Life insurance exists to transfer financial risk away from the people who depend on you. It creates a tax-advantaged pool of money that can replace income, settle obligations and protect plans when a death occurs.

At its core, the purpose is stability. A policy can turn an unpredictable loss into predictable resources that help survivors keep housing, education and daily life on track.

Financial Protection for Loved Ones

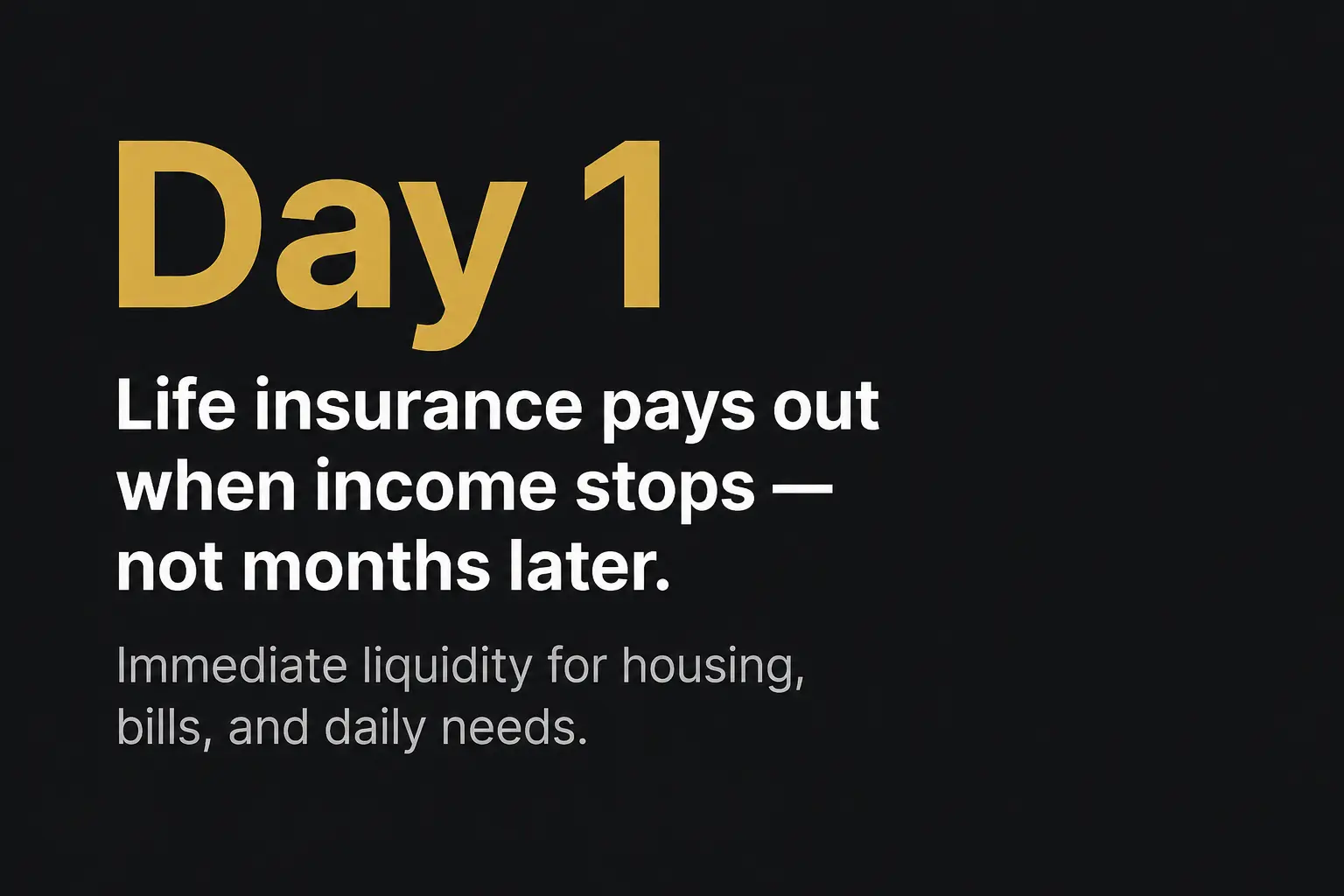

The most direct purpose of life insurance is to protect people who rely on your earnings or unpaid work. When a paycheck stops, families often face immediate cash needs alongside long-term income gaps.

