Universal life insurance is a type of permanent life insurance designed to provide lifelong coverage with adjustable premiums and a cash value component. It combines insurance protection with an internal account that can grow over time based on credited interest and policy charges.

Unlike term coverage, universal life insurance does not end after a set number of years if it is funded enough to cover its ongoing costs. It is built for people who want flexibility and are comfortable monitoring how the policy performs.

How Universal Life Insurance Works?

Universal life insurance is funded by premium payments that the insurer allocates across policy charges and the cash value account. The insurer deducts costs, then credits interest to the remaining cash value according to the policy terms.

The death benefit is generally the face amount, though some policies offer options that increase the death benefit under defined rules. Policy performance depends on funding level, credited interest and cost of insurance charges that typically rise with age.

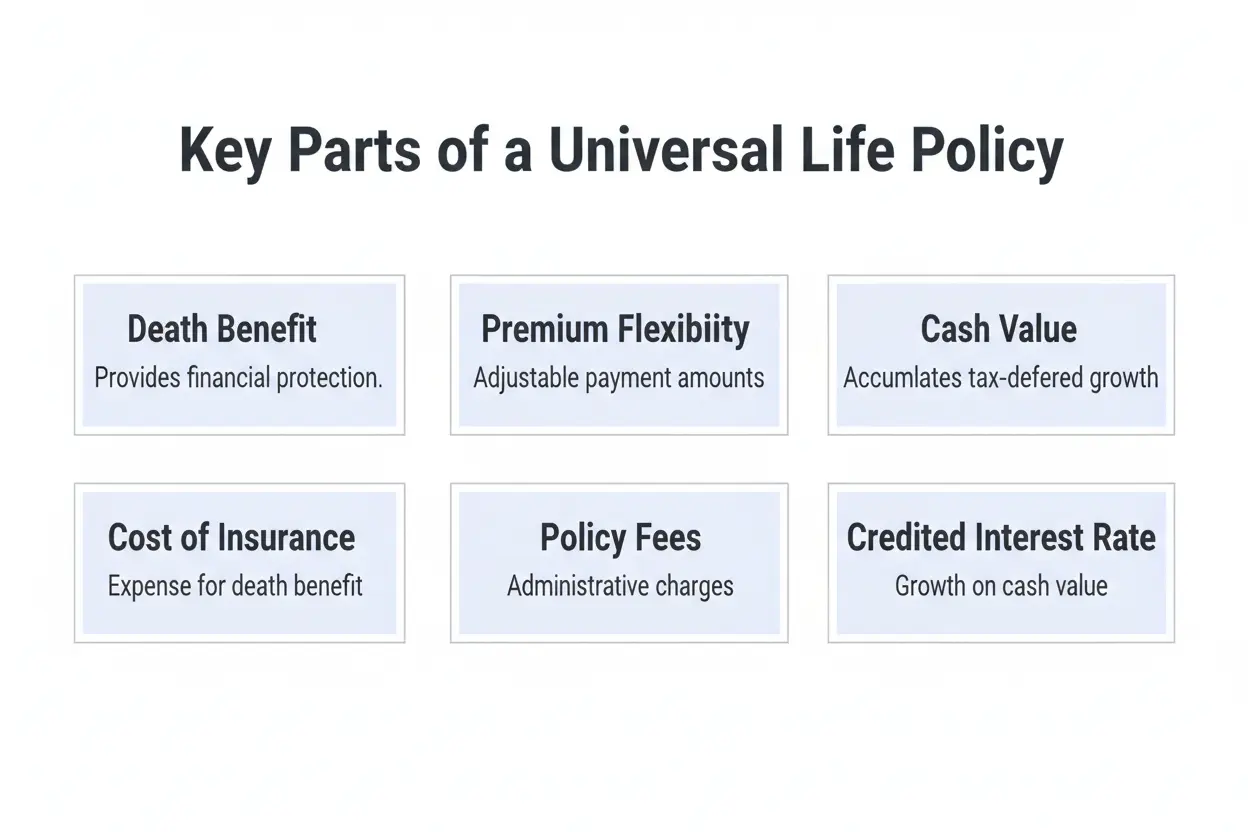

Key Parts Of a Universal Life Policy

Most universal life insurance contracts share the same core moving pieces, even if the labels vary by carrier. Knowing these parts helps you evaluate illustrations and avoid surprises later.

- Death benefit. The amount paid to beneficiaries after the insured dies, subject to the policy being in force.

- Premium flexibility. The ability to pay more, pay less, or sometimes skip payments when cash value is sufficient.

- Cash value. The internal account value after charges, which can earn interest and may be accessed through withdrawals or loans.

