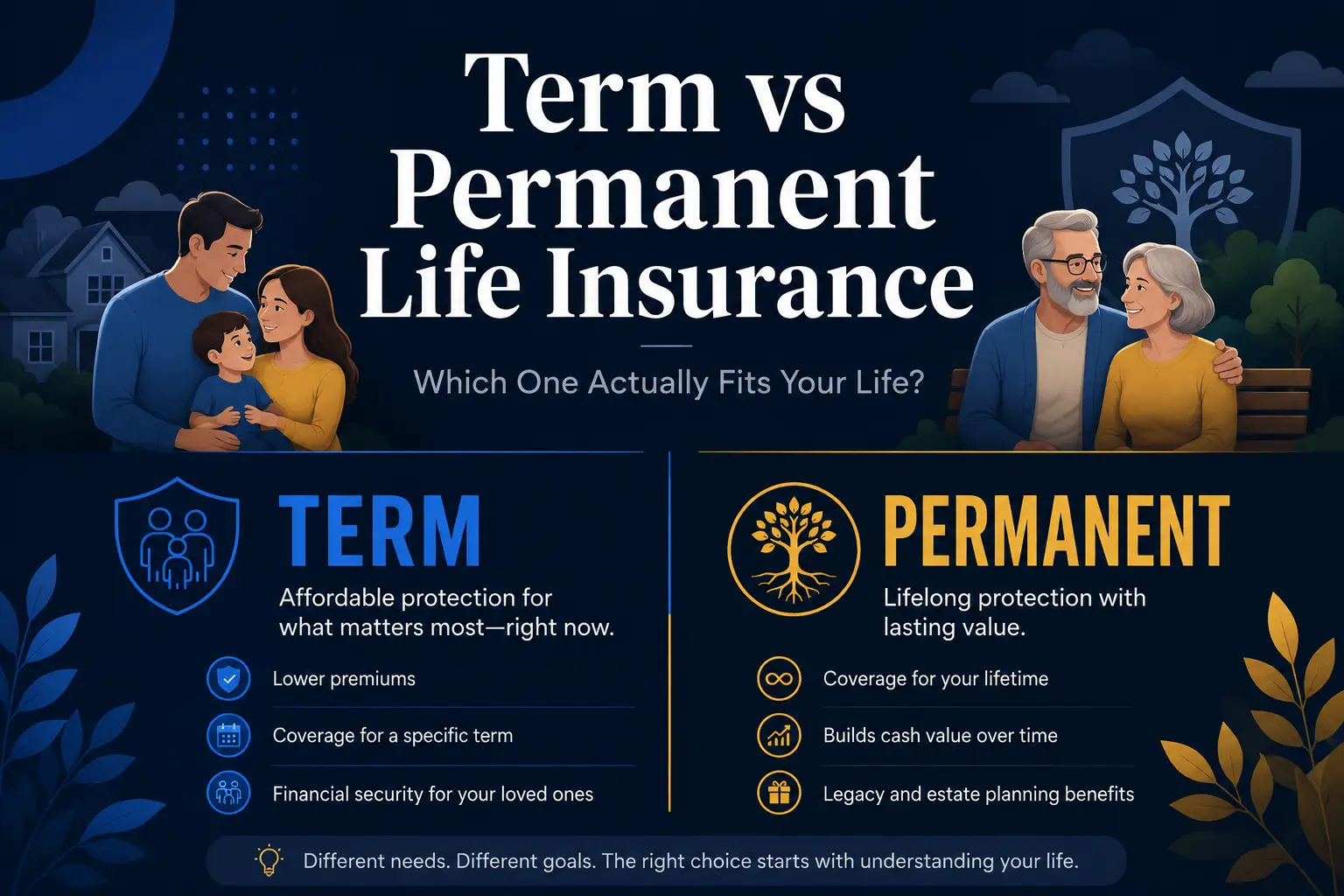

Term life insurance provides coverage for a set period, often 10, 20, or 30 years. If the insured person dies during the term, the policy pays a death benefit to the beneficiaries.

If the term ends and the insured is still living, coverage typically expires unless it is renewed or converted. Term coverage is designed for clear, time-bound needs rather than lifelong planning.

Understanding Whole Life Insurance

Whole life insurance is permanent coverage that can last for the insured’s lifetime as long as premiums are paid. It combines a guaranteed death benefit with a cash value component that can grow over time.

