Many people believe that having a health issue automatically disqualifies them from getting life insurance. The good news is that this is not always true. In many cases, getting life insurance with pre existing condition is absolutely possible.

Whether you have diabetes, high blood pressure, asthma, heart disease, or another medical history concern, insurance companies look at many factors—not just the diagnosis itself.

The key is understanding how insurers evaluate risk and which policies may work best for your situation.

Knowing how life insurance with pre existing condition works can help you avoid unnecessary fear and make smarter decisions for your family’s financial protection.

This guide explains your options, what affects approval, and how to improve your chances of getting the right policy.

What Counts as a Pre Existing Condition?

Before understanding life insurance with pre existing condition, it helps to know what insurers usually consider a pre-existing condition.

Common examples include:

- Diabetes

- High blood pressure

- Heart disease

- Asthma

- Cancer history

- High cholesterol

- Sleep apnea

- Anxiety or depression

- Arthritis

- Obesity

- Kidney disease

A pre-existing condition simply means a medical issue that existed before applying for insurance.

It does not automatically mean denial.

This is the first important truth about life insurance with pre existing condition.

Can You Qualify for Life Insurance with Pre Existing Condition?

Yes—many people successfully qualify for life insurance with pre existing condition every day.

Insurance companies review:

- Type of condition

- Severity of the condition

- How well it is managed

- Medications and treatment

- Doctor visit history

- Lifestyle habits

- Smoking status

- Age and overall health

For example, controlled high blood pressure may be viewed very differently from unmanaged heart disease.

Insurers want to understand risk, not just labels.

This is why two people with the same diagnosis may receive very different rates.

How Life Insurance Companies Evaluate Risk

Understanding underwriting helps explain life insurance with pre existing condition more clearly.

Insurance companies may ask:

- When were you diagnosed?

- Are symptoms controlled?

- Have you been hospitalized recently?

- Are you following treatment plans?

- Has your condition improved over time?

Medical exams may also include:

- Blood pressure checks

- Blood tests

- Urine tests

- Height and weight review

The goal is not perfection—it is stability.

A well-managed condition often improves approval chances significantly.

