If you’ve been researching life insurance lately, you’ve probably noticed one thing: Indexed Universal Life Insurance keeps popping up everywhere.

Agents are recommending it. Financial influencers are talking about it. And more families are choosing it over traditional policies.

So what’s going on?

Let’s break it down in simple terms—no jargon, no fluff—just real insight into why this type of coverage is exploding in popularity.

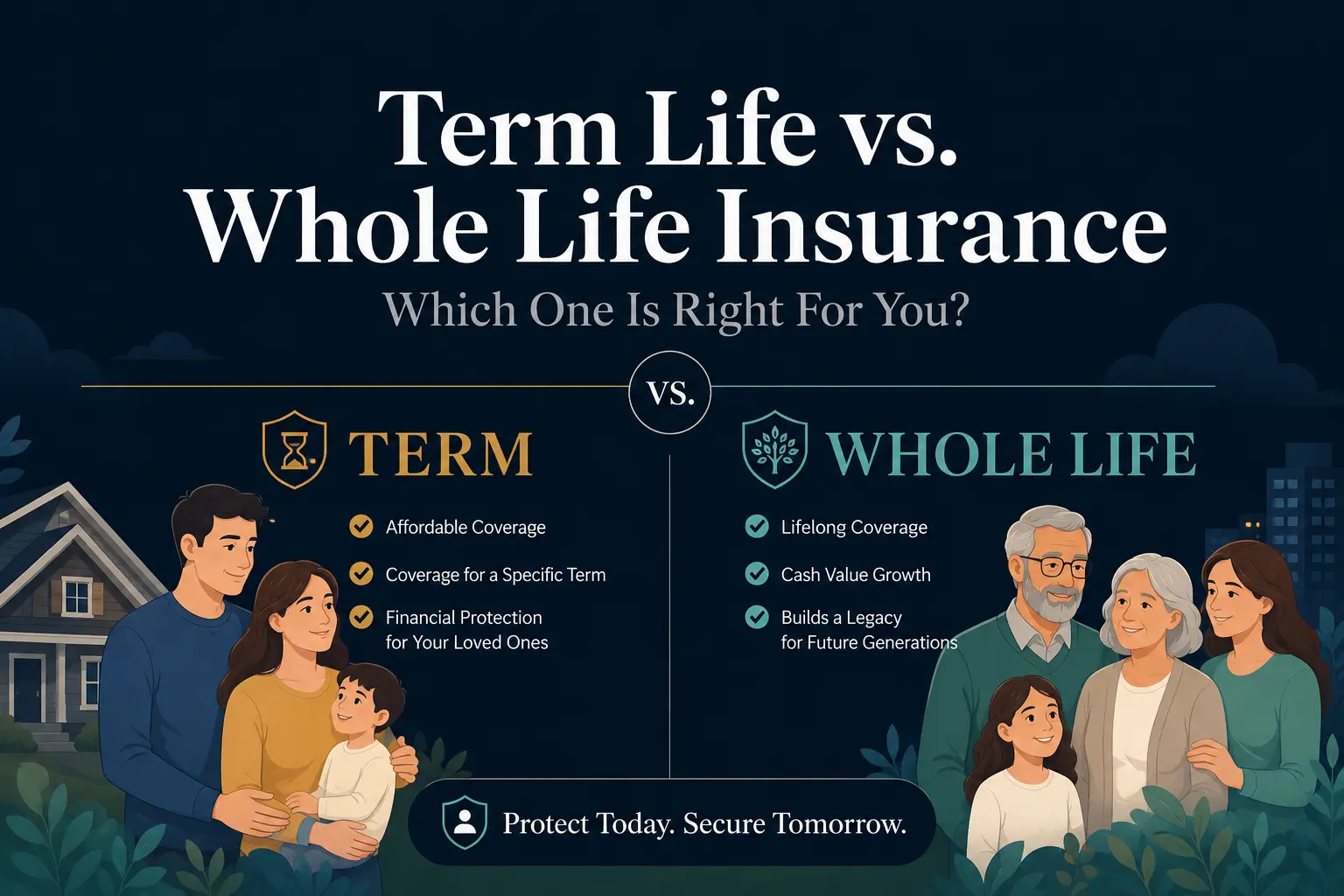

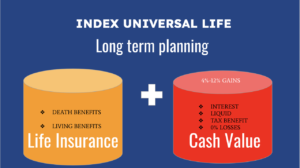

What Is Indexed Universal Life Insurance?

