Life insurance is designed to replace lost income and cover financial obligations after a death. Still, many people buy a policy without fully understanding what life insurance covers and not cover, especially when exclusions and timing rules apply. Knowing the boundaries helps you choose the right type, disclose information correctly and avoid denied claims.

How Life Insurance Coverage Works?

Life insurance pays a death benefit to a named beneficiary when the insured person dies and the policy is in force. The benefit amount is set by the contract and payments depend on premiums being paid on time.

Coverage is not a blanket promise for every situation. Each policy has definitions, exclusions and conditions that determine whether the insurer must pay.

What Life Insurance Typically Covers?

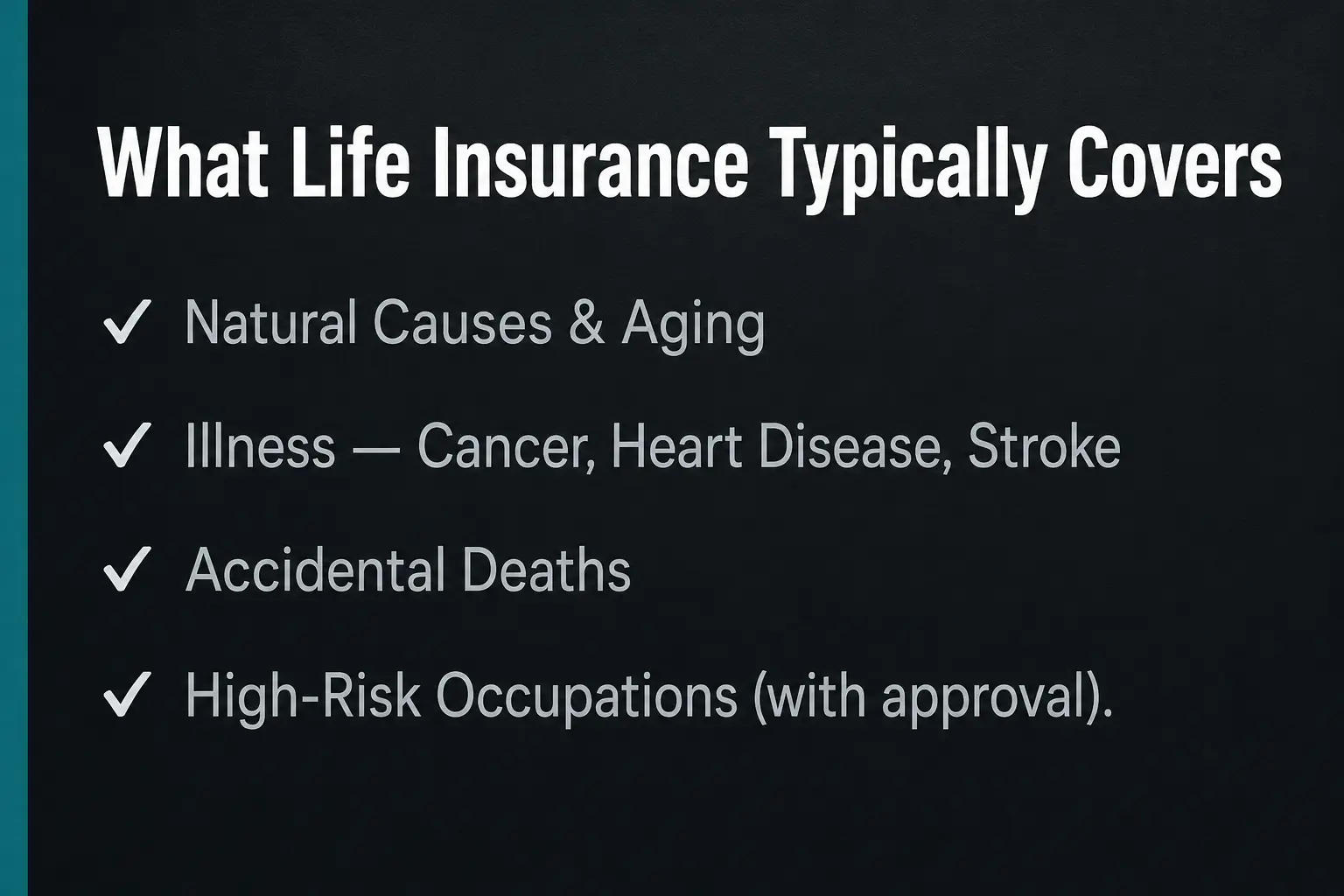

Most policies cover death from natural causes, illnesses and accidents, as long as the policy is active and the application was truthful. Term life and permanent life both generally pay when a covered death occurs within the policy rules.

Coverage focuses on the event of death, not the cause, unless the contract specifically limits certain causes. The details vary by insurer and by policy form.

- Natural causes: Death related to aging or underlying health conditions is usually covered after underwriting and the contestability window.

- Illness: Many cancers, heart disease, stroke and other medical causes are covered if disclosed accurately during application.

- Accidents: Accidental deaths are commonly covered and some policies add extra benefits through accidental death riders.

- Occupational and lifestyle risks: High-risk jobs or activities can be covered, but may require higher premiums, ratings, or specific approvals.

Once you understand these common covered categories, it becomes easier to evaluate exclusions that limit payment.

What Life Insurance Usually Does Not Cover?

Life insurance exclusions are policy clauses that remove coverage for specific circumstances. Some exclusions are standard across many insurers, while others are optional or depend on underwriting.

These limits are not hidden, but they are often overlooked. Reviewing them before buying matters more than any marketing promise.

- Fraud and material misrepresentation: Incorrect or withheld information that would have changed the underwriting decision can trigger denial or rescission.

- Nonpayment and lapse: If premiums are not paid and grace periods end, coverage can terminate and no death benefit is owed.

- Excluded causes in the contract: Some policies include specific exclusions tied to war, aviation, hazardous activities, or other risks.

- Death outside defined covered status: If a policy requires active employment for group coverage or other eligibility rules, failing those rules can affect benefits.

These exclusions connect directly to two core concepts that often decide claims, contestability and suicide limitations.

Contestability Period and Application Accuracy

Many individual life policies include a contestability period that allows the insurer to review the application more aggressively after death. If the death occurs during that window, the insurer may investigate medical history, prescriptions and records for inconsistencies.

Honest disclosure is essential because the issue is not only intent. Even unintentional errors can be considered material if they would have changed the premium or approval.