- Cost of insurance. The monthly charge for coverage, usually increasing over time as mortality risk rises.

- Policy fees. Administrative charges and other expenses taken from premiums or cash value.

- Credited interest rate. The rate applied to cash value under the policy’s crediting method, often with a guaranteed minimum.

These components interact continuously, so small changes in funding or crediting can have long-term effects. That is why reviewing the ledger and assumptions matters before committing.

Premium Flexibility and Funding Rules

The flexibility in universal life insurance can be helpful, but it also places more responsibility on the policy owner. Paying the minimum may keep the policy in force early on, yet it can raise the risk of shortfalls later if costs rise faster than growth.

Many policies define a target premium that supports the illustrated outcome, even though it is not always required. Overfunding can improve cash value growth, but it must stay within tax rules to avoid creating a modified endowment contract.

Cash Value Growth and Interest Crediting

Cash value in universal life insurance grows through interest crediting after charges are deducted. Interest crediting depends on the policy type and the credited rate may change based on carrier declarations or index-linked formulas.

Most contracts include a guaranteed minimum interest rate for the general account method, although the actual credited rate can be higher or lower than past performance. It is important to separate guarantees from non-guaranteed assumptions when reviewing projections.

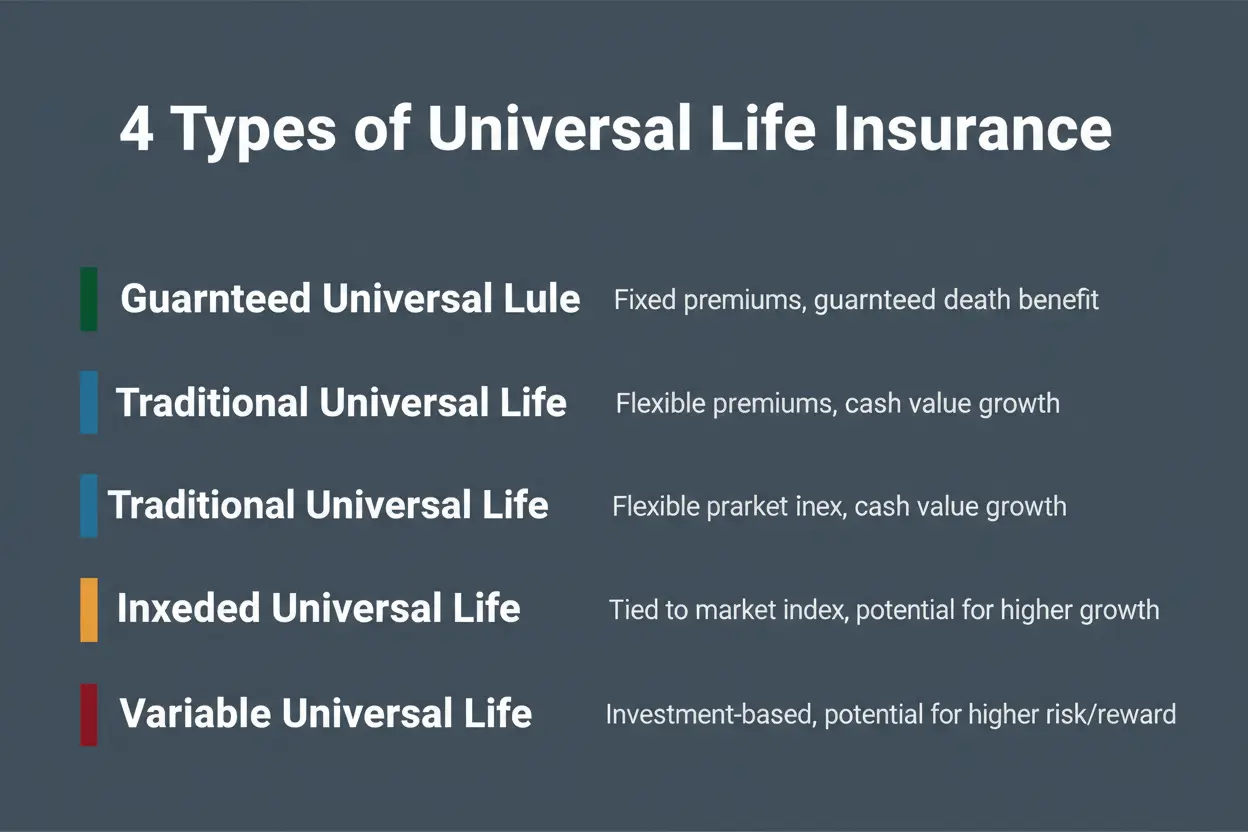

Types of Universal Life Insurance

Universal life insurance comes in several forms, each using a different method for cash value accumulation. The right choice depends on risk tolerance, the need for predictability and how actively you want to track performance.