A death benefit can provide liquidity at the moment it is needed most. That funding can support routine bills while giving survivors room to make careful decisions instead of rushed ones.

Income Replacement and Household Continuity

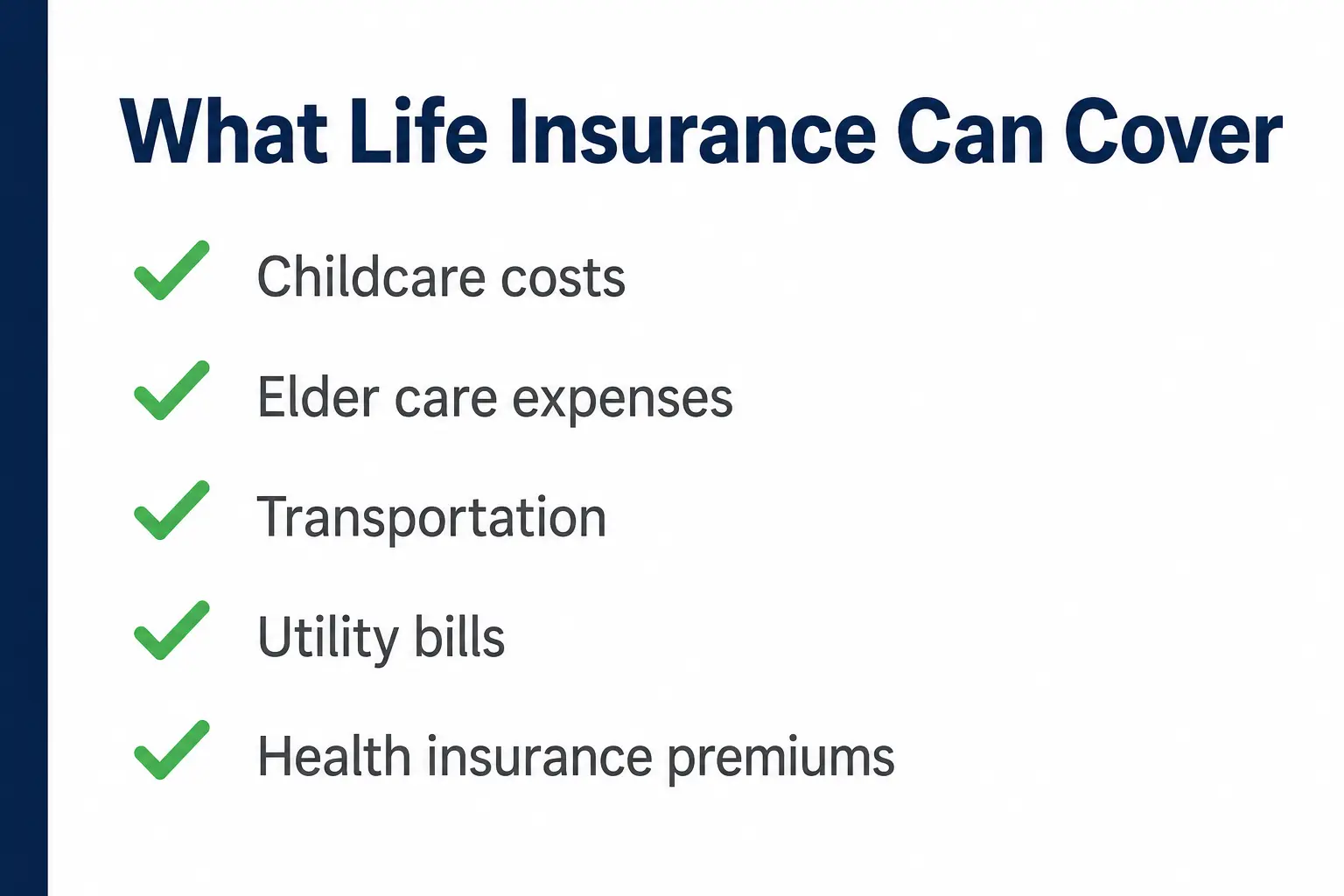

Many households depend on one or two incomes plus the value of caregiving and household management. Life insurance can cover both by providing cash that substitutes for earnings and helps pay for services a family now must purchase.