Premiums are usually level, meaning they do not increase as the insured ages. Whole life policies are often used when someone wants both lifelong protection and a structured, contractual savings element.

Key Differences That Affect Real Decisions

Term is mainly about maximizing death benefit per premium dollar for a specific window of time. Whole life is about lifetime coverage, stability and cash value accumulation built into the policy design.

The better option depends on what you need the insurance to do. A policy can be protection-first, wealth planning-oriented, or a blend of both.

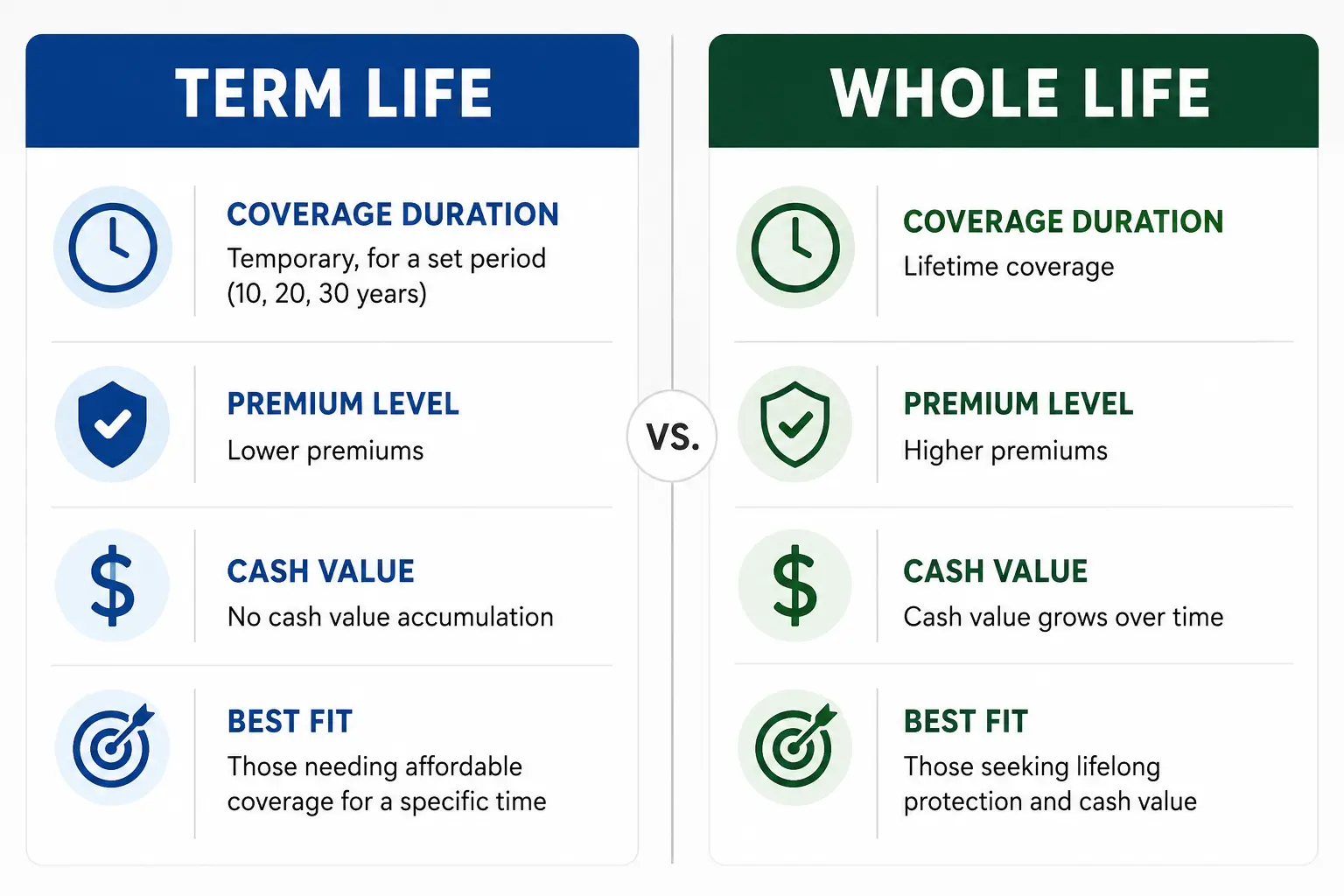

| Feature | Term Life Insurance | Whole Life Insurance |

|---|---|---|

| Coverage Duration | Fixed period such as 10 to 30 years | Lifetime coverage with premiums paid |

| Typical Premium Level | Lower at the start for comparable death benefit | Higher but generally level for life |

| Cash Value | No cash value in most term policies | Cash value grows inside the policy |

| Best Fit | Income replacement and time-limited obligations | Lifelong protection and long-term planning |

The table highlights the practical differences that change how a policy behaves over time. Next, it helps to connect those features to common financial goals.

