Healthcare costs continue rising in 2026, and mid-sized businesses are under growing pressure to control employee benefit expenses without sacrificing quality coverage.

As traditional fully insured plans become more expensive, many employers are exploring alternative funding strategies. Two of the most talked-about options are level-funded plans and true self-funded plans.

That’s why understanding level funded vs true self funded plans is becoming increasingly important for business owners and HR leaders.

While both options offer greater flexibility than traditional insurance, they work very differently financially. One focuses on predictable monthly payments, while the other gives employers maximum control — along with more financial risk.

In this guide, we’ll explain the major differences between level-funded and true self-funded plans, their pros and cons, and how mid-sized businesses can determine which model fits their goals.

What Is a Level-Funded Health Plan?

To understand level funded vs true self funded, it’s important to first define how level-funded plans work.

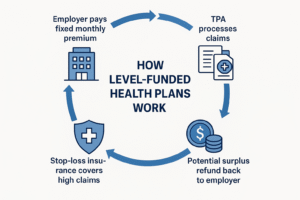

A level-funded plan combines features of both fully insured and self-funded healthcare.

With a level-funded plan:

- Employers pay fixed monthly amounts

- Payments cover claims, administration, and stop-loss insurance

- Unused claims funds may be refunded at year-end

- Financial risk is partially limited through stop-loss protection

This structure gives businesses more predictable healthcare costs while still offering some potential savings.

For many mid-sized employers, level-funded plans feel like a safer introduction to self-funding.

What Is a True Self-Funded Plan?

A true self-funded plan places more direct financial responsibility on the employer.

Under level funded vs true self funded, true self-funding means:

- Employers pay healthcare claims directly as they occur

- Monthly costs can fluctuate significantly

- Businesses usually purchase stop-loss insurance

- Employers gain greater claims transparency and flexibility

Unlike level-funded models, there are no fixed monthly claim payments. Actual healthcare usage determines costs.

This can create larger savings opportunities — but also more financial unpredictability.

Why Mid-Sized Businesses Are Exploring Self-Funding

Rising insurance premiums are forcing employers to look for alternatives.

Many companies researching level funded vs true self funded plans want:

- Better cost control

- Greater healthcare transparency

- Flexible plan design

- Long-term savings opportunities

- Reduced dependence on traditional insurance carriers

Mid-sized businesses are increasingly realizing that fully insured plans may not always provide the best financial value.

The Biggest Difference: Financial Predictability

The largest distinction in level funded vs true self funded is how costs are managed.

Level-Funded Plans

- Predictable monthly payments

- Lower cash flow volatility

- Easier budgeting

True Self-Funded Plans

- Variable monthly costs

- Greater exposure to claims spikes

- Higher financial flexibility

For businesses prioritizing stable budgeting, level-funded plans often feel less risky.

Risk Levels: Which Option Is Safer?

When comparing level funded vs true self funded, risk tolerance becomes extremely important.

Level-Funded Risk

Level-funded plans include built-in stop-loss protection and fixed payment structures, helping reduce financial surprises.

True Self-Funded Risk

True self-funded plans expose employers more directly to claims fluctuations, even with stop-loss insurance.

Companies with strong financial reserves may feel more comfortable handling this risk.

Potential Savings Opportunities

Both models may create savings opportunities compared to traditional fully insured plans.

However, level funded vs true self funded plans differ in how savings work.

Level-Funded Savings

If employee claims remain lower than expected, employers may receive partial refunds at year-end.

True Self-Funded Savings

Employers keep more direct control over healthcare spending and may experience larger long-term savings during low-claim years.

The trade-off is greater financial uncertainty.

Administrative Complexity Matters

Another major factor in level funded vs true self funded plans is administration.

Level-Funded Plans

These plans are often easier to manage because carriers or administrators handle much of the complexity.

True Self-Funded Plans

Employers may need more active oversight involving:

- Claims monitoring

- Vendor management

- Financial reporting

- Compliance tracking

Larger businesses may have the resources to handle this more effectively.

Claims Transparency and Data Access

One reason employers prefer self-funded structures is healthcare data visibility.