Common continuity needs include childcare, elder care, transportation, utilities and health insurance premiums. Coverage can be sized to match the years of support survivors would realistically require.

Debt Coverage and Final Expenses

Another key purpose is to prevent debts and end-of-life costs from falling onto surviving family members. Even when some debts are not inherited, obligations tied to shared assets and ongoing expenses can still create pressure.

Life insurance can provide a simple way to pay these costs quickly. That reduces the chance of missed payments, forced sales, or use of high-interest credit.

- Funeral and burial costs that can arrive before estates are settled.

- Mortgage or rent commitments that keep housing stable for dependents.

- Auto loans and personal loans that may affect co-borrowers or shared budgets.

- Credit card balances that can strain cash flow even when not legally transferred.

Handled thoughtfully, coverage can act as a buffer that keeps short-term expenses from turning into long-term financial damage.

Estate Planning and Wealth Transfer

Life insurance can also support estate planning by providing cash that is separate from market timing and asset sales. That liquidity can help heirs maintain property, keep a business intact, or cover costs associated with administering an estate.

Policies are often used to balance inheritances when one heir receives a non-divisible asset such as a home or business interest. Life insurance proceeds can provide an offset so distributions feel fair without forcing liquidation.

Liquidity When Assets are Illiquid

Some families are asset-rich but cash-poor, especially when wealth is tied up in real estate, retirement accounts, or privately held businesses. Life insurance can create cash on demand to prevent sales under pressure.

This can be particularly valuable when markets are down or when buyers are scarce. Access to immediate funds can protect long-term value and family intent.

Business Continuity and Key Person Protection

Life insurance is not only personal. In business settings, it can support continuity when an owner, partner, or essential employee dies.

When properly structured, it can help fund buy-sell agreements, stabilize cash flow and cover recruitment or transition costs. This reduces disruption for employees, customers and surviving owners.

- Buy-sell funding can provide capital so remaining owners can purchase a deceased partner’s share.

- Key person coverage can offset revenue loss and pay for training or hiring.

- Loan protection can reassure lenders and keep credit terms stable.

These uses depend on clear ownership, beneficiary designations and legal agreements that align with the policy structure.