Cost and Value Over Time

Term usually wins on upfront affordability, which can matter when budgets are tight and coverage needs are high. This makes it easier to buy a larger death benefit early in life when responsibilities often peak.

Whole life costs more because part of each premium supports permanent coverage and builds cash value. The extra cost is not automatically wasteful, but it must match a real purpose in your broader plan.

What You are Paying for With Whole Life?

Whole life premiums fund insurance costs, policy guarantees and cash value growth. Some policies may also be eligible for dividends depending on the insurer and policy type, although dividends are not guaranteed.

It can help to view whole life as insurance plus a conservative asset inside an insurance wrapper. That wrapper brings unique rules, benefits and tradeoffs.

Why Term Can Still Be The Best Value?

If the main goal is to protect dependents during working years, term can deliver strong value per dollar. The difference in premium between term and whole life can be redirected toward retirement savings, debt payoff, or emergency reserves.

That flexibility is powerful, but it relies on consistent follow-through. If saving is irregular, some people prefer the enforced structure that comes with permanent policy premiums.

Coverage Needs and Life Stages

Insurance needs often rise and fall with life events and obligations. Matching policy type to the timeline of your needs reduces the chance of overpaying or ending up underinsured.

Common time-bound needs include paying off a mortgage, replacing income while children are dependent, or covering business loans tied to an owner’s personal guarantee. These are typically aligned with term coverage.

When Permanent Coverage Matters?

Some goals do not have a natural end date. These include lifelong dependent care, estate planning needs and final expenses where the intent is to leave a guaranteed benefit regardless of when death occurs.

Whole life can be suitable when the priority is certainty and long-term stability. It can also play a role when someone wants an asset that is not directly tied to market swings, depending on the policy structure.

