Yes, you can have multiple life insurance policies at the same time. Many people build coverage in layers to match changing needs, budgets and goals.

Having more than one policy can be a practical way to protect a family, cover a mortgage, or support a business plan without relying on a single contract.

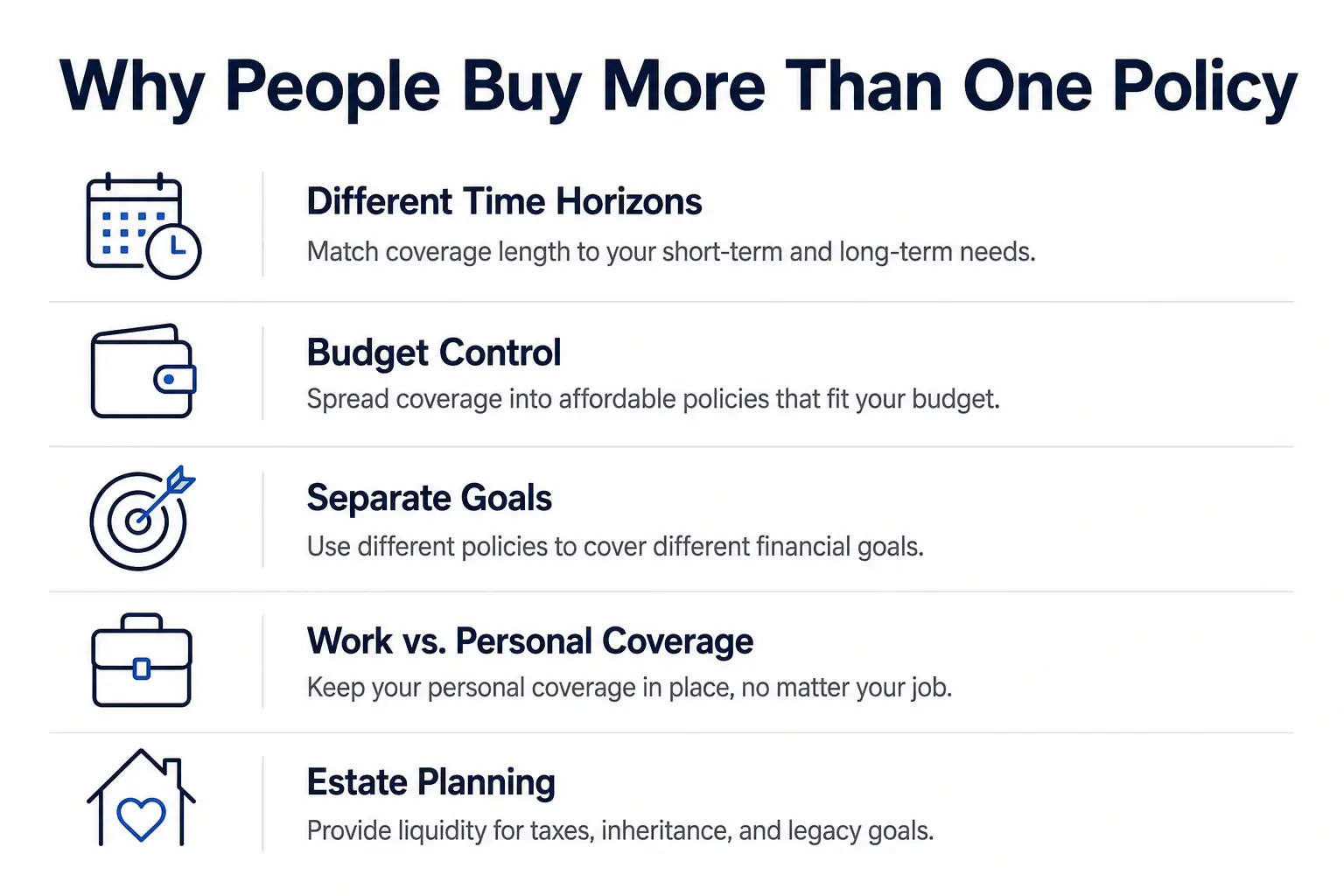

Why People Buy More Than One Policy?

Life insurance needs rarely stay the same for decades. Income rises, debts change, children become adults and retirement timelines shift.

Multiple policies can help you adjust coverage without replacing everything at once. This can reduce the risk of being underinsured during major transitions.