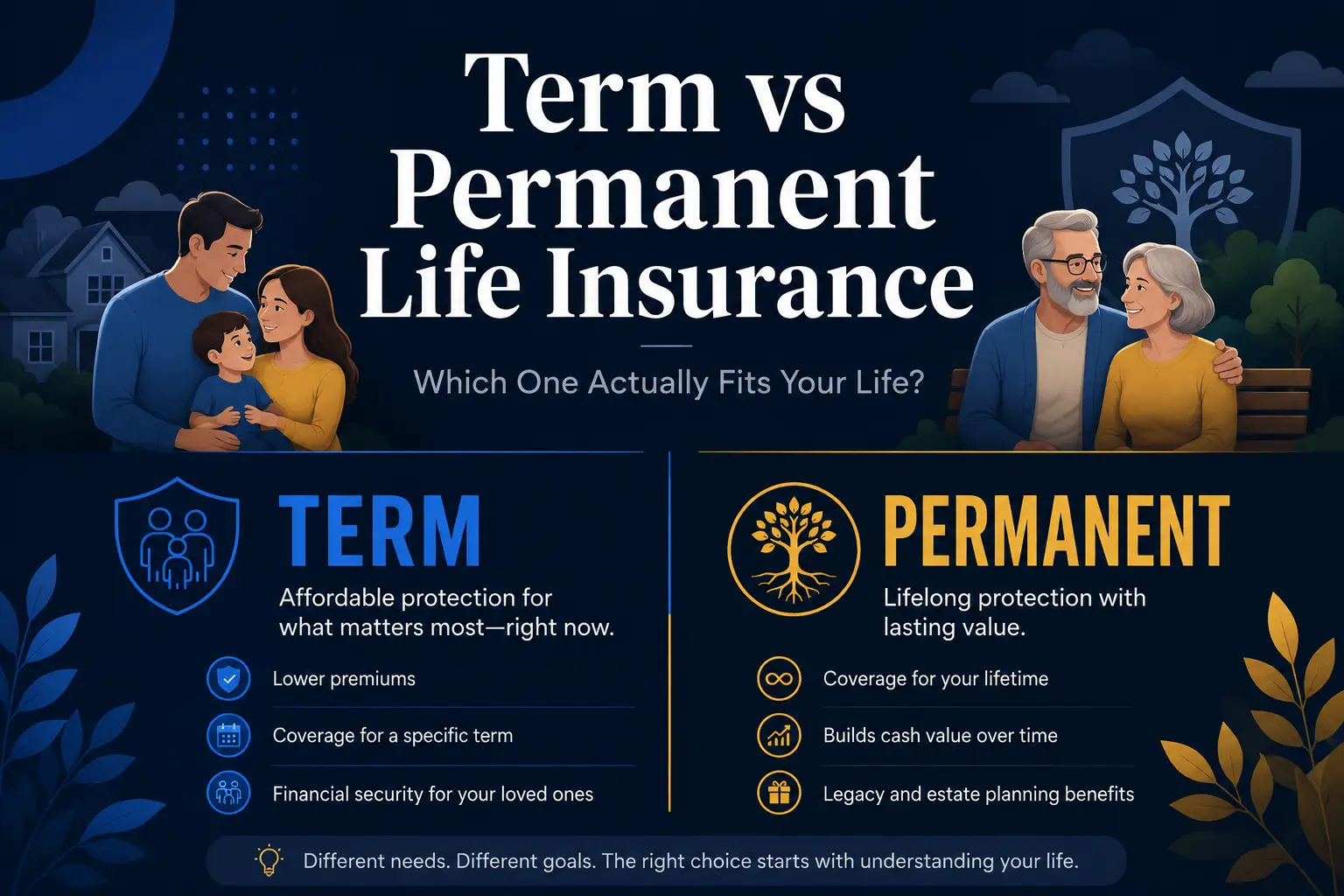

Types of Life Insurance with Pre Existing Condition

There are several options for life insurance with pre existing condition, depending on your health and financial goals.

