-funded plans, the financial trade-offs involved, and how employers can decide which model fits their business goals.

What Are Fully Insured Health Plans?

To understand fully insured vs self funded health plans, it’s important to first define how each option works.

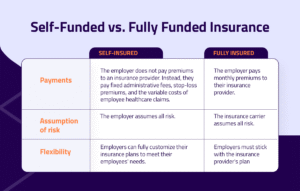

A fully insured health plan is the traditional insurance model most businesses know.

With this structure:

- Employers pay fixed monthly premiums to an insurance company

- The insurer assumes financial risk for employee medical claims

- Premiums are usually locked for a contract period

- Insurance carriers manage claims processing and administration

In simple terms, the insurance company handles most of the financial uncertainty.

This predictability makes fully insured plans attractive for many small and mid-sized businesses.

What Are Self-Funded Health Plans?

A self-funded health plan works differently.

Instead of paying fixed premiums to an insurer, the employer directly pays employee healthcare claims as they occur.

Under fully insured vs self funded health plans, self-funded arrangements typically involve:

- Employers covering medical claims directly

- Third-party administrators (TPAs) handling claims management

- Stop-loss insurance for catastrophic protection

- Greater plan customization flexibility

This approach gives businesses more control over healthcare spending but also exposes them to more financial risk.

The Biggest Financial Difference

The core financial difference in fully insured vs self funded health plans comes down to risk.

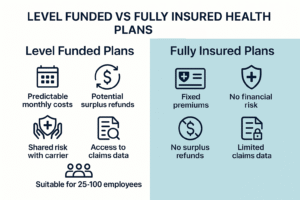

Fully Insured Plans

- Predictable monthly premiums

- Lower financial volatility

- Limited savings opportunities if claims are low

Self-Funded Plans

- Variable monthly healthcare costs

- Potential for major savings during healthy claim years

- Greater exposure to large unexpected claims

For employers, the decision often depends on risk tolerance and cash flow stability.

Why Some Businesses Prefer Fully Insured Plans

Many businesses choose fully insured plans because they provide simplicity and predictability.

Advantages of fully insured plans include:

- Easier budgeting

- Stable monthly expenses

- Reduced administrative complexity

- Less financial uncertainty

- Lower risk for smaller businesses

For companies with limited cash reserves, predictable costs are often extremely valuable.

When comparing fully insured vs self funded health plans, smaller employers frequently prefer the security of fully insured coverage.

If you are also comparing lower-cost coverage strategies for individuals and families, check out our guide on 2026 Bronze Health Insurance Plans.

Why Self-Funded Plans Are Growing in Popularity

Despite higher risk, self-funded plans are becoming more popular in 2026.

Many employers are attracted to the potential cost savings associated with fully insured vs self funded health plans.

Possible benefits of self-funded plans include:

- Lower long-term healthcare costs

- Greater transparency into claims data

- Customizable employee benefits

- Reduced state insurance taxes in some cases

- Flexibility in plan design

For healthier employee populations, self-funded plans can create substantial financial savings over time.

Stop-Loss Insurance Protects Self-Funded Employers

One major concern with self-funded plans is catastrophic medical claims.

That’s why many businesses purchase stop-loss insurance.

Stop-loss coverage helps limit financial exposure by protecting employers against:

- Extremely high individual claims

- Unexpected overall claim spikes

This protection plays a critical role in balancing risk under fully insured vs self funded health plans.

Without stop-loss protection, a few major medical cases could severely impact company finances.

Administrative Differences Matter Too

Another important factor in fully insured vs self funded health plans is administration.

Fully insured plans are generally easier to manage because insurance carriers handle:

- Claims processing

- Provider networks

- Regulatory compliance

- Customer support

Self-funded plans often require:

- Third-party administrators

- More active oversight

- Detailed claims monitoring

- Additional financial reporting

Larger companies may have the resources to manage this complexity more effectively.

Data Transparency Can Help Control Costs

One reason employers increasingly favor self-funded plans is access to healthcare claims data.

With fully insured plans, businesses often receive limited insight into employee healthcare spending patterns.

Self-funded models may provide more detailed reporting on:

- Prescription drug spending

- High-cost claims trends

- Preventive care usage

- Chronic condition management

This transparency can help employers make smarter long-term decisions when evaluating fully insured vs self funded health plans.

If you are also comparing lower-cost coverage strategies for individuals and families, check out our guide on 2026 Bronze Health Insurance Plans.

Which Businesses Benefit Most from Self-Funding?

Self-funded plans often work best for businesses that:

- Have strong cash flow

- Employ healthier populations

- Want customized benefit structures

- Have larger employee groups

- Can tolerate some financial variability

Companies with stable finances may view self-funding as a long-term investment strategy rather than simply an insurance purchase.

Which Businesses Should Stay Fully Insured?

Fully insured plans may remain the better option for businesses that:

- Need predictable monthly costs

- Have smaller employee groups

- Prefer simpler administration

- Have limited financial reserves

- Want lower risk exposure

For many employers, stability and simplicity outweigh potential savings opportunities.

Regulatory and Compliance Considerations

Another major difference in fully insured vs self funded health plans involves regulation.

Fully insured plans are primarily regulated by state insurance laws.

Self-funded plans are generally governed under federal ERISA regulations, which can create:

- Different compliance obligations

- Greater flexibility in some areas

- Potential legal complexity

Businesses should consult benefits professionals before making major plan changes.

Rising Healthcare Costs Are Driving Change

Healthcare inflation continues pressuring employers nationwide.

As costs rise, many businesses are reevaluating traditional insurance structures and exploring alternatives.

This is one reason why discussions around fully insured vs self funded health plans are becoming more common in 2026.

Employers increasingly want more control over healthcare spending while still providing competitive employee benefits.

If you are also comparing lower-cost coverage strategies for individuals and families, check out our guide on 2026 Bronze Health Insurance Plans.

How to Choose the Right Plan Structure

When comparing fully insured vs self funded health plans, businesses should evaluate:

- Cash flow stability

- Risk tolerance

- Employee health trends

- Administrative resources

- Long-term financial goals

- Workforce size

The “best” option depends entirely on company finances and operational priorities.

For more health insurance insights and business coverage guidance, visit Quote Maestro.

Final Thoughts

Understanding fully insured vs self funded health plans is essential for businesses trying to manage rising healthcare costs while maintaining strong employee benefits.

Fully insured plans provide stability, simplicity, and predictable budgeting. Self-funded plans offer greater flexibility, transparency, and potential long-term savings — but with higher financial risk.

As healthcare expenses continue rising in 2026, more employers are carefully weighing these trade-offs to determine which approach best fits their business strategy.

The right decision ultimately depends on balancing financial protection with cost-control opportunities.

FAQs About Fully Insured vs Self Funded Health Plans

What is the difference between fully insured vs self funded health plans?

Fully insured plans involve fixed premiums paid to an insurer, while self-funded plans require employers to pay employee claims directly.

Are self-funded health plans cheaper?

They can be cheaper long term for healthier employee groups, but they also involve greater financial risk.

Why do businesses choose fully insured plans?

Many businesses prefer predictable monthly costs and reduced administrative complexity.

What is stop-loss insurance?

Stop-loss insurance protects self-funded employers from catastrophic healthcare claims.

Are self-funded plans only for large companies?

Traditionally yes, but more mid-sized businesses are now exploring self-funded options.

Which option is safer financially?

Fully insured plans generally provide more predictable financial protection, especially for smaller businesses.