- Different time horizons: Shorter term coverage can protect a mortgage, while long term coverage can support a spouse for longer.

- Budget control: Adding a smaller policy can be cheaper than increasing a larger one, depending on age and health.

- Separate goals: One policy can focus on income replacement, while another targets final expenses or a specific debt.

- Work benefits and personal coverage: Employer provided life insurance may not be enough or may not be portable.

- Estate and legacy planning: Some households use permanent coverage for predictable lifetime protection.

Once you know why you want coverage, the next step is understanding how insurers evaluate overlapping policies.

Is it Legal and Allowed by Insurers

Owning multiple life insurance policies is legal. Insurers generally allow it as long as the total coverage is reasonable for your financial profile.

Carriers look for insurable interest at the time of purchase and for appropriate coverage relative to income, debts and existing insurance.

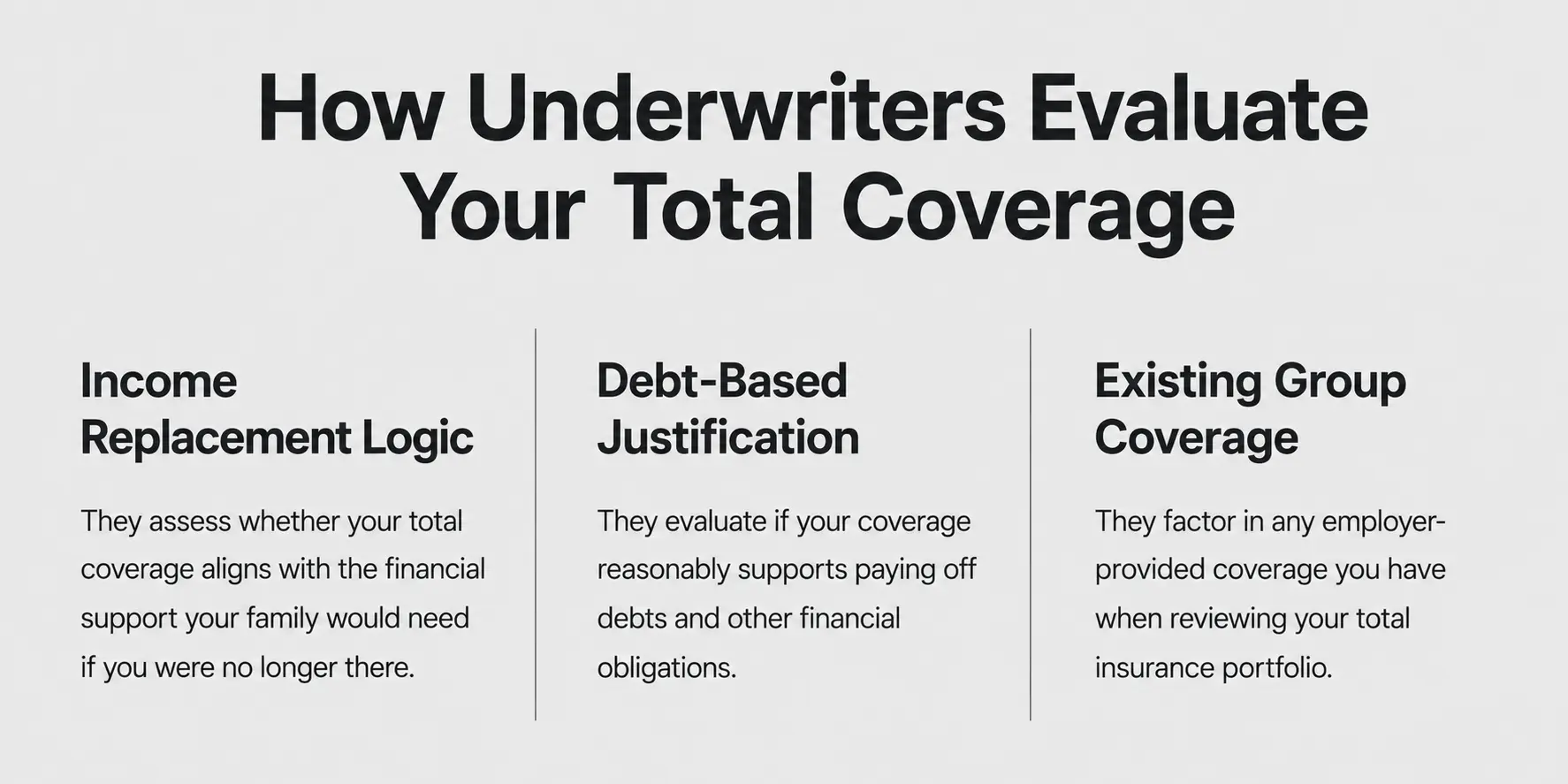

How Underwriting Looks at Total Coverage?

