Switching to a self-funded health plan can feel like a major leap for any business. While self-funding offers more flexibility and potential cost savings, the first year often comes with a learning curve that many employers underestimate.

That’s why understanding the realities of a first year self funded health plan is so important before making the transition.

Unlike traditional fully insured coverage, self-funded plans place more financial responsibility directly on the employer. Businesses gain more control over healthcare spending, but they also become more involved in claims management, budgeting, and employee communication.

The good news is that most challenges become easier after the first year once systems, reporting, and expectations stabilize.

In this guide, we’ll break down exactly what businesses should expect during the first 12 months of a self-funded health plan.

What Is a Self-Funded Health Plan?

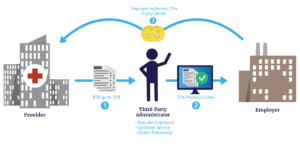

Before discussing the first year self funded health plan experience, it’s important to understand how self-funding works.

With a self-funded plan:

- Employers pay employee healthcare claims directly

- Third-party administrators (TPAs) usually manage claims processing

- Businesses often purchase stop-loss insurance for protection

- Healthcare costs fluctuate based on actual employee usage

Instead of paying fixed premiums to an insurance carrier, employers take on more financial risk in exchange for greater flexibility and potential savings.

For independent contractors and self-employed professionals exploring alternative healthcare options, check out How to Choose Health Insurance as a Freelancer.

Why Businesses Switch to Self-Funding

Many employers move toward self-funded models because of rising healthcare costs.

A first year self funded health plan often appeals to businesses seeking:

- More control over healthcare spending

- Greater transparency into claims data

- Customizable benefits

- Potential long-term savings

- Reduced insurance carrier restrictions

For healthier employee populations, self-funding can create substantial financial advantages over time.

Month 1–3: The Adjustment Period

The first few months of a first-year self-funded health plan are usually the most unpredictable.

Employers often experience:

- Employee questions about new coverage

- Claims processing adjustments

- New reporting systems

- Administrative learning curves

- Cash flow monitoring changes

Employees may also need time to understand:

- Provider networks

- Prescription coverage

- ID cards and billing

- Claims procedures

Strong communication during this phase is extremely important.

Businesses with remote workers or freelancers should also review How to Choose Health Insurance as a Freelancer to better understand modern healthcare coverage trends.

Expect More Attention on Cash Flow

One major difference during a first year self funded health plan is financial variability.

Under fully insured plans, monthly costs are mostly predictable.

With self-funding:

- Some months may have very low claims

- Other months may include major unexpected expenses

- Healthcare costs become less consistent

This unpredictability can feel stressful at first, especially for businesses unfamiliar with variable healthcare spending.

That’s why maintaining strong financial reserves is essential.

Stop-Loss Insurance Becomes Critical

During a first year self funded health plan, stop-loss insurance plays a major role in protecting company finances.

Stop-loss coverage helps reimburse employers for:

- Large individual claims

- Unexpected overall claims spikes

Without this protection, one catastrophic medical event could significantly affect the business.

Many employers gain peace of mind knowing stop-loss coverage limits financial exposure during the transition period.

Claims Data Starts Becoming Valuable

One of the most powerful benefits of a first year self funded health plan is access to healthcare claims data.

Unlike fully insured models, self-funded employers often receive detailed insights into:

- High-cost claims trends

- Prescription spending

- Preventive care usage

- Chronic condition costs

- Emergency room utilization

This information allows businesses to make smarter long-term healthcare decisions.

The first year is often when employers begin identifying cost-saving opportunities they never saw before.

Employee Education Is Extremely Important

Employees may initially feel nervous about changes in healthcare coverage.

That’s why successful businesses prioritize communication during the first year self funded health plan experience.

Helpful employee education may include:

- Benefit meetings

- FAQ documents

- Claims support contacts

- Network explanations

- Preventive care guidance

When employees understand how the plan works, confusion and frustration decrease significantly.

For self-employed workers learning about private healthcare options, our guide on How to Choose Health Insurance as a Freelancer offers additional helpful insights.

Administrative Work Usually Increases

Another reality of the first year self funded health plan is increased administration.

Even with a third-party administrator, employers often become more involved in:

- Reviewing claims reports

- Monitoring healthcare trends

- Managing compliance requirements

- Evaluating stop-loss renewals

- Tracking healthcare spending

This increased visibility creates more responsibility, but also more control.

Cost Savings May Not Happen Immediately

Some businesses expect instant savings after switching to self-funding.

However, the first year self funded health plan is often more about stabilization and learning than dramatic short-term financial gains.

Savings depend heavily on:

- Employee health trends

- Claims experience

- Stop-loss structure

- Administrative efficiency

Many employers see the greatest long-term value after the first year once they begin using claims data strategically.

Wellness Programs Become More Valuable

Self-funded employers directly benefit when employees stay healthier.

That’s why wellness initiatives often become a major focus during a first year self funded health plan.

Popular wellness efforts may include:

- Preventive screenings

- Smoking cessation programs

- Mental health support

- Fitness incentives

- Chronic disease management

Healthier employees can lead to lower long-term claims costs.

Renewal Discussions Start Earlier Than Expected

Many employers are surprised by how early renewal planning begins during the first year self funded health plan.

Businesses often review:

- Claims performance

- Stop-loss renewal pricing

- Employee healthcare usage

- Plan design changes

- Cost-control strategies

This ongoing analysis helps improve future healthcare planning.

Common Challenges During Year One

Some of the most common challenges businesses face during a first year self funded health plan include:

- Claims volatility

- Employee confusion

- Cash flow stress

- Administrative complexity

- Provider network concerns

Fortunately, most of these issues become easier to manage with experience and strong vendor support.

Signs Your First Year Is Going Well

Positive indicators during a first year self funded health plan may include:

- Stable claims trends

- Strong employee engagement

- Effective stop-loss protection

- Improved healthcare transparency

- Better cost forecasting

Businesses that monitor data consistently often gain more confidence as the year progresses.

How to Succeed in Year One

To improve the success of your first year self funded health plan, focus on:

- Strong employee communication

- Financial preparation

- Reliable stop-loss coverage

- Regular claims monitoring

- Long-term planning

Self-funding works best when businesses stay proactive rather than reactive.

For more healthcare strategy insights and insurance guidance, visit Quote Maestro.

Final Thoughts

The first year self funded health plan experience is often both exciting and challenging for employers.

While self-funding introduces more financial responsibility and administrative involvement, it also creates opportunities for greater transparency, long-term savings, and healthcare customization.

Businesses that prepare carefully, communicate clearly with employees, and monitor claims consistently are often in the best position to succeed.

The first 12 months are usually about learning, adapting, and building a stronger long-term healthcare strategy for both the company and its employees.

FAQs About First Year Self Funded Health Plan

What is a first year self funded health plan?

It refers to the first 12 months after a business transitions from fully insured healthcare to a self-funded insurance model.

Are self-funded plans risky in the first year?

They can involve more financial unpredictability, especially if businesses lack strong reserves or stop-loss protection.

Why do businesses choose self-funded plans?

Many employers want more healthcare cost control, transparency, and long-term savings opportunities.

What is stop-loss insurance?

Stop-loss insurance protects self-funded employers from catastrophic medical claims.

Do businesses save money immediately after self-funding?

Not always. Some savings may take time as claims data and healthcare strategies improve.

Is employee communication important during year one?

Yes, clear employee education helps reduce confusion and improves the transition experience.