Life Insurance Rates Factors matter because they directly impact how much you pay every month for protection.

Insurance companies use risk-based pricing, meaning:

- Higher risk = higher premiums

- Lower risk = lower premiums

Most people only think about age and health, but Life Insurance Rates Factors are much broader than that.

Understanding Life Insurance Rates Factors helps you see why two people with similar coverage can still pay very different premiums. It also gives you better control over your long-term insurance costs.

Why Insurance Companies Use Life Insurance Rates Factors

Insurance companies are not guessing when they set prices. They use data, statistics, and risk models to decide how likely a claim is to happen.

That is why Life Insurance Rates Factors are so important in pricing decisions.

They evaluate:

- How long a person is likely to live

- The probability of health issues

- Financial risk exposure

- Lifestyle habits that affect longevity

All of these elements combine into a personalized risk score, which determines your final premium.

How Small Changes Affect Life Insurance Rates Factors

One of the most surprising things about Life Insurance Rates Factors is how small lifestyle changes can make a big difference.

For example:

- Quitting smoking can reduce premiums significantly over time

- Improving fitness can lower risk classification

- Managing blood pressure can improve eligibility

- Choosing a safer job role can reduce risk ratings

Even simple daily habits influence how insurers view your overall risk profile.

Why Two People Pay Different Premiums

Even if two people choose the same coverage amount, their premiums can still be very different because Life Insurance Rates Factors are personalized.

Insurers look at:

- Medical history

- Family health background

- Lifestyle habits

- Occupation risk level

- Driving record

- Financial stability

This is why your friend may pay less—even with similar coverage.

Understanding this helps you avoid comparing policies incorrectly and instead focus on improving your own profile.

How You Can Take Control of Your Life Insurance Rates

The good news is that Life Insurance Rates Factors are not completely out of your control.

You can actively improve your situation by:

- Maintaining a healthy lifestyle

- Avoiding risky habits

- Buying insurance earlier in life

- Comparing multiple providers

- Choosing the right policy type

Small improvements today can lead to long-term savings on premiums.

👉 You can compare options here: https://quotemaestro.com/

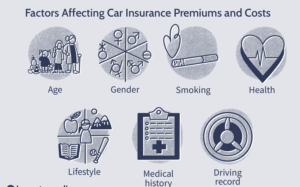

✔️ 1. Your Age (The Biggest Factor)

Age is one of the strongest factors affecting life insurance pricing.

The younger you are, the lower your risk profile. Even a 1–2 year delay can increase your premium because insurers see older applicants as higher risk.

This is why buying early usually locks in better long-term pricing.

✔️ 2. Your Health Condition

Health is another major pricing factor in life insurance.

Conditions like:

- Diabetes

- High blood pressure

- Heart issues

- Obesity

can significantly increase your cost because insurers assess long-term medical risk before approving coverage.

Even small improvements in health can sometimes lead to better rates over time.

✔️ 3. Smoking or Vaping Habits

Tobacco use is one of the most expensive pricing factors in life insurance.

Smokers can pay 2–3 times more than non-smokers because of higher long-term health risks.

Even switching to non-smoking status (after a qualifying period) can sometimes reduce premiums.

✔️ 4. Your Occupation Risk Level

Your job also plays a big role in pricing.

High-risk jobs like:

- Construction work

- Piloting

- Truck driving

- Mining

can increase premiums because insurers evaluate workplace safety and accident exposure.

Office-based jobs usually receive lower rates due to reduced physical risk.

✔️ 5. Your Lifestyle Choices

Lifestyle habits also influence underwriting decisions.

This includes:

- Extreme sports

- Alcohol consumption

- Frequent high-risk travel

Insurers consider these as behavioral risk indicators that may increase claim probability.

Maintaining a balanced lifestyle can help keep premiums stable.

✔️ 6. Coverage Amount You Choose

The higher your coverage, the higher your premium.

For example:

500,000×2=1,000,000500{,}000 \times 2 = 1{,}000{,}000

Choosing $1M coverage instead of $500K naturally increases cost, but it also provides stronger financial protection for your family.

It’s important to balance affordability with real coverage needs.

