One of the biggest questions people ask before buying life insurance is simple but incredibly important: how much life insurance coverage do you need?

Buy too little, and your family may struggle financially when they need support the most. Buy too much, and you may end up paying higher premiums than necessary.

Finding the right balance is where smart financial planning begins.

The truth is, there is no one-size-fits-all answer. Your ideal coverage depends on your income, debts, family responsibilities, future goals, and the lifestyle you want your loved ones to maintain.

Understanding how much life insurance coverage do you need helps you make a confident decision instead of guessing.

This guide breaks down the hidden math behind life insurance so you can protect your family the right way.

Why Understanding How Much Life Insurance Coverage Do You Need Matters

Life insurance is not just about leaving money behind. It is about replacing stability, income, and financial security.

When asking how much life insurance coverage do you need, you are really asking:

“How can I make sure my family is financially safe if I am no longer here?”

That answer includes more than funeral costs.

It includes:

- Monthly household expenses

- Mortgage or rent payments

- Outstanding debts

- Children’s education costs

- Future retirement needs for your spouse

- Emergency financial support

- Long-term family security

This is why accurate planning matters so much.

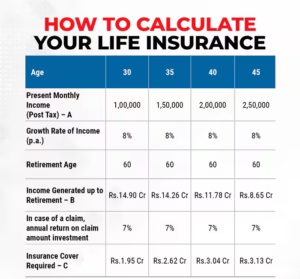

The Basic Formula for How Much Life Insurance Coverage Do You Need

A common starting point for how much life insurance coverage do you need is the 10 to 15 times income rule.

For example:

If your annual income is $50,000, your coverage may need to be between $500,000 and $750,000.

Coverage=Income×(10 to 15)Coverage = Income \times (10 \text{ to } 15)

This is a helpful estimate, but it is not enough for everyone.

A better strategy looks deeper into your personal financial responsibilities.

Step 1: Calculate Income Replacement

The first major part of how much life insurance coverage do you need is replacing lost income.

Ask yourself:

How many years would my family need financial support?

For example:

- 10 years of support

- 15 years until children become independent

- Coverage until retirement for your spouse

If your family needs $60,000 per year for 15 years:

60,000×15=900,00060{,}000 \times 15 = 900{,}000

That means income replacement alone may require $900,000 in coverage.

This is why guessing often leads to underinsurance.

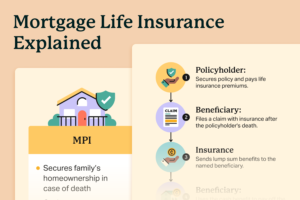

Step 2: Add Debt and Mortgage Protection

Another critical part of how much life insurance coverage do you need is debt protection.

Your family should not inherit financial burdens like:

- Mortgage balances

- Car loans

- Credit card debt

- Personal loans

- Business obligations

If your mortgage is $250,000 and other debts total $50,000:

250,000+50,000=300,000250{,}000 + 50{,}000 = 300{,}000

That adds another $300,000 to your ideal coverage amount.

Life insurance should protect your family from stress—not transfer debt to them.

Step 3: Plan for Children’s Education

When thinking about how much life insurance coverage do you need, education planning is often overlooked.

College and school expenses can be significant.

Ask yourself:

- How many children do I have?

- What future education costs should be covered?

- Private school or college tuition goals?

If education needs total $100,000 per child for two children:

100,000×2=200,000100{,}000 \times 2 = 200{,}000

That becomes part of your total protection plan.

Your family’s future goals should stay protected.

Step 4: Subtract Existing Savings and Assets

Not all calculations in how much life insurance coverage do you need are additions.

You should also subtract:

- Existing savings

- Emergency funds

- Retirement accounts

- Current investments

- Employer-provided life insurance coverage

If your total financial need is $1,200,000 and you already have $300,000 in savings and benefits:

1,200,000−300,000=900,0001{,}200{,}000 – 300{,}000 = 900{,}000

Your actual coverage need may be closer to $900,000.

This creates a more realistic and affordable target.

Common Mistakes When Deciding How Much Life Insurance Coverage Do You Need

Many people make costly mistakes when calculating how much life insurance coverage do you need.

Choosing the Cheapest Policy Only

Low premiums often mean low protection.

Forgetting Inflation

Future costs will likely be much higher than today.

Ignoring Stay-at-Home Parent Value

Even unpaid household work has major financial value.

Not Reviewing Coverage Over Time

Marriage, children, income growth, and new debts all change your needs.

Life insurance should grow with your life.

How to Get the Right Answer for How Much Life Insurance Coverage Do You Need

There is no perfect universal number.

The best answer to how much life insurance coverage do you need is the amount that keeps your family financially stable without creating unnecessary premium costs.

A strong plan should protect:

- Income

- Home

- Education

- Lifestyle

- Long-term financial peace

If you want to compare policies and calculate the right amount for your needs, visit

👉 https://quotemaestro.com/

This helps simplify the process and makes choosing the right coverage much easier.

Final Thoughts: The Right Number Creates Real Peace of Mind

The question is not simply how much life insurance coverage do you need.

The real question is:

“How much protection does my family need to feel secure without me?”

That answer is deeply personal.

Life insurance is not about random numbers.

It is about protecting people, preserving dreams, and creating financial confidence for the future.

The hidden math matters because your family matters.

And when you get the number right, you are not just buying insurance—you are building peace of mind.

❓ FAQs About How Much Life Insurance Coverage Do You Need

1. How much life insurance coverage do you need for a family?

Most families need 10 to 15 times annual income, but the exact answer depends on debts, mortgage, education costs, and long-term financial goals.

2. Is the 10x income rule enough for how much life insurance coverage do you need?

It is a helpful starting point, but a full calculation should include debts, children’s education, and existing savings for better accuracy.

3. Does mortgage affect how much life insurance coverage do you need?

Yes. Your mortgage balance should be included so your family can remain financially secure without housing stress.

4. Should stay-at-home parents consider how much life insurance coverage do you need?

Absolutely. Childcare, household management, and daily support all have major financial value that should be protected.

5. Can employer life insurance answer how much life insurance coverage do you need?

Usually not completely. Employer coverage is often limited and may not be enough for full family protection.

6. Where can I calculate how much life insurance coverage do you need?

You can compare plans and estimate the right amount of coverage by visiting

👉 https://quotemaestro.com/

This helps you make a smarter and more confident life insurance decision.