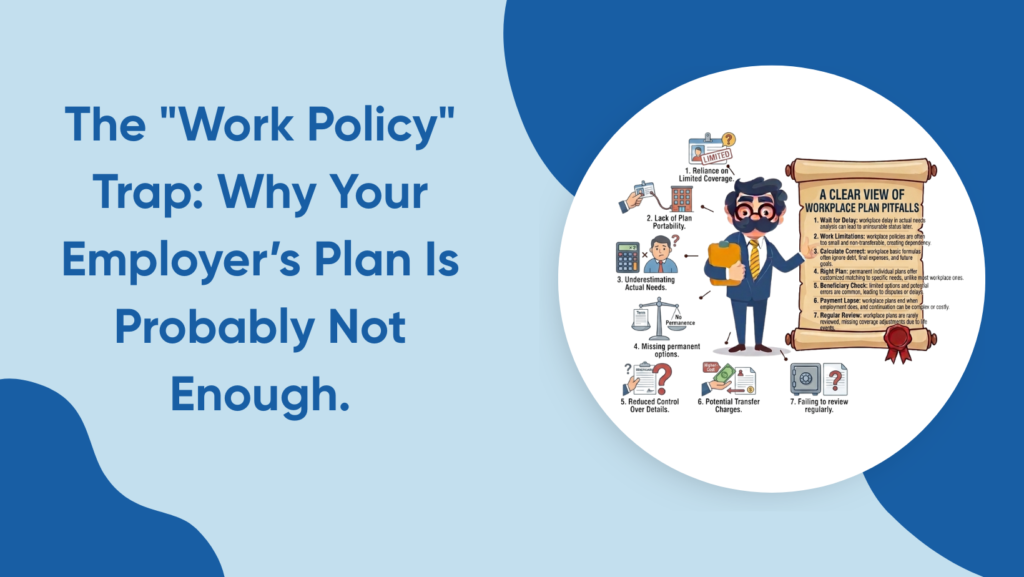

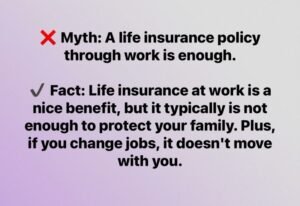

Many people feel secure because they have life insurance through work. It feels automatic, convenient, and often comes at little or no direct cost. But the reality for many families is simple—employer life insurance not enough for true long-term financial protection.

Workplace life insurance is helpful, but it is usually designed as a basic benefit, not a complete financial plan.

If your family depends on your income, your mortgage, your future savings, and your long-term support, relying only on your employer’s plan may leave dangerous financial gaps.

Understanding why employer life insurance not enough can help you avoid one of the most common mistakes in family financial planning.

This guide explains where employer coverage falls short and how to build stronger protection for the people who depend on you most.

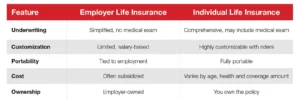

What Employer Life Insurance Usually Includes

Before understanding why employer life insurance not enough, it helps to know what most workplace plans actually provide.

Employer-sponsored life insurance often includes:

- Group life insurance coverage

- Coverage equal to 1x or 2x annual salary

- Automatic enrollment

- Employer-paid or low-cost premiums

- Limited customization options

For example, if your annual salary is $70,000 and your employer offers 2x salary coverage:

70,000×2=140,00070{,}000 \times 2 = 140{,}000

That means your family may receive $140,000 in coverage.

While helpful, that amount may be far below what your family actually needs.

This is the first reason employer life insurance not enough becomes a serious issue.

Why Employer Life Insurance Not Enough for Most Families

Most financial experts recommend life insurance coverage equal to 10 to 15 times your annual income.

Using the same $70,000 income example:

70,000×10=700,00070{,}000 \times 10 = 700{,}000

That suggests your family may need at least $700,000—not just $140,000.