When you apply for a new policy, you usually must disclose existing life insurance. The insurer adds up your in force coverage, pending applications and the amount you request.

Underwriters often review income, net worth, liabilities and purpose of insurance. If the total looks excessive, they can reduce the offer, request more documentation, or decline.

- Income replacement logic: Coverage commonly aligns with earning power and dependents, not just what you want to buy.

- Debt based justification: Mortgages, personal loans and business obligations can support higher totals.

- Existing group coverage: Workplace policies count, even if you did not actively shop for them.

This review helps insurers manage risk and helps you avoid paying for coverage that does not match a clear need.

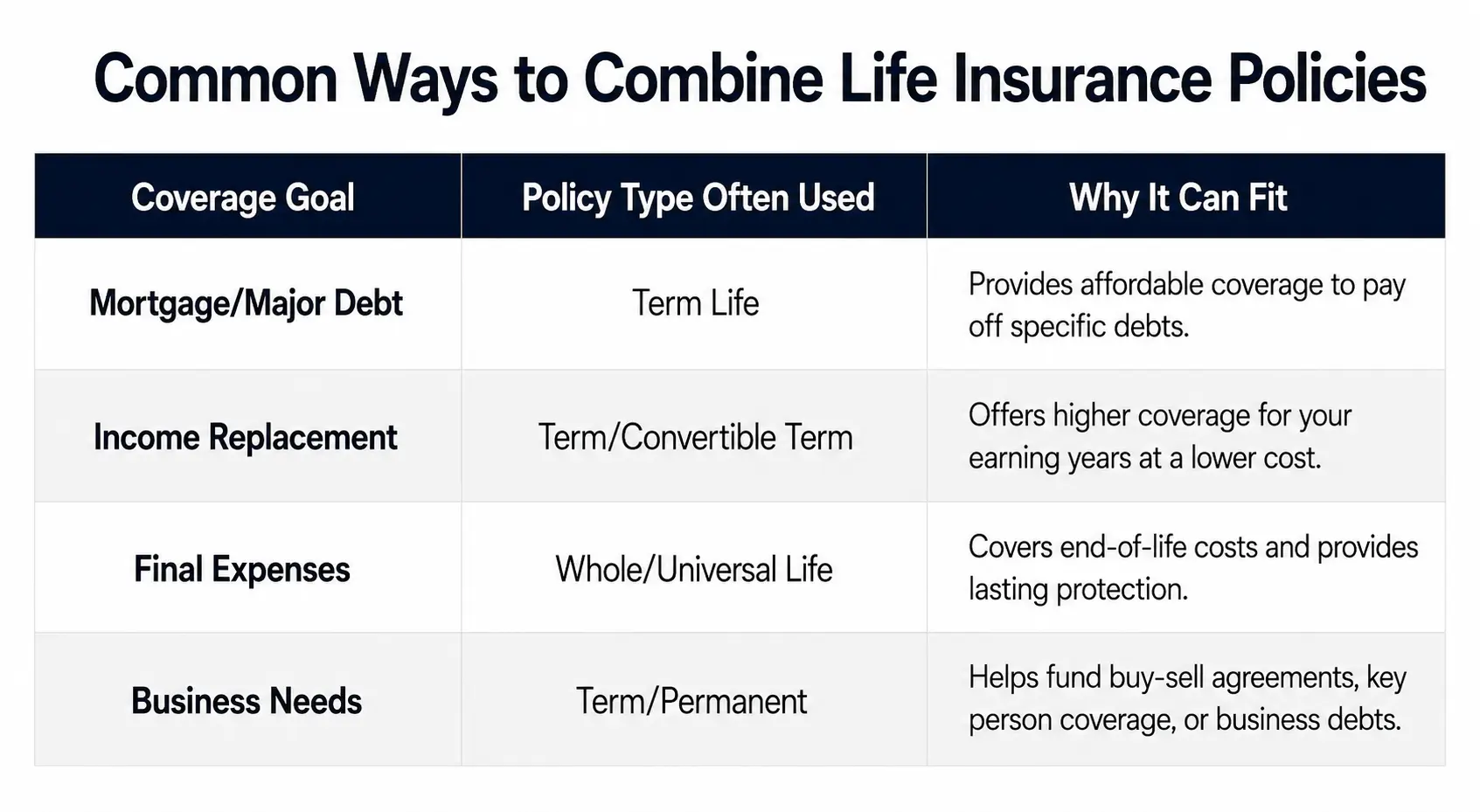

Common Ways to Combine Policies

Layering policies can be simple when each one has a clear job. People often pair a larger term policy with a smaller permanent policy, but there are many combinations.

