Whole life insurance is a type of permanent life insurance designed to last for your entire life as long as premiums are paid. It combines a death benefit for beneficiaries with a cash value component that can grow over time.

People often consider it when they want lifelong coverage, predictable premiums and a policy that builds value inside the contract. Understanding how the coverage, costs and cash value mechanics work makes it easier to decide if it fits your goals.

What is Whole Life Insurance and How Does It Work?

Whole life insurance is a contract between you and an insurer that provides a guaranteed death benefit and level premiums, with cash value that typically grows on a set schedule. In many policies, the insurer credits interest or a fixed rate to the cash value according to the policy terms.

The key idea is that a portion of each premium pays for insurance costs and fees, while another portion helps build cash value. Over time, the cash value can become a meaningful feature of the policy, though growth is usually slower in the early years.

Whole Life Insurance Basics

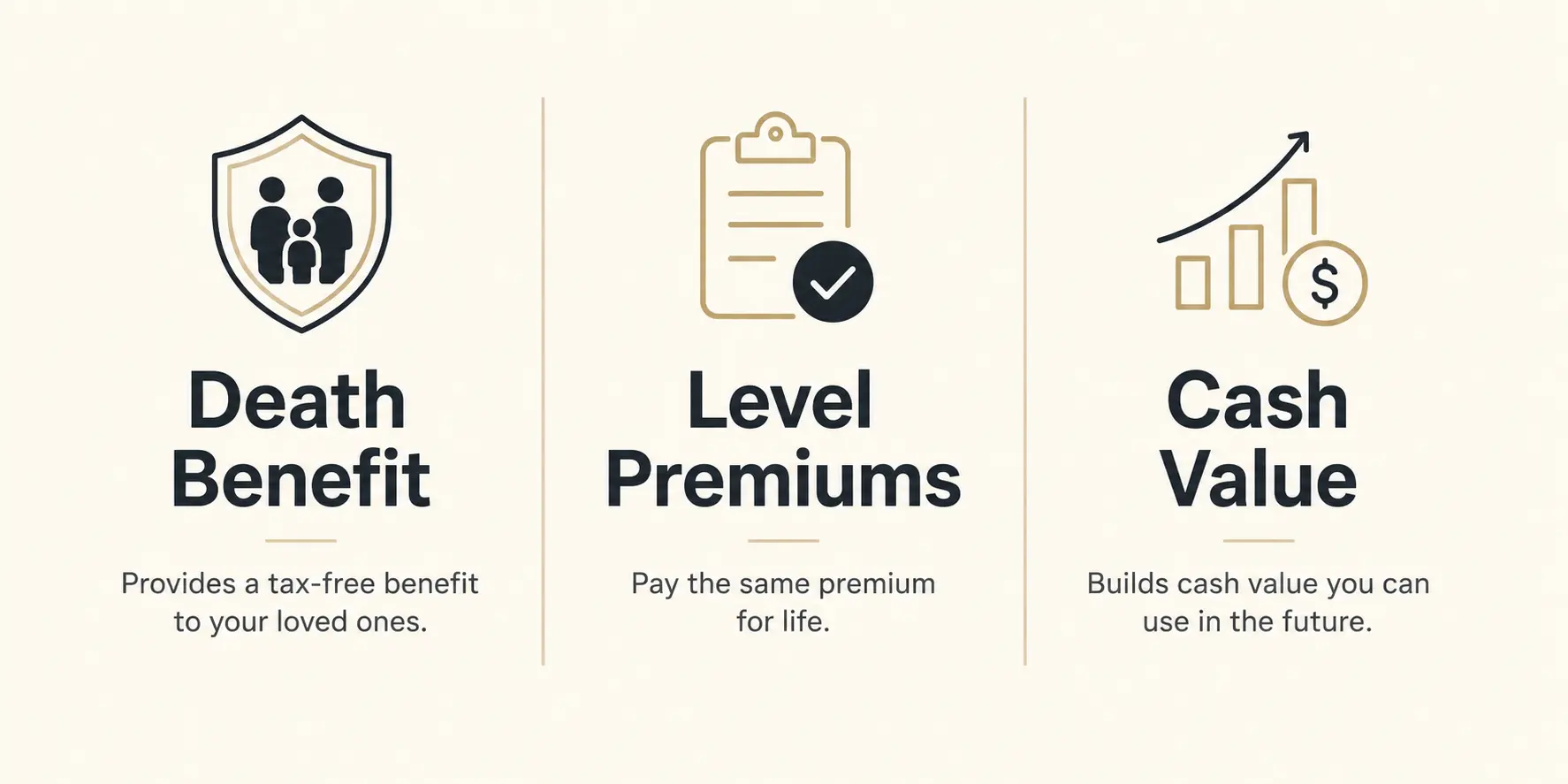

A whole life policy is built around three core parts, the death benefit, the premium and the cash value. The death benefit is the amount paid to beneficiaries when the insured person dies, assuming the policy is in force.

Premiums are typically level, meaning they are intended to stay the same for the life of the policy. Cash value is the internal account value that can increase over time based on the policy guarantees and crediting method.