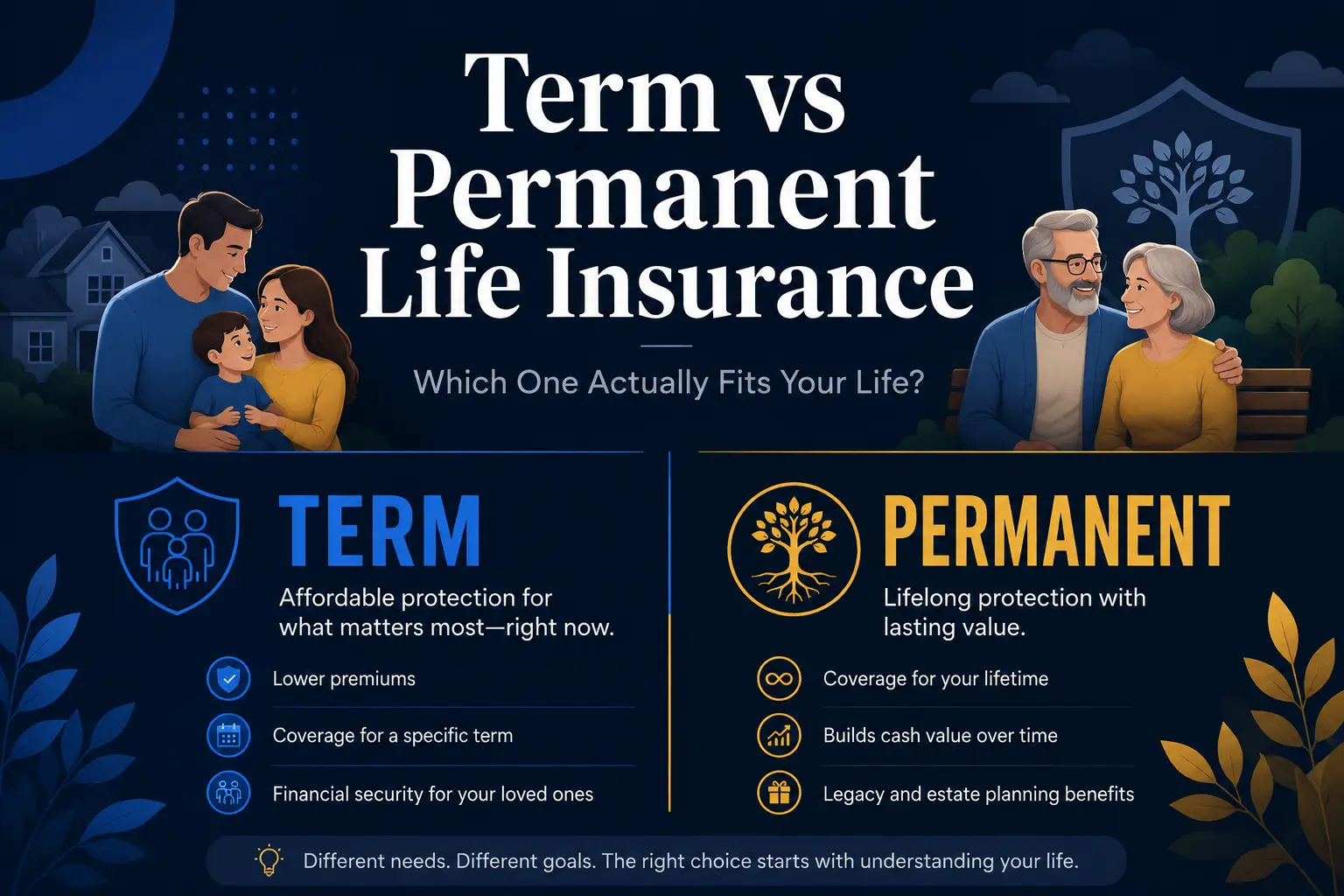

Types of Life Insurance and What They are Designed To Do?