The key is to align each policy term, death benefit and premium with a specific obligation or goal.

| Coverage Goal | Policy Type Often Used | Why It Can Fit |

|---|---|---|

| Mortgage or Major Debt | Term Life | Matches a fixed time period and can keep premiums lower |

| Income Replacement For Dependents | Term Life or Convertible Term | Provides high coverage during peak earning and child raising years |

| Final Expenses and Lifelong Coverage | Whole Life or Universal Life | Designed to stay in force for life if premiums are paid as required |

| Business Continuity and Key Person Needs | Term Life or Permanent Life | Can support buy sell plans or protect revenue tied to a key employee |

This mix helps clarify what each policy is protecting and reduces overlap that adds cost without adding value.

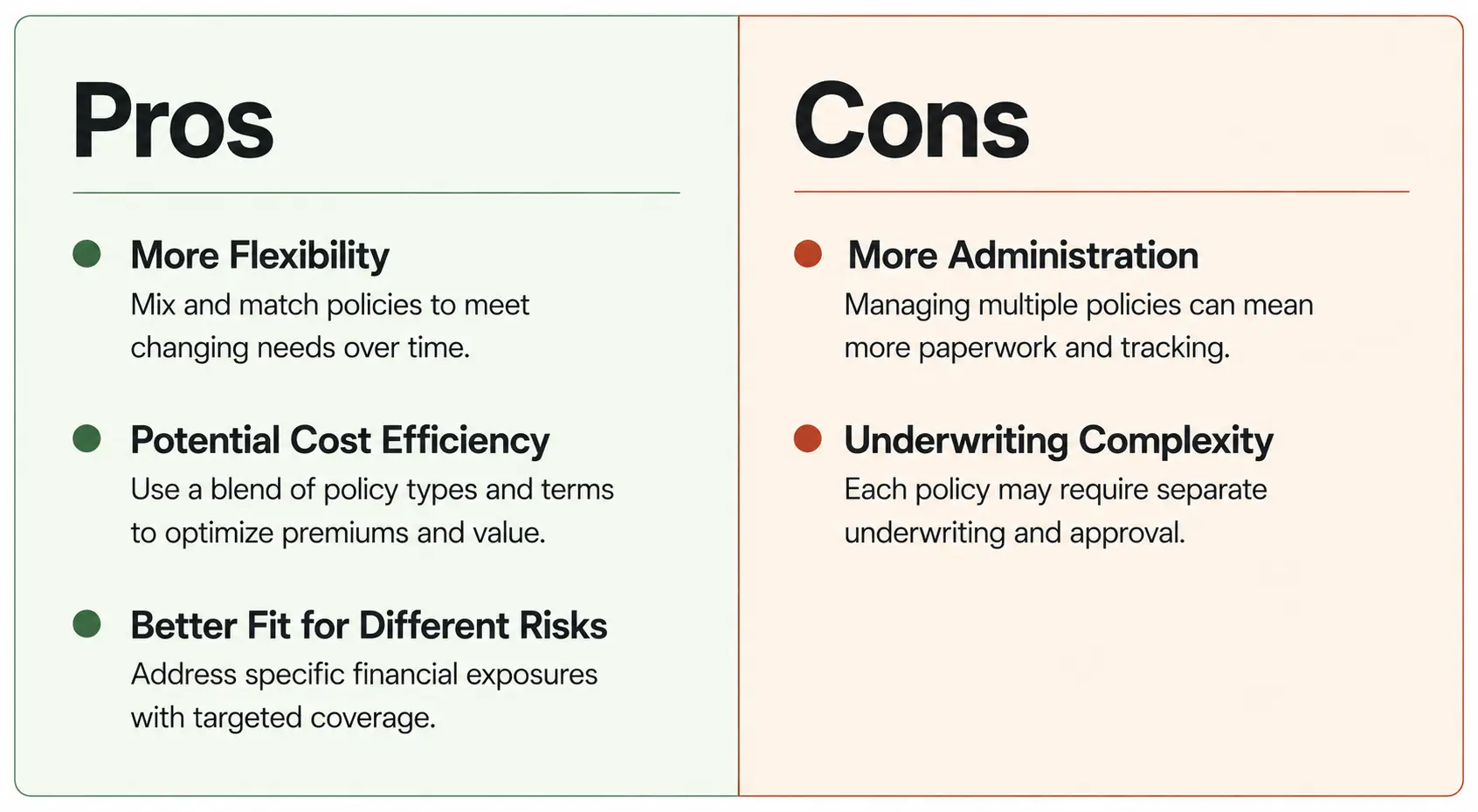

Pros and Cons Of Multiple Policies

Multiple policies can give flexibility, but they also add moving parts. A clear tracking system matters so coverage stays aligned with your plan.

Reviewing policies together can also prevent paying for duplicate riders or unnecessary add ons.

- More flexibility: You can add or drop a layer later without rewriting everything.

- Potential cost efficiency: A blend of term lengths can reduce premiums compared to one large long term policy.

- Better fit for different risks: Personal, family and business needs do not always share the same timeline.

- More administration: Multiple premiums, beneficiaries and policy numbers increase the chance of missed updates.

- Underwriting complexity: New applications require disclosure and justification of total coverage.

Understanding the tradeoffs makes it easier to decide whether layering improves your protection or just adds clutter.

How Beneficiaries and Payouts Work?

Each life insurance policy pays its own death benefit to the named beneficiaries, assuming the claim is valid. Payouts can arrive at different times if policies are with different carriers.

You can name the same beneficiary on every policy or split beneficiaries across policies. Keeping beneficiary designations current is critical after marriage, divorce, or the birth of a child.

When Multiple Policies Can Cause Problems?

Problems usually come from poor coordination, not from the fact that there are multiple contracts. The biggest risk is buying coverage without a clear purpose and later struggling to keep premiums affordable.

Another issue is inconsistent information across applications. Differences in medical history answers, tobacco use, or existing coverage disclosures can delay underwriting or lead to disputes.

- Premium strain: If income drops, maintaining several policies can be harder than maintaining one.