- Guaranteed universal life. Designed to keep coverage in force with limited cash value growth when funded to the guarantee requirements.

- Traditional universal life. Credits interest based on the insurer’s declared rate, usually with a minimum guarantee.

- Indexed universal life. Credits interest based on an index-linked formula with caps and participation rates, generally without direct market investment.

- Variable universal life. Cash value is invested in subaccounts and performance can vary with market results and investment choices.

Each type balances guarantees, potential upside and complexity differently. Comparing the mechanics side by side can make the tradeoffs clearer.

| Type | Main Cash Value Driver | Typical Strength |

|---|---|---|

| Guaranteed Universal Life | Premium schedule meeting guarantee terms | Strong focus on keeping coverage in force |

| Traditional Universal Life | Carrier-declared interest crediting | Moderate flexibility with simpler mechanics |

| Indexed Universal Life | Index-linked crediting with caps and participation | Potential for higher credited interest without direct equity ownership |

| Variable Universal Life | Market performance of subaccounts | Highest upside potential with higher volatility and responsibility |

Universal Life Insurance Vs Term Life Insurance

Term life insurance is built for a specific period, often with level premiums and no cash value. Universal life insurance is built for long-term coverage with cash value and policy controls that can shift over time.

Term can be a straightforward way to buy a large death benefit for a lower cost, but it may become expensive to renew later. Universal life insurance generally costs more than term initially, but it may provide lifetime protection and a funding buffer through cash value.

Potential Benefits

Universal life insurance can solve multiple planning goals when the policy is structured and maintained properly. The benefits tend to be strongest when the policy is funded consistently and reviewed periodically.

- Lifetime coverage potential. Coverage can remain in force beyond a term period when funding supports ongoing charges.

- Adjustable premiums. Premium flexibility can help during income changes, within policy and tax limits.

- Cash value access. Loans and withdrawals may be available, although they can reduce death benefits and affect policy health.

- Estate planning support. Death benefit proceeds are generally paid to beneficiaries and ownership structures can be planned carefully.

These advantages come with tradeoffs, so the next step is understanding costs and ongoing responsibilities. That context helps set realistic expectations.

Risks and Downsides to Know

Universal life insurance is not a set-and-forget product, especially outside of strong guarantee designs. If credited interest underperforms or charges rise, the policy may require higher premiums to avoid lapse.

Policy loans can create compounding strain if unpaid loan balances and interest grow faster than cash value. A lapse with loans may also create taxable income, so ongoing monitoring is essential.

- Non-guaranteed assumptions. Illustrated values can change if crediting rates or charges differ from projections.

- Increasing insurance costs. Monthly costs can rise with age, especially in later years.

- Complexity. Index caps, participation rates and investment options can be hard to compare without careful review.

- Lapse risk. Underfunding can cause the policy to terminate when cash value can no longer cover charges.

These risks are manageable when you understand the mechanics and track the policy regularly. The goal is to choose a structure that matches how much oversight you want.

Policy Loans and Withdrawals

Universal life insurance often allows access to cash value through withdrawals or policy loans. Withdrawals typically reduce cash value and may reduce the death benefit, depending on the policy option.

Loans use the cash value as collateral and charge loan interest, while the insurer may still credit interest on the loaned amount depending on the contract. Managing loan balances matters because excessive loans can increase lapse risk and may trigger taxes if the policy ends.

Costs and Fees That Affect Performance

Policy charges shape how universal life insurance performs over time. Understanding the cost structure helps you interpret why two policies with the same premium can produce different outcomes.

- Premium load. A percentage taken from premiums before money reaches cash value.

- Monthly policy fee. A fixed administrative charge deducted regularly.

- Cost of insurance rate. A charge based on age, health class and net amount at risk.

- Surrender charges. Fees for canceling in the early years, often declining over time.

When reviewing an illustration, focus on guaranteed values, current assumptions and how sensitive the outcome is to lower crediting. That perspective keeps decisions grounded.

Who Universal Life Insurance May Fit?

Universal life insurance is often considered by people who need coverage beyond a specific time window. It can also appeal to those who want flexibility in premium timing while keeping permanent protection as the central goal.

It may be less suitable for anyone who prefers fixed, simple structures and does not want to review statements or adjust funding. In that case, term insurance or more guarantee-heavy permanent options can be easier to manage.