This gap affects:

- Mortgage payments

- Daily household expenses

- Children’s education

- Debt repayment

- Retirement support for your spouse

- Long-term financial stability

This is exactly why employer life insurance not enough for serious family protection.

Your Coverage May Disappear When Your Job Changes

Another major reason employer life insurance not enough is portability.

Your work policy is tied to your employment.

If you:

- Change jobs

- Lose your job

- Start your own business

- Retire early

- Experience layoffs

your employer-sponsored life insurance may end.

That means your family could lose protection during one of the most financially stressful times.

Personal life insurance stays with you, regardless of where you work.

That creates stronger peace of mind.

Employer Plans Often Lack Flexibility

Group life insurance is built for convenience—not customization.

This is another reason employer life insurance not enough for families with specific financial needs.

Many employer plans do not offer:

- Strong rider options

- Child coverage flexibility

- Long-term estate planning benefits

- Cash value growth opportunities

- Retirement income planning features

- Advanced beneficiary planning

Personal life insurance allows you to build protection around your real life—not a standard employee benefits package.

Stay-at-Home Spouses and Hidden Financial Risk

Many families forget that life insurance is not only about the income earner.

This creates another reason employer life insurance not enough.

Stay-at-home spouses often manage:

- Childcare

- School transportation

- Daily home operations

- Meal planning

- Family scheduling

- Household stability

Replacing these responsibilities can be expensive.

Employer life insurance only protects the working employee.

That means major family value may remain completely uninsured.