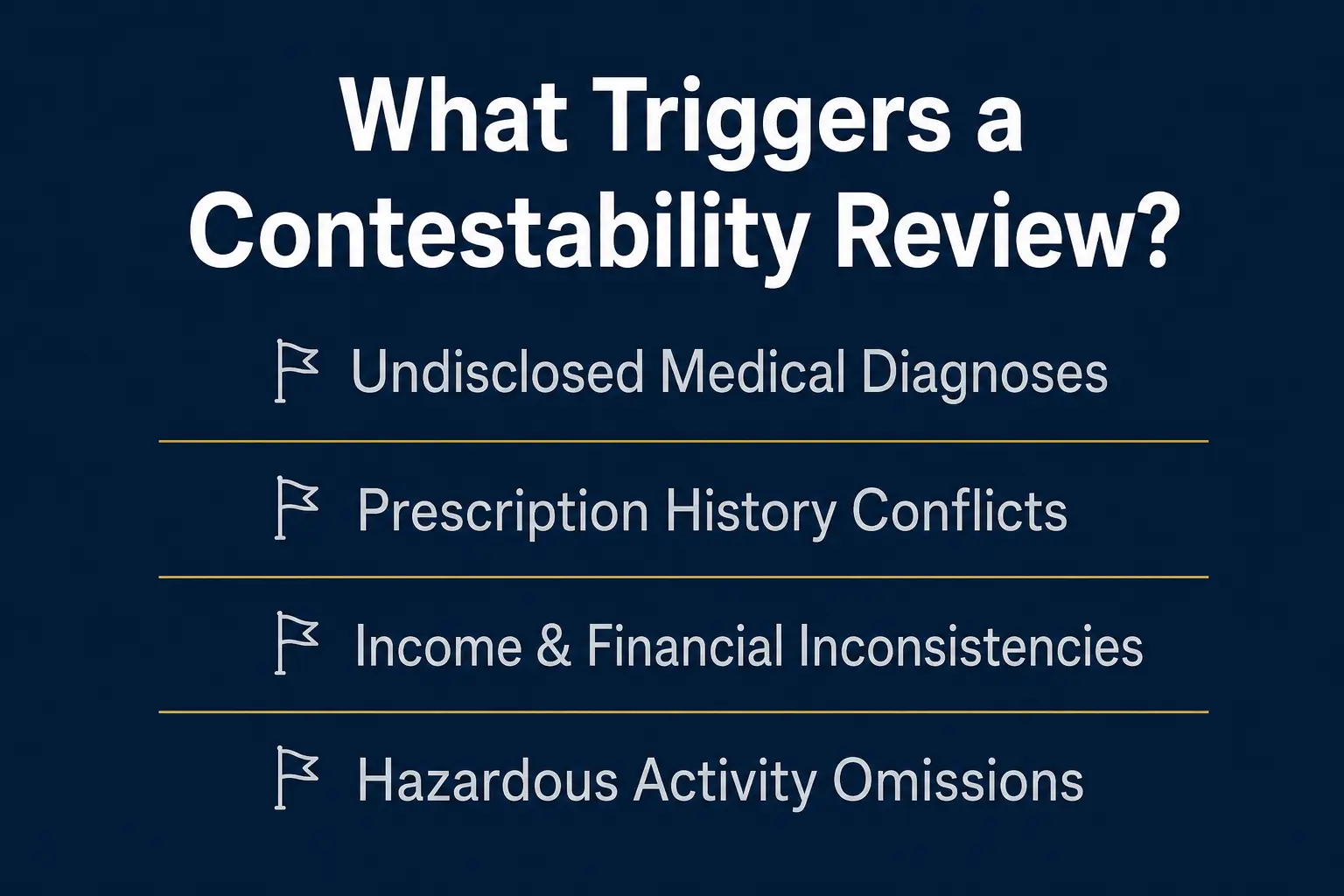

What Commonly Triggers a Contestability Review?

Insurers generally investigate when timing, medical records, or application responses do not align. The goal is to confirm the contract was issued based on accurate risk information.

- Undisclosed diagnoses: Missing a significant condition can be treated as material even if it seems unrelated to the cause of death.

- Prescription history conflicts: Medication records can contradict reported health status or tobacco use.

- Income and financial inconsistencies: Large policies may require financial justification and inaccurate figures can raise issues.

- Hazardous activity omissions: High-risk hobbies and job duties are often specifically asked during underwriting.

Clear, complete answers reduce claim delays and lower the chance of a denial based on the application.

Suicide Clause and Self Inflicted Death

Many policies include a suicide limitation period, after which suicide is typically covered. During the limitation period, the insurer may return premiums paid rather than paying the full death benefit.

Definitions vary, including how the policy treats mental health conditions, intoxication and intent. Reading the contract language matters, especially when a policy is newly issued.

Accidental Death Benefit and AD and D Limits

Accidental death benefit riders or standalone AD and D coverage can pay an additional amount when death is caused by a covered accident. These benefits often have narrower definitions than people expect.

Accidents must usually be sudden, external and independent of illness. Events involving risky behavior, certain exclusions, or contributing medical conditions may not qualify for the extra benefit even if base life insurance still pays.

Common Exclusions You Should Check in The Policy

Exclusions are highly specific, so a quick skim is not enough. A few pages in the policy contract can change whether an event is covered.