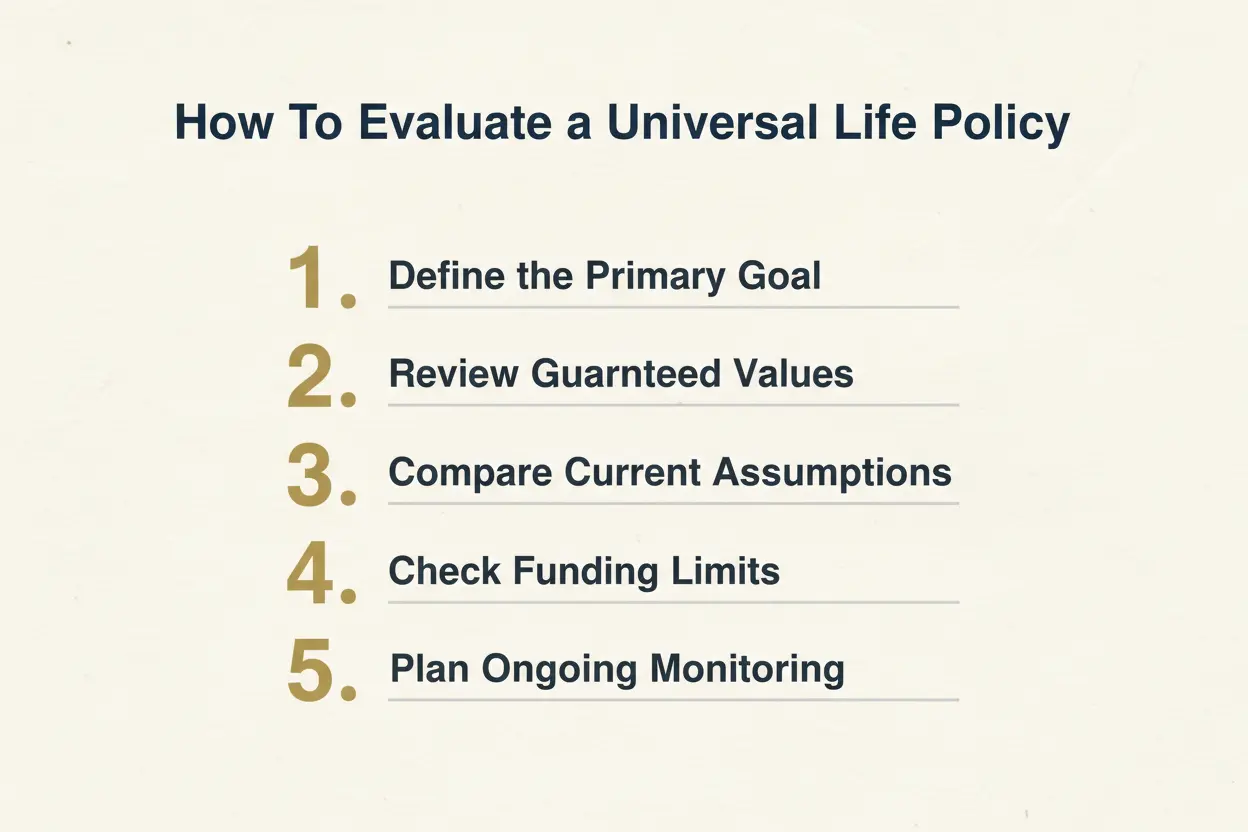

How To Evaluate a Policy Before Buying?

A good evaluation starts with clarity on what the policy must accomplish, then stress-testing the design under conservative assumptions. It also requires attention to guarantees, ongoing costs and how easily the policy can be managed.

- Define the primary goal. Decide whether lifetime death benefit, cash value growth, or premium stability matters most.

- Review guaranteed values. Confirm how the policy behaves under guaranteed crediting and maximum charges.

- Compare current assumptions. Examine the non-guaranteed illustration and ask how rates, caps and charges can change.

- Check funding limits. Make sure planned premiums stay within tax rules and avoid unintended contract classification.

- Plan ongoing monitoring. Set a schedule to review in-force ledgers and adjust premiums if performance shifts.

Using this process makes it easier to compare policies on substance rather than marketing language. It also reduces the chance of buying a design that only works under optimistic projections.

Conclusion

Universal life insurance is permanent coverage with flexible premiums and cash value that grows through interest crediting after policy charges. It can be powerful when structured correctly, but it requires attention to funding, costs and how non-guaranteed elements may change.

The best outcomes come from choosing the right type, focusing on guarantees and monitoring performance over time. With clear goals and realistic assumptions, universal life insurance can provide durable protection and long-term planning flexibility.