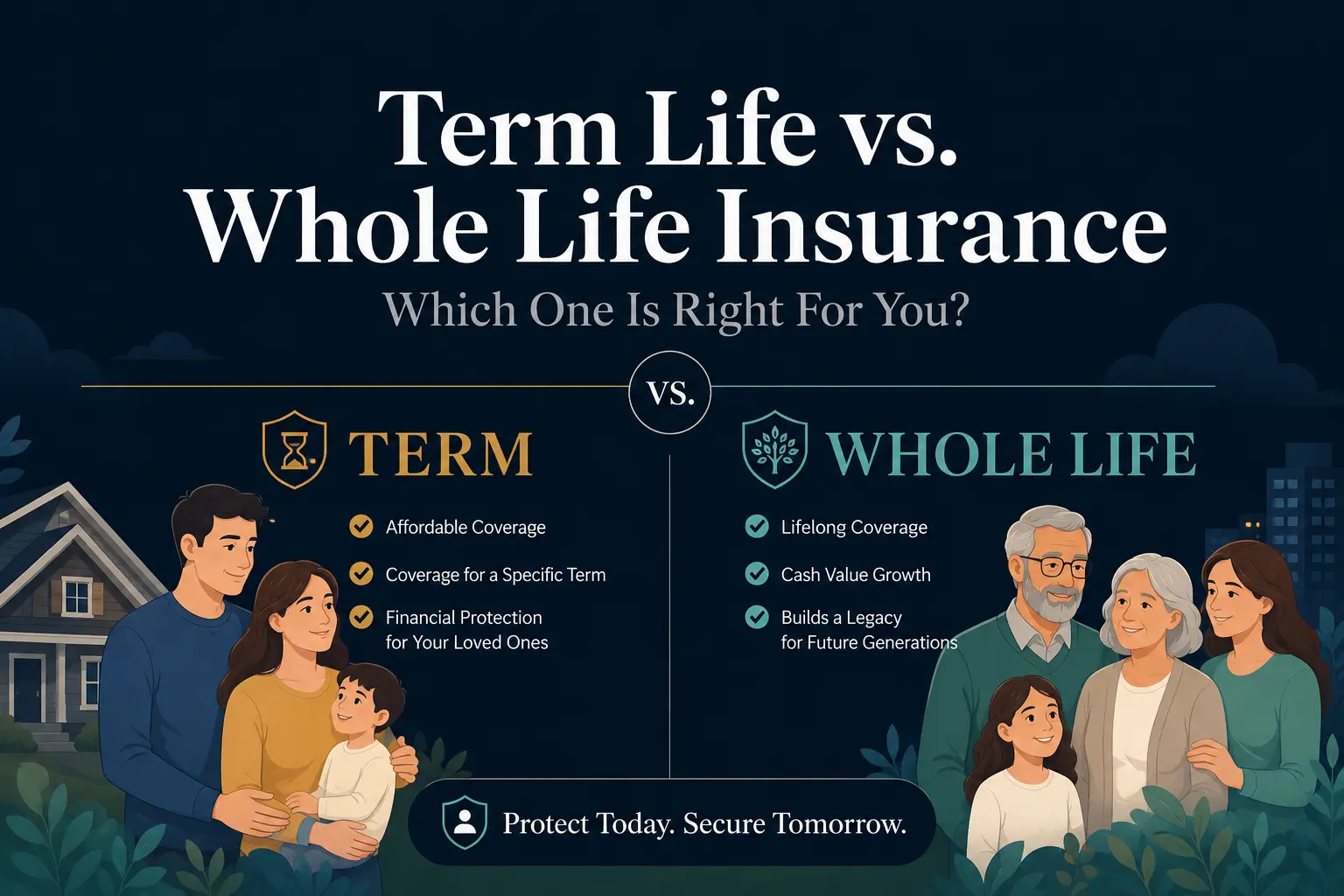

Different products serve different purposes and matching the policy type to the goal matters. The main choice is usually between term life insurance and permanent life insurance.

Term coverage focuses on protection for a set period, while permanent coverage can last for life and may build cash value. The right fit depends on your time horizon, budget and whether lifelong coverage is needed.