Ask for the specimen policy or the actual contract wording, then confirm any exclusions listed in your issued policy schedule.

- War and military service exclusions: Some contracts limit benefits for deaths related to war, declared or undeclared, or certain deployments.

- Aviation exclusions: Coverage may be limited for noncommercial flights, private piloting, or certain aircraft use.

- Hazardous sports exclusions: Activities such as skydiving or technical climbing may be excluded or require extra underwriting approval.

- Illegal acts exclusions: Death during certain illegal activities may be excluded depending on policy language and jurisdiction.

After you identify exclusions, you can decide whether a rider, different insurer, or different policy type is a better fit.

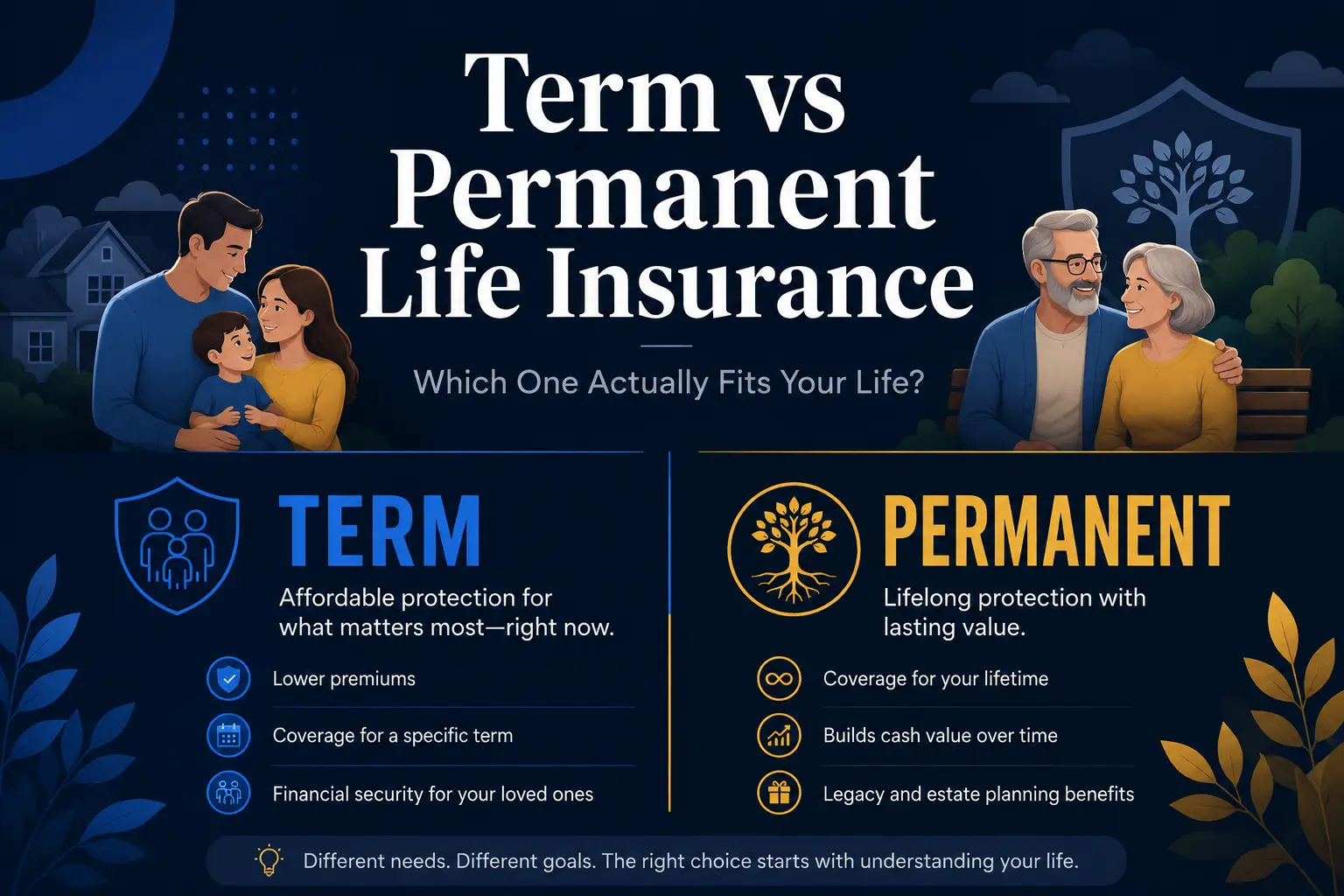

Term Life Versus Whole Life Coverage Differences

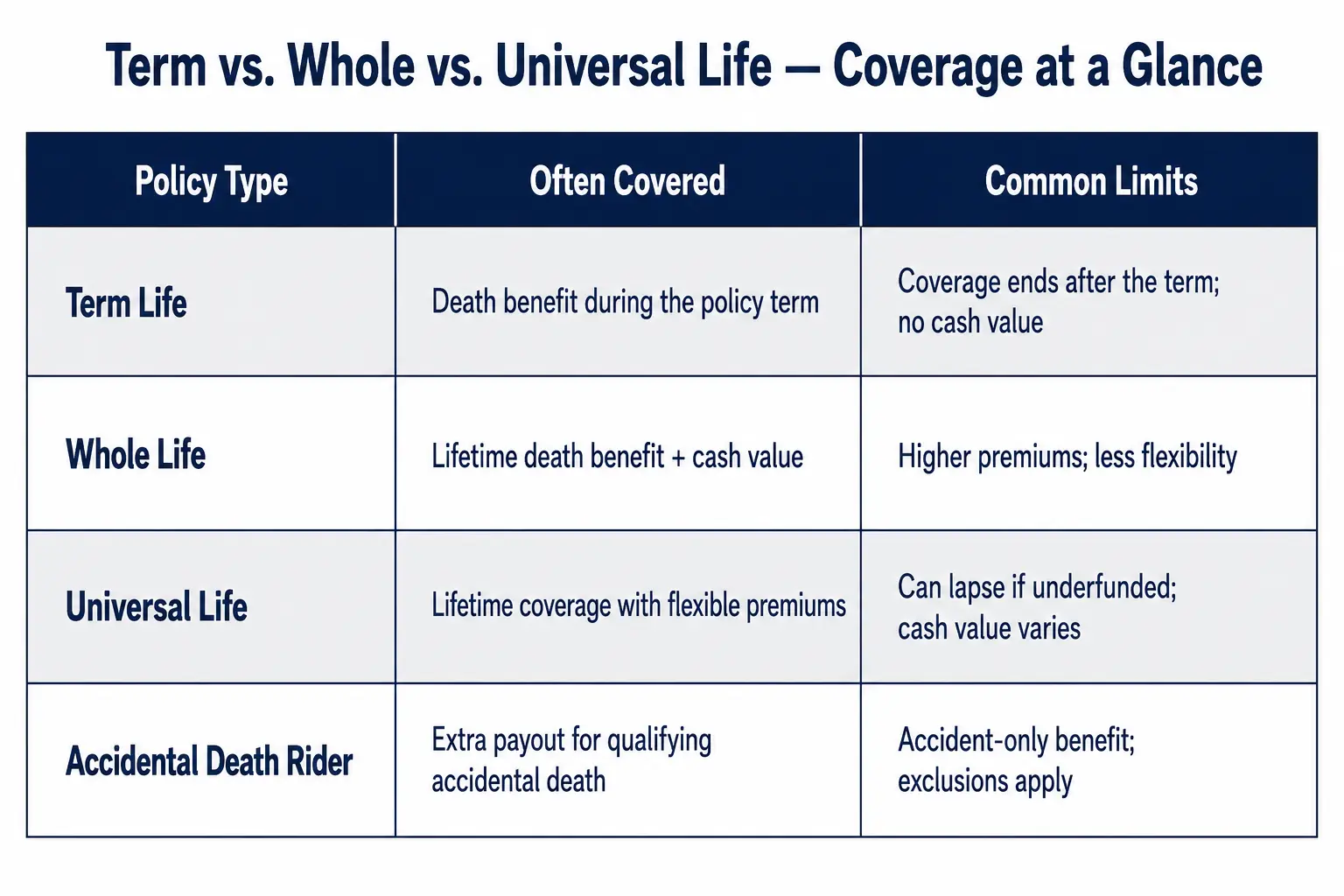

Term life covers death during a set period, such as 10, 20, or 30 years, as long as premiums are paid. Whole life and other permanent policies are designed to last longer and may build cash value, but they still have exclusions and conditions.

The biggest practical difference is duration, not whether death is covered. Term coverage can expire with no payout, while permanent coverage can remain in force if funded properly.

| Policy Feature | Often Covered | Common Limits or Not Covered |

|---|---|---|

| Term Life | Death from illness or accident during the term | No payout after term ends unless converted or renewed |

| Whole Life | Death benefit for life when premiums are kept current | Policy can lapse if loans and premiums are mismanaged |