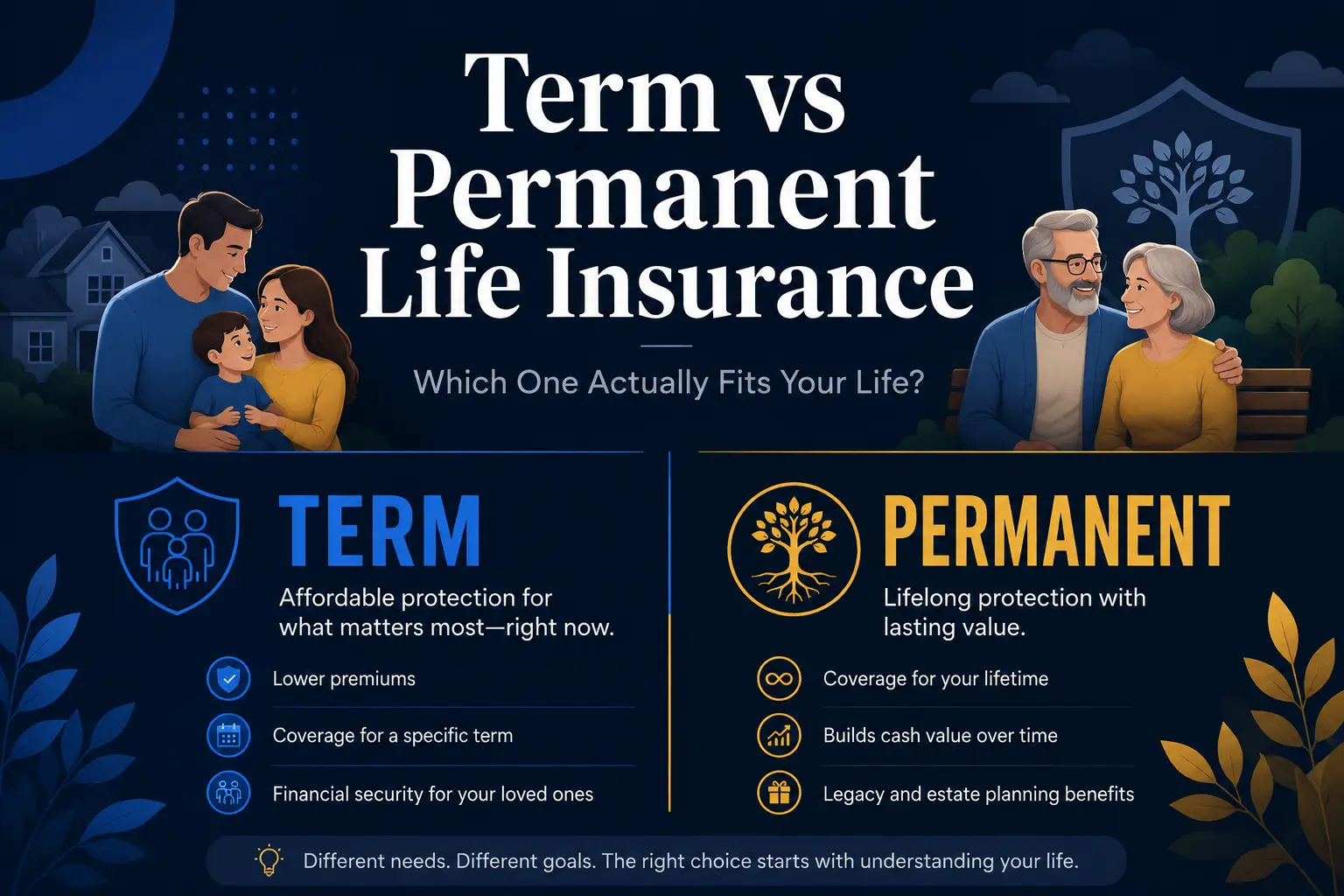

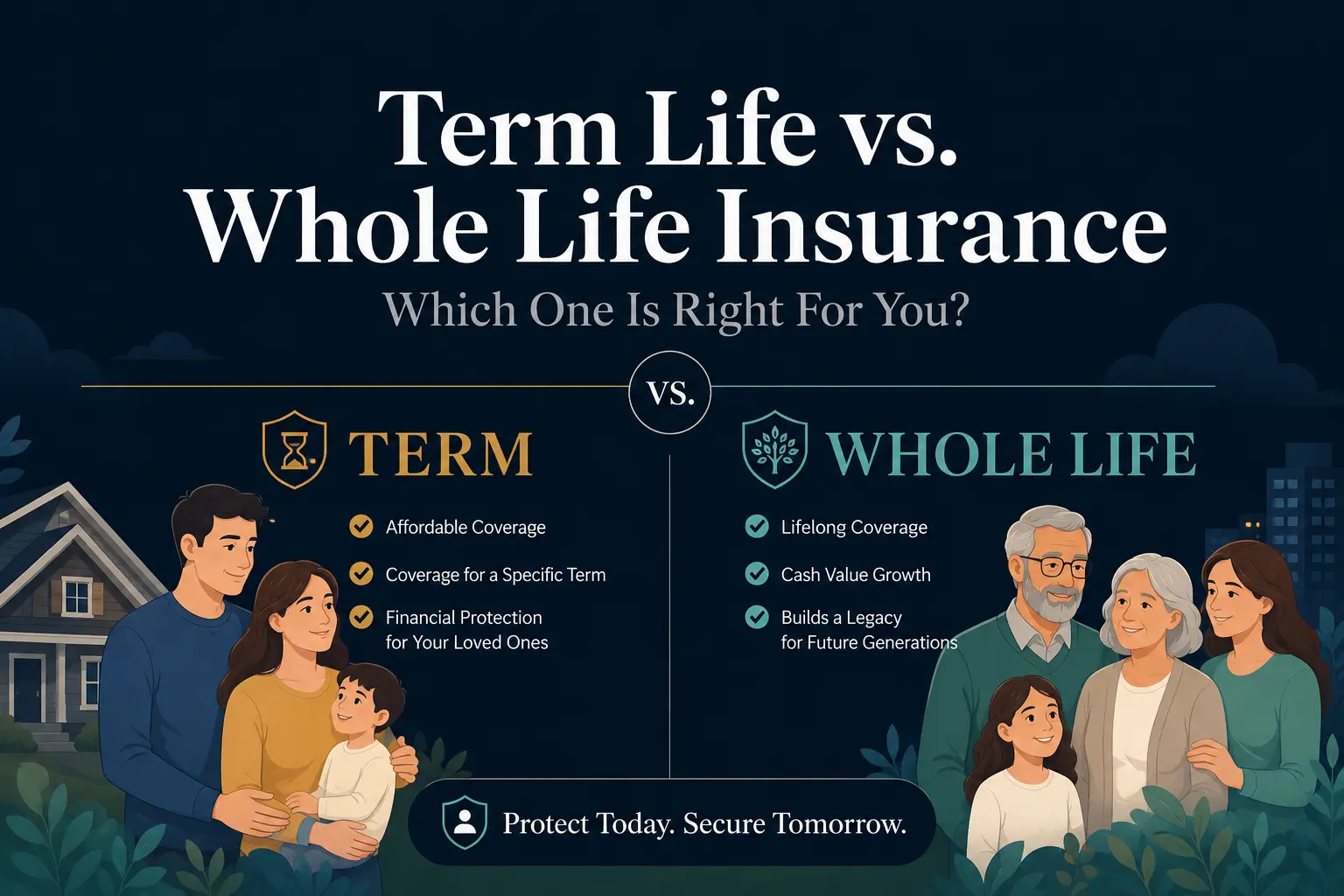

✔️ 7. Policy Type (Term vs Whole Life)

Policy type significantly affects pricing.

- Term life = lower cost, temporary coverage

- Whole life = higher cost, lifetime protection + cash value

Your choice should depend on whether you want affordability or long-term financial benefits.

✔️ 8. Family Medical History

Family health history can influence pricing decisions.

If close relatives experienced early serious illnesses, insurers may adjust your risk profile slightly higher.

However, lifestyle improvements can sometimes offset part of this impact.

✔️ 9. Gender Differences

Gender can also affect pricing.

Statistically, women tend to live longer, which often results in lower premiums compared to men of the same age and health profile.

This is based on actuarial risk calculations.

✔️ 10. Your Driving Record

Your driving history is another overlooked factor.

A record of:

- Accidents

- Speeding tickets

- DUIs

can increase premiums because insurers see driving behavior as a reflection of overall risk habits.

Safe driving history can help keep costs lower.

How to Reduce Your Life Insurance Costs

While you cannot control every factor, you can actively improve many of them to lower your premium over time.

Here’s what helps:

- Quit smoking

- Improve fitness and health markers

- Buy coverage at a younger age

- Choose term insurance when appropriate

- Compare multiple insurers before finalizing