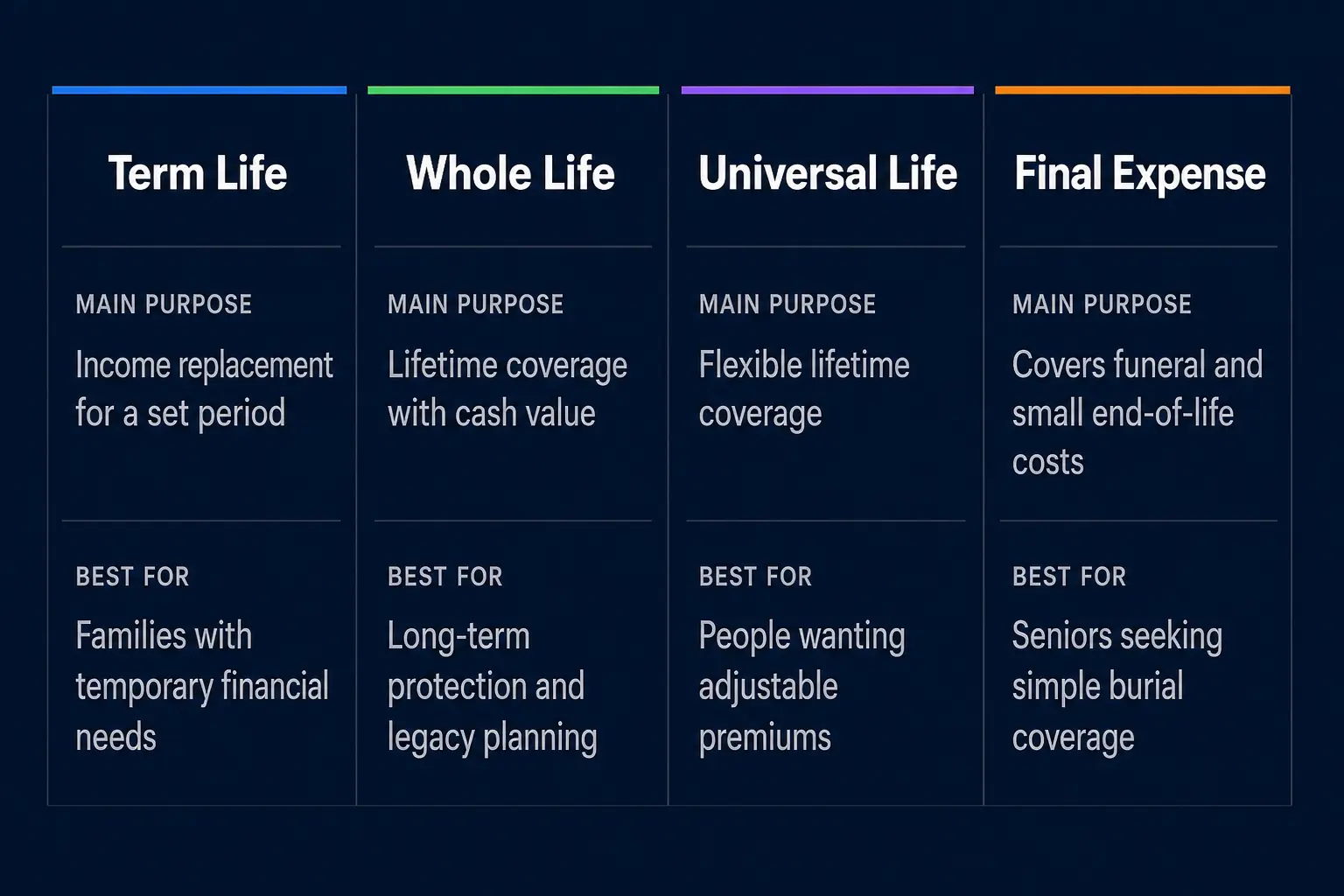

| Policy Type | Main Purpose | Best Fit When |

|---|---|---|

| Term Life | High death benefit for a lower cost during working years | Income replacement is needed for a set period |

| Whole Life | Lifelong coverage with guaranteed features and cash value | Long-term planning needs stable, predictable protection |

| Universal Life | Flexible premiums with potential cash value growth | Needs may change and flexibility is a priority |

| Final Expense | Smaller coverage focused on funeral and end-of-life costs | Primary goal is reducing immediate expenses for family |

Term Life Insurance Purpose

Term life insurance is designed to cover financial obligations that decline over time. These commonly include child-rearing years, a mortgage payoff period, or the span until retirement savings are sufficient.

Because it is generally more affordable for a given death benefit, it is often used for large protection needs with a clear endpoint. The goal is straightforward risk coverage, not accumulation.

Permanent Life Insurance Purpose

Permanent life insurance is designed for needs that do not end at a specific age. It can support estate liquidity, long-term dependent care, or legacy goals where coverage must remain in force indefinitely.

Some permanent policies build cash value that can be accessed under certain conditions. That feature should be evaluated carefully, since costs, guarantees and performance assumptions vary by product.

How Much Coverage Matches The Purpose?

Coverage amount should reflect the problem you are trying to solve. A policy meant to cover final expenses will look very different from one meant to replace decades of income or fund a business agreement.

Start with major obligations and add ongoing needs, then subtract resources survivors can realistically access. The goal is a practical number that supports a plan rather than a guess.