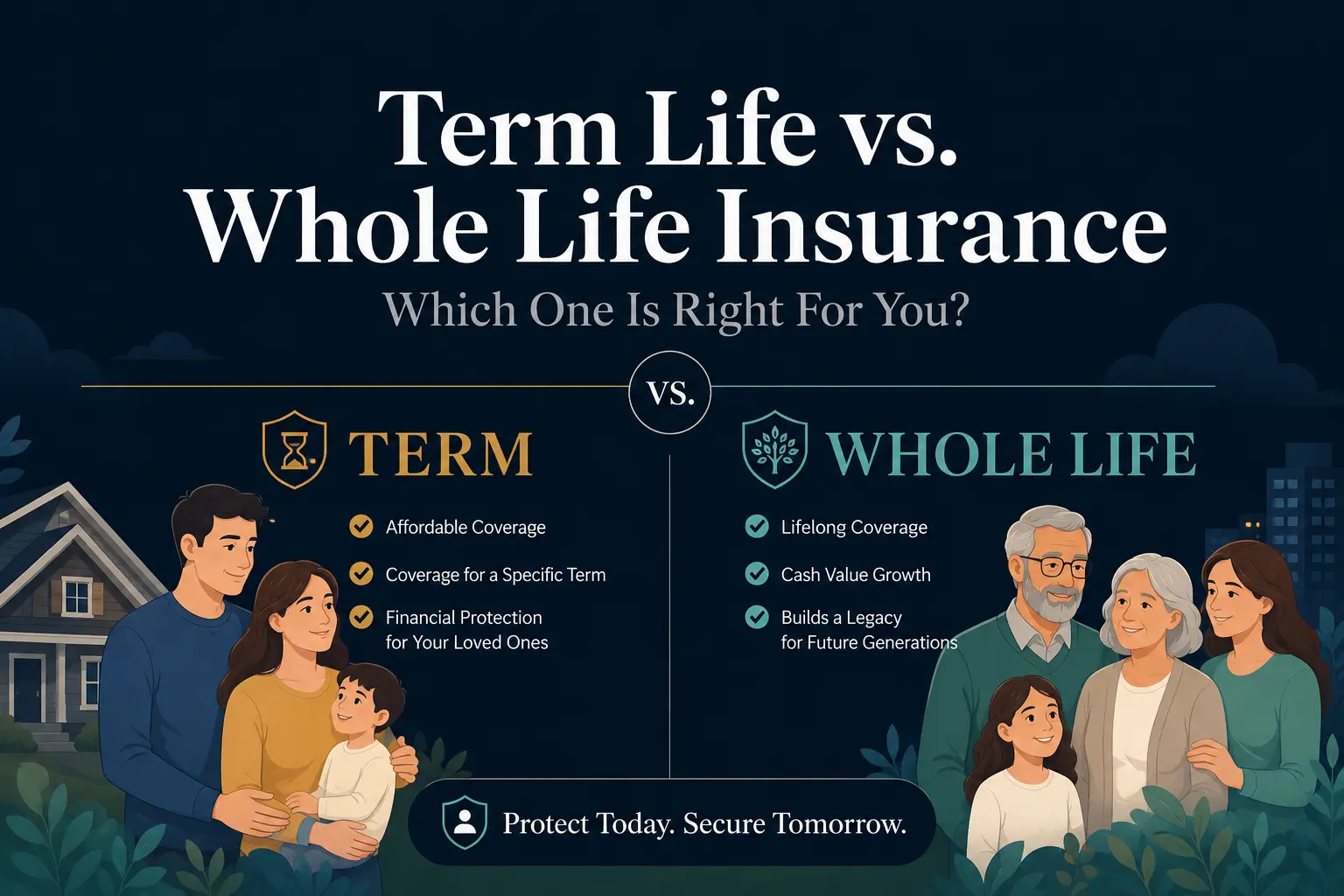

Term Life Insurance

Term life is often the most affordable option.

It provides:

- Coverage for a set number of years

- Lower monthly premiums

- Strong family protection

- Ideal mortgage and income replacement support

If your condition is stable, term life may still be available with standard or slightly higher premiums.

Whole Life Insurance

Whole life insurance offers:

- Lifetime coverage

- Fixed premiums

- Cash value growth

- Long-term financial planning benefits

It may cost more than term life, but it provides permanent protection.

This can be valuable for people seeking estate planning or guaranteed lifetime security.

Guaranteed Issue Life Insurance

This option is often used when medical approval is difficult.

It usually offers:

- No medical exam

- Simplified approval

- Smaller coverage amounts

- Higher premiums

While not ideal for everyone, it can be a valuable backup option for severe health conditions.

It is an important part of life insurance with pre existing condition planning.

Will Life Insurance with Pre Existing Condition Cost More?

Sometimes yes—but not always.

The cost of life insurance with pre existing condition depends on risk level.

For example:

A person with well-managed diabetes may pay only slightly more than someone without it.

But serious unmanaged conditions may create significantly higher premiums.

If a standard policy costs $40 monthly and your condition adds $20:

40+20=6040 + 20 = 60

That means your premium becomes $60 per month.

The goal is not finding the cheapest option—it is finding the best protection your family can rely on.

How to Improve Approval for Life Insurance with Pre Existing Condition

There are smart ways to improve your chances of approval.

Manage Your Health Consistently

Follow treatment plans and medication schedules.

Stop Smoking

Smoking significantly increases premium costs.

Maintain Regular Doctor Visits

Consistent care shows stability and responsibility.

Apply While Your Condition Is Stable

Waiting for health to worsen often creates bigger problems.

Compare Multiple Insurance Providers

Different insurers evaluate risk differently.

This is one of the most important strategies for getting better life insurance with pre existing condition offers.

Why Comparison Matters Most

Not all insurers treat medical history the same way.

One company may offer much better pricing for diabetes, while another may be stronger for heart conditions.

This is why comparing providers is critical when searching for life insurance with pre existing condition.

You should compare:

- Monthly premium costs

- Approval requirements

- Medical exam rules

- Policy flexibility

- Rider availability

- Long-term affordability

If you want to compare trusted providers and better policy options, visit

👉 https://quotemaestro.com/

This helps simplify the process and improves your chances of finding the right coverage.

Final Thoughts: A Health Condition Does Not Mean No Protection

Many people assume a diagnosis means rejection.

That is simply not true.

Getting life insurance with pre existing condition is possible for many families, especially when the condition is stable and the right policy is chosen.

The key is:

- Understanding your options

- Applying strategically

- Comparing providers carefully

- Acting before health worsens

Life insurance is about protecting people—not perfection.

Even with medical history challenges, your family still deserves financial security.

And in many cases, that protection is more available than people think.

❓ FAQs About Life Insurance with Pre Existing Condition

Can I get life insurance with pre existing condition like diabetes?

Yes. Many people with diabetes qualify for life insurance with pre existing condition, especially when the condition is well-managed and regularly monitored.

Is life insurance with pre existing condition always expensive?

Not always. Costs depend on the type of condition, severity, treatment history, and overall health. Some people only pay slightly higher premiums.

Do I need a medical exam for life insurance with pre existing condition?

Sometimes yes. Many traditional policies require medical underwriting, but guaranteed issue policies may offer no-exam options.

What is the best policy for life insurance with pre existing condition?

It depends on your health and goals. Term life is often more affordable, while whole life offers permanent coverage and guaranteed issue policies help when approval is difficult.

Can I be denied life insurance with pre existing condition?

Yes, in some cases, but many people still qualify through alternative policy options or specialized insurers that work with higher-risk applicants.

Where can I compare life insurance with pre existing condition options?

You can compare trusted providers and better policy options by visiting

👉 https://quotemaestro.com/

This helps you find the right coverage for your health situation and family needs.