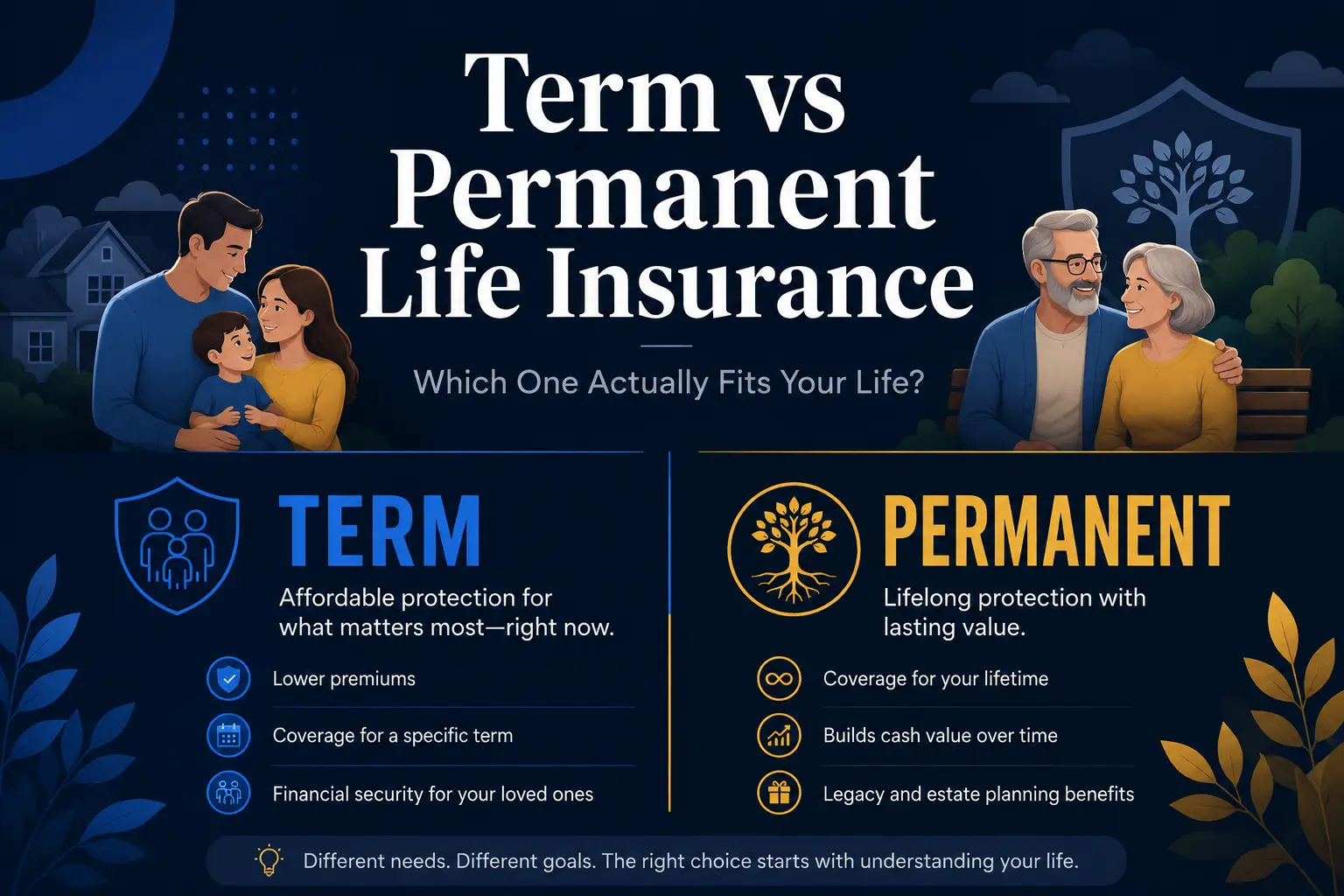

Building Better Protection Beyond Work Coverage

The good news is that employer life insurance not enough does not mean workplace coverage is useless.

It simply means it should be treated as a starting point—not the final solution.

Many families create stronger protection by combining:

- Employer life insurance

- Personal term life insurance

- Permanent life insurance for long-term planning

For example:

- Work coverage handles basic benefits

- Term life protects income replacement and mortgage needs

- Permanent life supports retirement and estate planning

This layered strategy creates stronger overall security.

How to Know If Employer Life Insurance Not Enough for You

Ask yourself:

- Would my family survive financially with only my work policy?

- Could they pay the mortgage and daily expenses?

- Would my children’s education stay protected?

- What happens if I leave my current job?

- Does my spouse also need separate coverage?

If these questions create uncertainty, then employer life insurance not enough is likely true for your situation.

The goal is confidence—not assumptions.

If you want to compare personal life insurance options and stronger family protection plans, visit

👉 https://quotemaestro.com/

This helps you find coverage that truly matches your financial reality.

Final Thoughts: Work Coverage Is a Benefit, Not a Full Plan

The phrase employer life insurance not enough surprises many people because workplace coverage feels safe and reliable.

But convenience is not the same as complete protection.

Employer life insurance is valuable, but it often falls short in:

- Coverage amount

- Long-term portability

- Family customization

- Wealth and retirement planning

Your family deserves more than minimum protection.

They deserve a plan that follows you, grows with you, and protects them no matter what happens at work.

Employer coverage is a great first step.

But real financial security usually requires more.

❓ FAQs About Employer Life Insurance Not Enough

Why is employer life insurance not enough for most families?

Because workplace coverage is often limited to 1x or 2x your salary, which may not be enough for mortgage payments, family expenses, debts, and long-term financial security.

Can I rely only on employer life insurance not enough coverage?

Usually no. Most families need additional personal life insurance because employer coverage alone often creates major financial gaps.

Does changing jobs affect employer life insurance not enough?

Yes. Employer-sponsored life insurance is usually tied to your job, so changing employers or losing your job can mean losing your coverage.

Is term life better if employer life insurance not enough?

Yes. Many people add personal term life insurance because it offers affordable higher coverage and stays with you even when jobs change.

Does my spouse need coverage if employer life insurance not enough?

Yes. Stay-at-home spouses provide major financial value through childcare and household management, so separate protection may be important.

Where can I compare options if employer life insurance not enough?

You can compare trusted personal life insurance plans by visiting

👉 https://quotemaestro.com/

This helps you build stronger protection beyond employer coverage.