Small improvements in lifestyle and timing can lead to meaningful long-term savings.

👉 You can compare affordable options here:

https://quotemaestro.com/

Added Value Insight (Important)

Most people think insurance pricing is fixed, but it’s not.

Insurers continuously evaluate risk patterns, which means improving your health and habits today can still positively impact future renewals or new policies.

💖 Final Thoughts

Life insurance pricing is more detailed than most people expect.

It’s not just about age or health—it’s a mix of lifestyle, financial habits, and personal risk factors.

Understanding how pricing works helps you:

- Pay more reasonable premiums

- Choose the right coverage

- Avoid costly mistakes

- Protect your family with confidence

Smart planning today can lead to long-term savings and better financial security.

❓ FAQs

What factors affect life insurance pricing?

Insurance companies consider age, health, smoking habits, occupation, and coverage amount when calculating premiums.

Which factors have the biggest impact on cost?

Age, medical history, and lifestyle choices usually have the strongest impact on pricing.

Can I reduce my insurance premium?

Yes, improving your health, quitting smoking, and comparing providers can help lower costs.

Does my job affect my insurance price?

Yes, high-risk jobs can increase premiums due to greater risk exposure.

Why do premiums vary between people?

Because insurers assess each person’s risk individually based on multiple personal and financial factors.

Where can I compare insurance options?