- Coverage gaps: Letting one policy lapse while assuming another is active can leave a household exposed.

- Beneficiary errors: Outdated names, missing contingent beneficiaries, or mismatched ownership can slow settlement.

A coordinated review keeps the full stack of coverage working as intended.

How to Decide The Right Total Amount of Coverage

Total coverage should reflect real obligations and the people who depend on you financially. A practical approach is to calculate needs in categories and then decide which policy layer covers each category.

Many households focus on income replacement, debt payoff, education funding and end of life costs. Business owners may add buy sell needs, key person exposure and loan guarantees.

- Income needs: Consider how many years a spouse or children would rely on your earnings.

- Debt and ongoing bills: Include mortgage balance, loans and recurring costs that would continue.

- Future goals: Education and caregiving plans can shape how long coverage is needed.

- Existing assets: Savings, retirement accounts and other resources can reduce the insurance gap.

Once the total is clear, you can decide whether a single policy or multiple life insurance policies best match the timeline of those needs.

Tips for Managing Multiple Policies Over Time

Good management keeps layering from turning into confusion. The goal is to make it easy for you and for beneficiaries to find policies, confirm coverage and file claims.

Regular reviews also help you adjust coverage as debts shrink and dependents become less reliant on your income.

- Document policy details. Keep carrier names, policy numbers and premium due dates in one secure place.

- Align ownership and beneficiaries. Confirm the owner, primary beneficiary and contingent beneficiary on every policy.

- Coordinate coverage terms. Match each term length to the obligation it is meant to cover.

- Review riders and duplication. Check for overlapping riders like waiver of premium or accidental death benefits.

- Schedule periodic checkups. Revisit coverage after major life changes and any large increase or decrease in income.

These habits reduce the chance of lapses and make claims far easier for survivors to handle.

Conclusion

You can have multiple life insurance policies and in many cases it is a smart way to build coverage that matches real life changes. The best results come from assigning each policy a clear purpose and keeping the total coverage reasonable for your financial situation.

Focus on coordination, accurate disclosures and consistent beneficiary updates. When managed well, multiple policies can provide stronger protection without unnecessary cost or confusion.