Under traditional insurance, businesses often receive limited claims information.

With level funded vs true self funded plans, employers may gain better insights into:

- Prescription drug costs

- High-cost claims trends

- Preventive care usage

- Chronic disease spending

This data helps businesses make smarter healthcare decisions long term.

Which Businesses Prefer Level-Funded Plans?

Level-funded plans often appeal to businesses that:

- Want predictable monthly costs

- Are new to self-funding

- Prefer lower financial volatility

- Have moderate cash reserves

- Want simplified administration

For many mid-sized employers, level-funded plans serve as a middle ground between fully insured and fully self-funded healthcare.

Which Businesses Prefer True Self-Funding?

True self-funded plans usually work best for businesses that:

- Have strong financial reserves

- Can tolerate claims volatility

- Want maximum plan flexibility

- Prefer direct healthcare spending control

- Have larger employee populations

These companies often view healthcare as a long-term financial strategy rather than simply an insurance expense.

Stop-Loss Insurance Is Essential

Both level funded vs true self funded models rely heavily on stop-loss insurance.

This protection limits exposure to catastrophic healthcare claims.

Stop-loss coverage may include:

- Individual stop-loss protection

- Aggregate stop-loss protection

Without stop-loss insurance, one major medical claim could significantly affect business finances.

Employee Experience Usually Stays Similar

One important fact about level funded vs true self funded plans is that employees may not notice major differences.

Most employees still receive:

- Provider networks

- ID cards

- Prescription coverage

- Claims processing support

The biggest differences happen behind the scenes financially for the employer.

Freelancers and Independent Contractors Are Also Exploring Alternative Coverage

As healthcare costs rise, freelancers and independent workers are also looking for more flexible insurance solutions.

If your business works with contractors or remote professionals, check out How to Choose Health Insurance as a Freelancer for additional healthcare planning insights.

Many businesses researching level funded vs true self funded strategies are also reevaluating healthcare support for non-traditional workers.

Long-Term Planning Is Critical

Choosing between level funded vs true self funded should involve long-term financial analysis.

Businesses should evaluate:

- Claims history

- Employee health trends

- Cash flow stability

- Risk tolerance

- Administrative capabilities

Healthcare funding decisions affect both financial performance and employee satisfaction.

Companies supporting remote teams and freelance talent may also benefit from reading How to Choose Health Insurance as a Freelancer to better understand modern healthcare expectations.

How to Choose the Right Option

When comparing level funded vs true self funded, ask these questions:

- Does your business need predictable monthly costs?

- Can you handle financial fluctuations?

- How healthy is your employee population?

- Do you want more healthcare spending transparency?

- Does your HR team have administrative capacity?

The right solution depends on your business’s financial goals and risk tolerance.

For more healthcare strategy resources and insurance guidance, visit Quote Maestro.

Final Thoughts

Understanding level funded vs true self funded plans is essential for mid-sized businesses navigating rising healthcare costs in 2026.

Level-funded plans provide greater budgeting stability and reduced financial risk, making them attractive for employers transitioning away from traditional insurance.

True self-funded plans offer maximum flexibility, transparency, and long-term savings potential — but they also require stronger financial reserves and greater risk tolerance.

The best option depends on your company’s healthcare goals, employee population, and financial strength.

Businesses exploring healthcare alternatives for both employees and contractors should also review How to Choose Health Insurance as a Freelancer for additional coverage insights.

FAQs About Level Funded vs True Self Funded

What is the difference between level funded vs true self funded plans?

Level-funded plans use fixed monthly payments, while true self-funded plans involve paying actual healthcare claims directly.

Which option is less risky?

Level-funded plans are generally less risky because they offer more predictable monthly costs.

Can businesses save money with self-funded plans?

Yes, healthier employee populations may create significant long-term savings opportunities.

What is stop-loss insurance?

Stop-loss insurance protects employers from catastrophic healthcare claims.

Are level-funded plans good for mid-sized businesses?

Yes, many mid-sized businesses use level-funded plans as a lower-risk introduction to self-funding.

Do employees notice differences between these plans?

Usually not. Employees often experience similar provider networks and healthcare access regardless of funding structure.