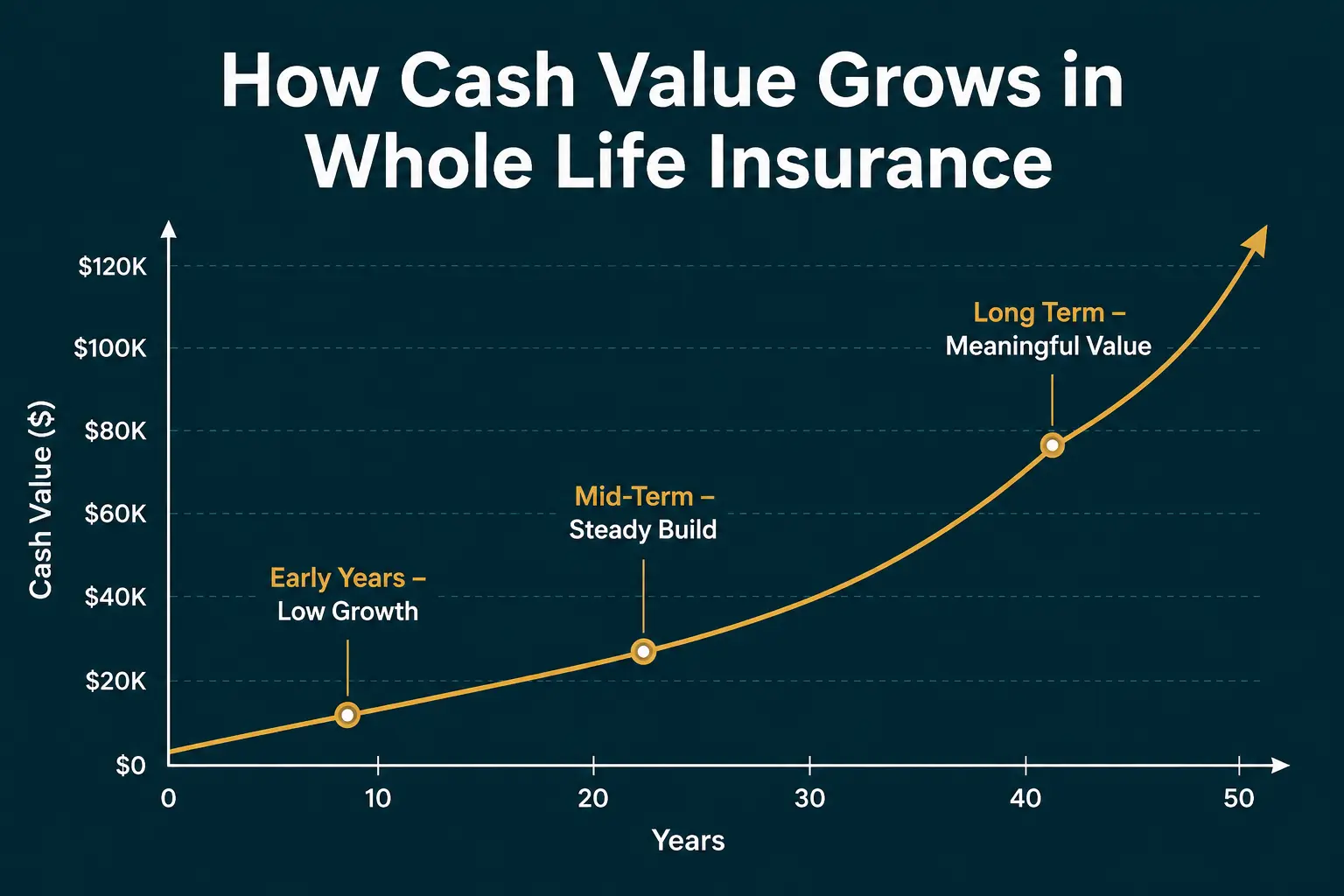

Cash Value Rules You Should Understand

Cash value grows slowly at first in most whole life policies. Early-year costs and policy charges can mean the cash value is lower than total premiums paid for a period of time.

Over the long run, cash value can become meaningful, but it should be evaluated as part of a long-term commitment. Buying whole life with the intent to cancel early often leads to disappointment.

Loans and Withdrawals

Whole life policies often allow borrowing against the cash value, subject to insurer rules. Policy loans can provide liquidity, but unpaid loans and interest can reduce the death benefit and may risk policy lapse if not managed.

Withdrawals can also reduce benefits and may have tax implications depending on the situation. Understanding these mechanics before purchase helps avoid surprises later.

Renewability and Conversion Options

Many term policies include a conversion feature that allows switching to a permanent policy within a set time frame. This can be valuable if health changes and you want to keep coverage without a new medical exam.

Renewing term after the initial period typically increases cost significantly because premiums reflect older age. Planning ahead matters so you do not face a steep jump right when coverage is still needed.

Medical Underwriting and Eligibility

Both term and whole life can require medical underwriting, though requirements vary by insurer and policy size. Age, health history, medications and lifestyle factors can all affect pricing and approval.

Some policies are simplified issue, which can reduce underwriting but raise premiums. If health is a concern, comparing underwriting classes and policy features can matter as much as comparing premium amounts.

Common Mistakes to Avoid

Choosing between term and whole life is easier when you avoid a few predictable errors. These mistakes usually involve buying a policy type that does not match the real goal or keeping the wrong policy too long.

- Buying too little coverage. A small death benefit may not replace income, cover debts and support dependents as intended.

- Overbuying permanent insurance. Paying for lifelong coverage when needs are time-limited can strain cash flow and create regret.

- Ignoring policy details. Conversion windows, riders and premium schedules can change outcomes more than headline pricing.

- Canceling whole life early. Early surrender often results in lower value due to initial costs and surrender charges.

A careful review of goals, timelines and budget can prevent most of these issues. Once the fit is clear, selecting coverage amount and term length becomes more straightforward.

How to Decide Which is Better For You?

No single policy is best for everyone because goals and constraints differ. The better choice is the one that delivers the right protection while keeping your overall finances stable.

Use these criteria to guide the decision and keep it grounded in your personal plan.