- Death benefit: Money paid to beneficiaries, usually income tax free under current rules in many cases.

- Level premiums: Designed to be predictable, which can help with long-term budgeting.

- Cash value: Value that grows inside the policy and may be accessed through loans or withdrawals, depending on the contract.

Those pieces work together, but the details vary by insurer, underwriting class, riders and how the policy is funded.

How Premiums are Structured?

Whole life premiums are priced to cover lifelong protection, not just a short period. Early premiums are generally higher than term life premiums for the same death benefit because the policy is designed to stay in force permanently.

Premiums also reflect factors such as age, health, tobacco use and the insurer’s underwriting guidelines. Some policies offer payment periods such as paid-up at a certain age or limited pay options, which can change the premium amount.

- Base premium: Funds the core coverage and guaranteed cash value schedule.

- Rider cost: Optional add-ons can raise the premium but may add flexibility or protection.

- Underwriting impact: Better health classes often receive lower rates for the same coverage.

Before committing, it helps to confirm whether premiums are fully guaranteed and what could trigger changes, such as adding riders or changing payment structure.

Cash Value Growth and Guarantees

Cash value typically grows according to a guaranteed schedule shown in the policy illustration, although actual results depend on the specific type of whole life and the insurer’s performance. Some whole life policies offer guarantees for minimum cash value and minimum death benefit, assuming premiums are paid as required.

In participating whole life, the policy may also be eligible for dividends, which are not guaranteed. When paid, dividends can be taken in cash, used to reduce premiums, left to accumulate interest, or used to purchase paid-up additions that may increase cash value and death benefit.

Cash value growth is usually constrained early on due to policy charges and front-loaded costs. This makes whole life generally more suitable for long-term horizons rather than short-term savings needs.

Policy Loans and Withdrawals

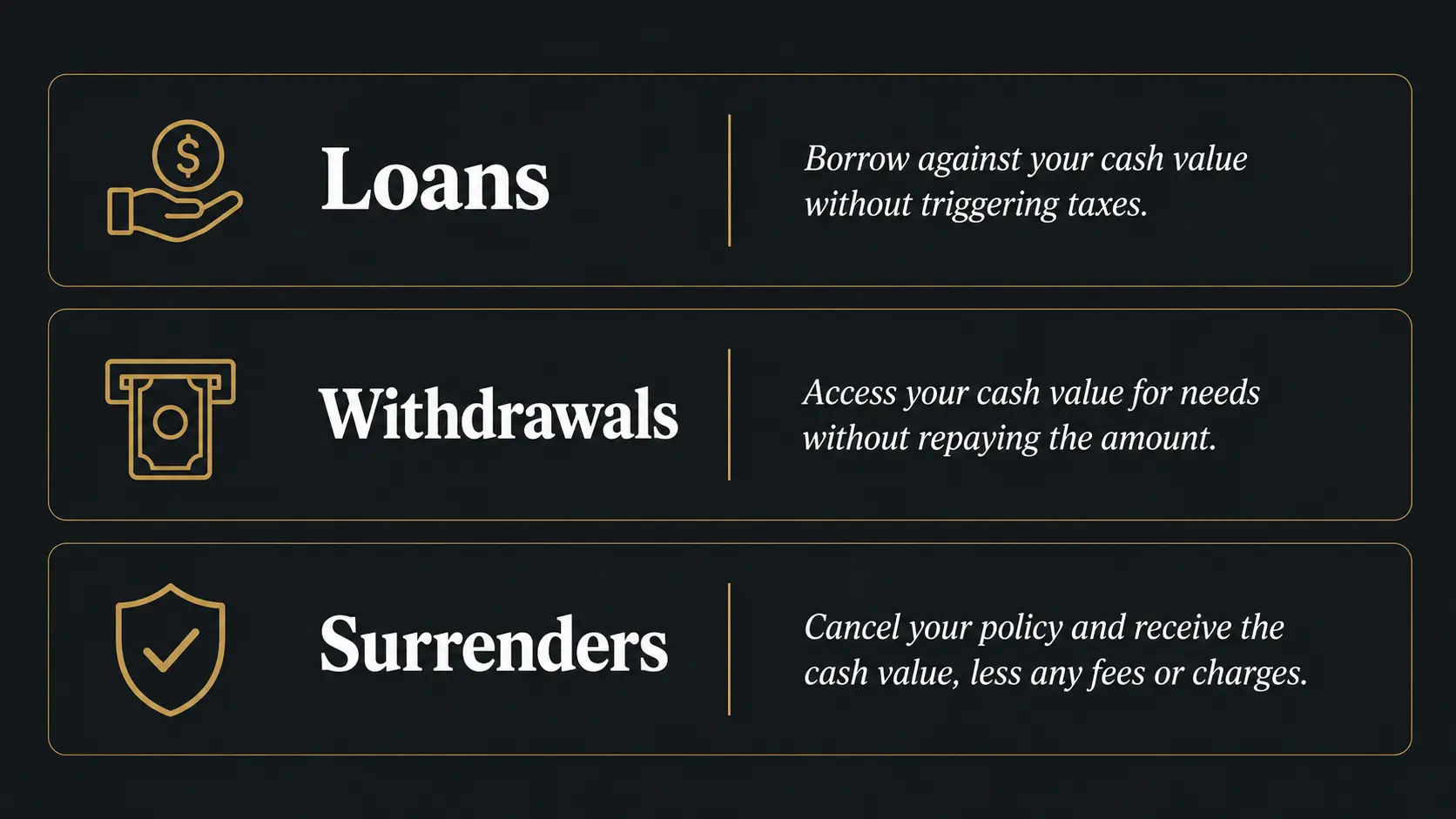

Access to cash value is often described as a feature, but it comes with rules and tradeoffs. Policy loans allow you to borrow against the cash value and the policy itself typically serves as collateral.