| Universal Life | Flexible premiums with ongoing death benefit potential | Coverage can end if cash value cannot support charges |

| Accidental Death Rider | Extra benefit for qualifying accidental death | Narrow definitions, exclusions and age limits may apply |

This comparison helps clarify that many coverage gaps come from timing, funding and definitions rather than from the general idea of life insurance.

Group Life Insurance and Employer Plans

Group life insurance through an employer can be a valuable baseline, but it may be limited in amount and portability. Coverage often ends when employment ends unless a conversion option is used.

Eligibility requirements, enrollment deadlines and evidence of insurability rules can affect what is covered. Some plans also include different definitions for accidental death benefits.

Riders That Can Expand What is Covered

Riders modify a policy and can broaden benefits, but they also add cost and specific rules. Riders are not automatically included, so they must be elected and approved.

Reading each rider is just as important as reading the base policy. A rider can have its own exclusions and waiting periods.

- Waiver of premium: Keeps coverage in force if disability meets the rider definition and requirements.

- Accelerated death benefit: Allows early access to part of the death benefit under qualifying terminal illness rules.

- Child term rider: Adds limited coverage for eligible children, usually with age and conversion limits.

- Guaranteed insurability: Offers future purchase options without new medical underwriting under specific conditions.

Choosing riders is most effective when it matches real risks and budget, not when it tries to cover every possible concern.