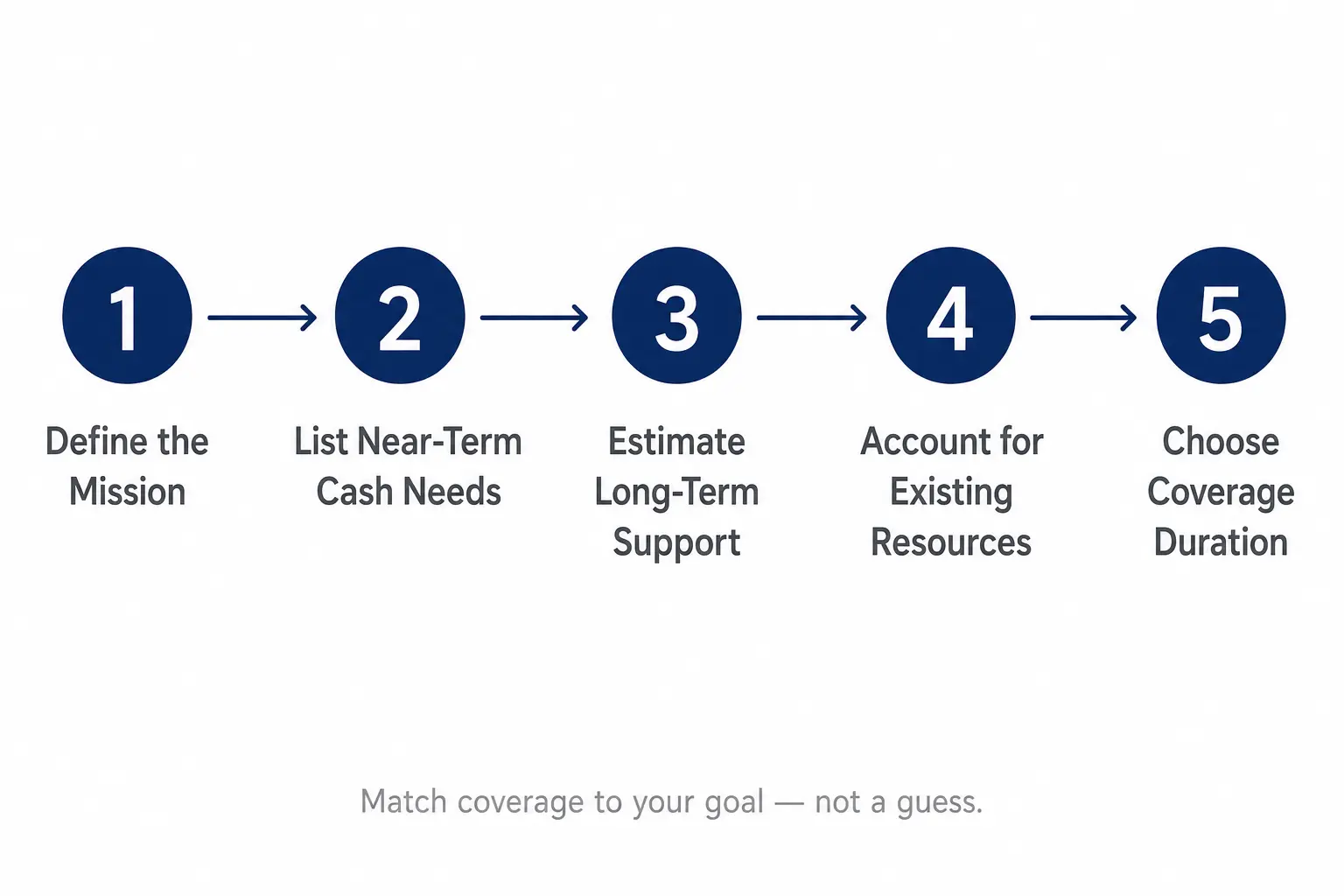

- Define the mission. Decide whether the priority is income replacement, debt payoff, estate liquidity, business continuity, or a combination.

- List near-term cash needs. Include funeral costs, emergency funds and several months of essential expenses.

- Estimate long-term support. Consider housing costs, child or dependent care, education goals and health insurance coverage.

- Account for existing resources. Review savings, retirement accounts, employer benefits and any other insurance already in place.

- Choose a coverage duration. Align term length or permanent coverage with how long the need will exist.

Once the purpose is clear, selecting a product and amount becomes a calmer decision with fewer tradeoffs hidden in the fine print.

Beneficiaries and Payout Clarity

Life insurance only fulfills its purpose if the payout reaches the right people in the right way. Beneficiary designations control who receives the death benefit and they should be kept current after major life changes.

Clear designations can reduce delays and conflict. They also help ensure that proceeds support intended dependents rather than drifting into avoidable disputes.