Indexed Universal Life Insurance (IUL) is a type of permanent life insurance that combines:

- A death benefit (like traditional life insurance)

- A cash value component that grows over time

- Growth tied to a stock market index (like the S&P 500)

But here’s the twist:

👉 You’re not directly investing in the stock market

Instead, your policy earns interest based on market performance—with built-in protection from losses.

Why Indexed Universal Life Insurance Is So Popular Right Now

1. Market Growth Without Market Risk

People want growth—but they don’t want to lose money.

With Indexed Universal Life Insurance:

- You benefit when the market goes up

- You’re protected when the market goes down (thanks to a floor, usually 0%)

That’s a powerful combination, especially in uncertain economic times.

2. Tax-Advantaged Wealth Building

This is where things get interesting.

The cash value in an Indexed Universal Life Insurance policy grows:

- Tax-deferred

- Can be accessed through tax-free loans

For many people, this becomes a supplemental retirement strategy.

👉 Want to explore strategies like this? Check out:

https://quotemaestro.com/

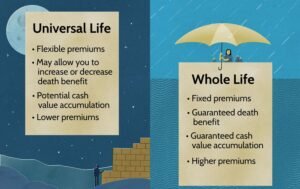

3. Flexibility That Traditional Policies Don’t Offer

Unlike whole life insurance, IUL policies are flexible:

- Adjust your premium payments

- Increase or decrease your death benefit

- Use cash value when needed

This flexibility makes it attractive for:

- Young families

- Business owners

- High-income earners

4. Living Benefits Are a Game-Changer

Many Indexed Universal Life Insurance policies now include living benefits, meaning you can access your policy while you’re alive if:

- You’re diagnosed with a serious illness

- You need long-term care

- You face a medical emergency

This turns life insurance into more than just a “death benefit”—it becomes a financial safety net.

5. It Fits Modern Financial Planning

Today’s financial planning isn’t just about protection—it’s about:

- Growth

- Tax efficiency

- Flexibility

Indexed Universal Life Insurance checks all three boxes.

That’s why financial professionals are increasingly positioning it as a hybrid solution.

But Is Indexed Universal Life Insurance Too Good to Be True?

Let’s be real—it’s not perfect.

Here are a few things to watch out for:

⚠️ Caps on Returns

Your gains are usually limited (e.g., 8–12%), even if the market performs better.

⚠️ Complexity

These policies can be complicated. If you don’t understand how they work, you could make poor decisions.

⚠️ Fees

There are costs involved, especially in the early years.

👉 That’s why working with a knowledgeable advisor matters.

Who Should Consider Indexed Universal Life Insurance?

This type of policy isn’t for everyone, but it can be a great fit if you:

- Want lifelong coverage

- Are looking for tax-advantaged growth

- Have maxed out traditional retirement accounts

- Prefer lower risk than direct stock investing

- Want flexible financial options

Real Talk: Why It’s “Taking Over”

Indexed Universal Life Insurance is gaining traction because it aligns with what people want today:

✔ Protection

✔ Growth potential

✔ Tax advantages

✔ Flexibility

It’s not just insurance anymore—it’s becoming part of a bigger financial strategy.

Final Thoughts

The rise of Indexed Universal Life Insurance isn’t random—it reflects a shift in how people think about money, risk, and long-term planning.

But like any financial product, it only works if it’s used correctly.

Before jumping in, take time to understand the structure, costs, and benefits—and make sure it fits your goals.

👉 Want to compare options or see if it’s right for you? Visit:

https://quotemaestro.com/

❓ FAQs About Indexed Universal Life Insurance

1. What is Indexed Universal Life Insurance in simple terms?

Indexed Universal Life Insurance is a permanent life insurance policy that builds cash value based on market index performance while protecting you from losses.

2. Is Indexed Universal Life Insurance a good investment?

It’s not a pure investment, but it can be a strong financial tool for tax-advantaged growth and long-term planning.

3. Can I lose money in Indexed Universal Life Insurance?

You typically won’t lose money due to market drops, but fees and poor structuring can reduce your cash value.

4. How is Indexed Universal Life Insurance different from whole life insurance?

IUL offers more flexibility and market-linked growth, while whole life provides fixed, guaranteed returns.

5. Who should avoid Indexed Universal Life Insurance?

People looking for simple, low-cost coverage or those who don’t want complexity may prefer term life insurance instead.