How to Reduce The Risk of a Denied Claim?

Claim denials often trace back to preventable issues such as missed payments, incomplete disclosures, or outdated beneficiary details. A simple review routine can remove most of the uncertainty.

Focus on accuracy, documentation and keeping the policy in force. That approach aligns the contract with the reason you bought coverage.

- Answer underwriting questions completely. Provide full medical, tobacco and lifestyle information so the policy is issued on accurate risk.

- Pay premiums reliably. Use autopay where possible and confirm grace period rules to avoid an unintended lapse.

- Update beneficiaries after major life changes. Marriage, divorce, births and deaths can make an old beneficiary designation unworkable.

- Store policy documents securely. Keep the contract, contact details and payment history accessible to beneficiaries.

- Review exclusions and riders annually. Confirm that current work, travel and hobbies still fit the policy terms.

These habits also make the claims process faster because beneficiaries can submit clean paperwork with fewer follow-up requests.

Conclusion

Understanding what life insurance covers and not cover comes down to reading the contract and respecting its conditions. Most policies cover death from illness and accidents when premiums are current and the application is accurate.

Exclusions, contestability rules, suicide limitations and lapses are the most common reasons benefits are reduced or denied. A careful policy review, smart rider choices and consistent maintenance help ensure the death benefit is there when it is needed.