Common Planning Details That Matter

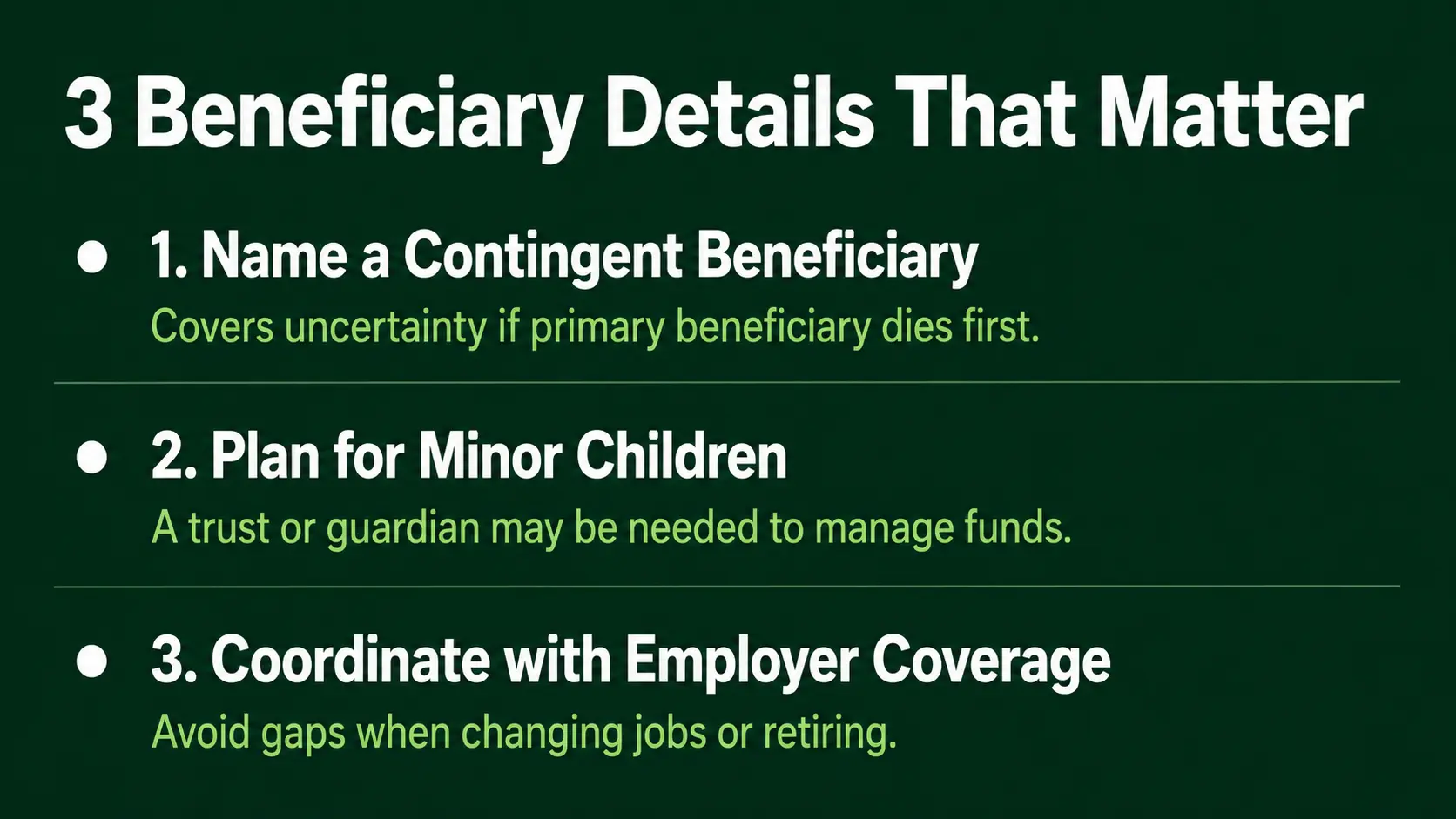

Small administrative choices can have big outcomes. Updating beneficiaries, naming contingent beneficiaries and coordinating with other accounts can strengthen the policy’s reliability.

- Primary and contingent beneficiaries help prevent uncertainty if a beneficiary dies first.

- Minor children planning may require a guardian or trust structure to manage funds responsibly.

- Coordination with employer coverage avoids gaps when changing jobs or retiring.

These details keep the policy aligned with your intent and reduce the risk of surprises when claims are filed.

What Life Insurance is Not Meant To Do?

Life insurance is not a substitute for emergency savings, disability insurance, or a well-built budget. It also should not be purchased solely on the hope that cash value will outperform other long-term strategies.

The purpose is protection first. Any secondary features should be evaluated in the context of costs, guarantees and the specific planning need you are trying to meet.

Conclusion

The purpose of life insurance is to protect the people and plans that would be financially exposed by a death. It creates immediate liquidity, supports income replacement, helps manage debts and final expenses and can strengthen estate and business planning.

When coverage is matched to a clear goal, life insurance becomes a practical tool rather than a confusing product. The best policy is the one that fits your purpose, your timeline and your budget while staying easy for beneficiaries to use.