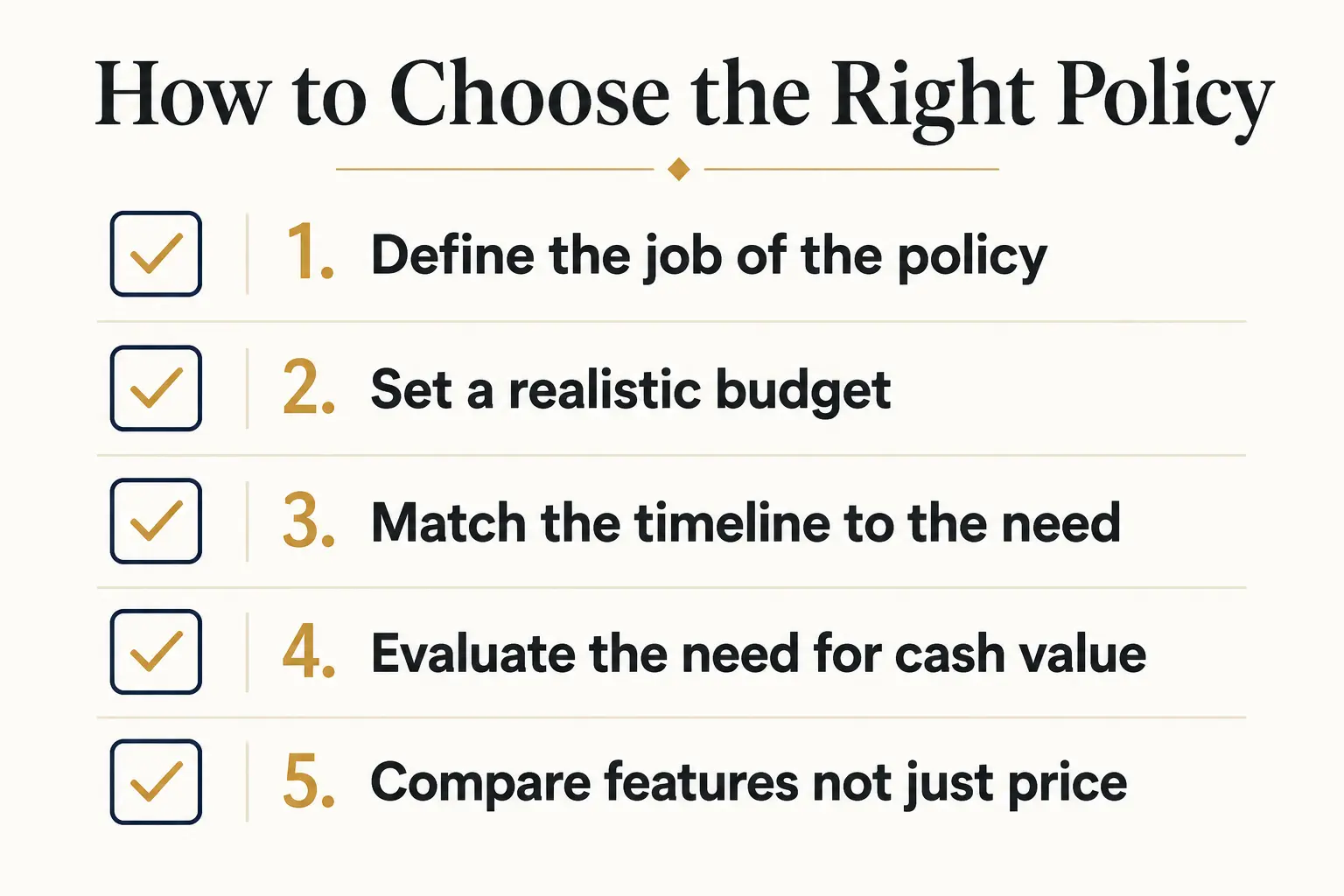

- Define the job of the policy. Decide whether the priority is income replacement for a period or a guaranteed lifetime benefit.

- Set a realistic budget. Choose a premium you can maintain even if expenses rise or income dips.

- Match the timeline to the need. Align term length with debts, dependent years, or retirement targets.

- Evaluate the need for cash value. Confirm whether cash value is truly needed and whether you can commit long term.

- Compare features not just price. Review conversion options, riders, exclusions and policy guarantees.

After you narrow the choice, comparing multiple insurers can help you find better underwriting outcomes and policy terms. That comparison also reveals how different companies structure permanent policy costs and guarantees.

Conclusion

Term life insurance is often better when you need high coverage for a defined period and want the lowest cost way to protect your household. Whole life insurance can be better when you want permanent coverage, stable premiums and cash value as part of a long-term plan.

The right answer depends on your timeline, budget and whether you need lifelong certainty or time-limited protection. A clear goal-first decision usually beats choosing based on premiums alone.