Loans usually charge interest and reduce the net death benefit while outstanding. If loans and interest grow too large, the policy can lapse, which can create serious financial and tax consequences.

- Loans: Keep the policy in force if managed carefully, but interest accrues and reduces the payout if not repaid.

- Withdrawals: May reduce cash value and death benefit and can trigger taxes depending on the policy basis and rules.

- Surrenders: Cancelling the policy provides the cash surrender value minus any fees or loan balances.

Careful tracking of loan balances, interest and ongoing premium requirements is essential when using a policy for liquidity.

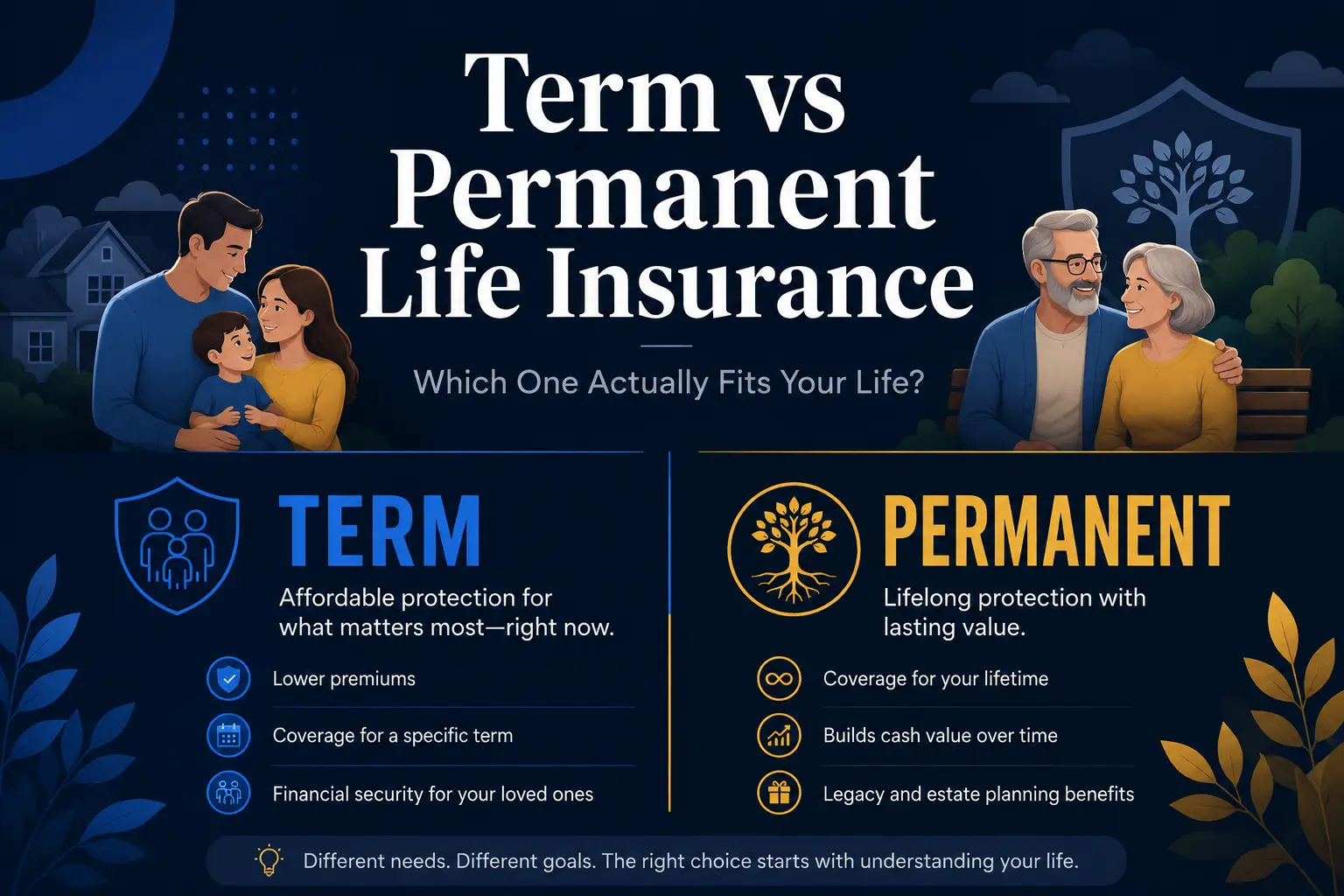

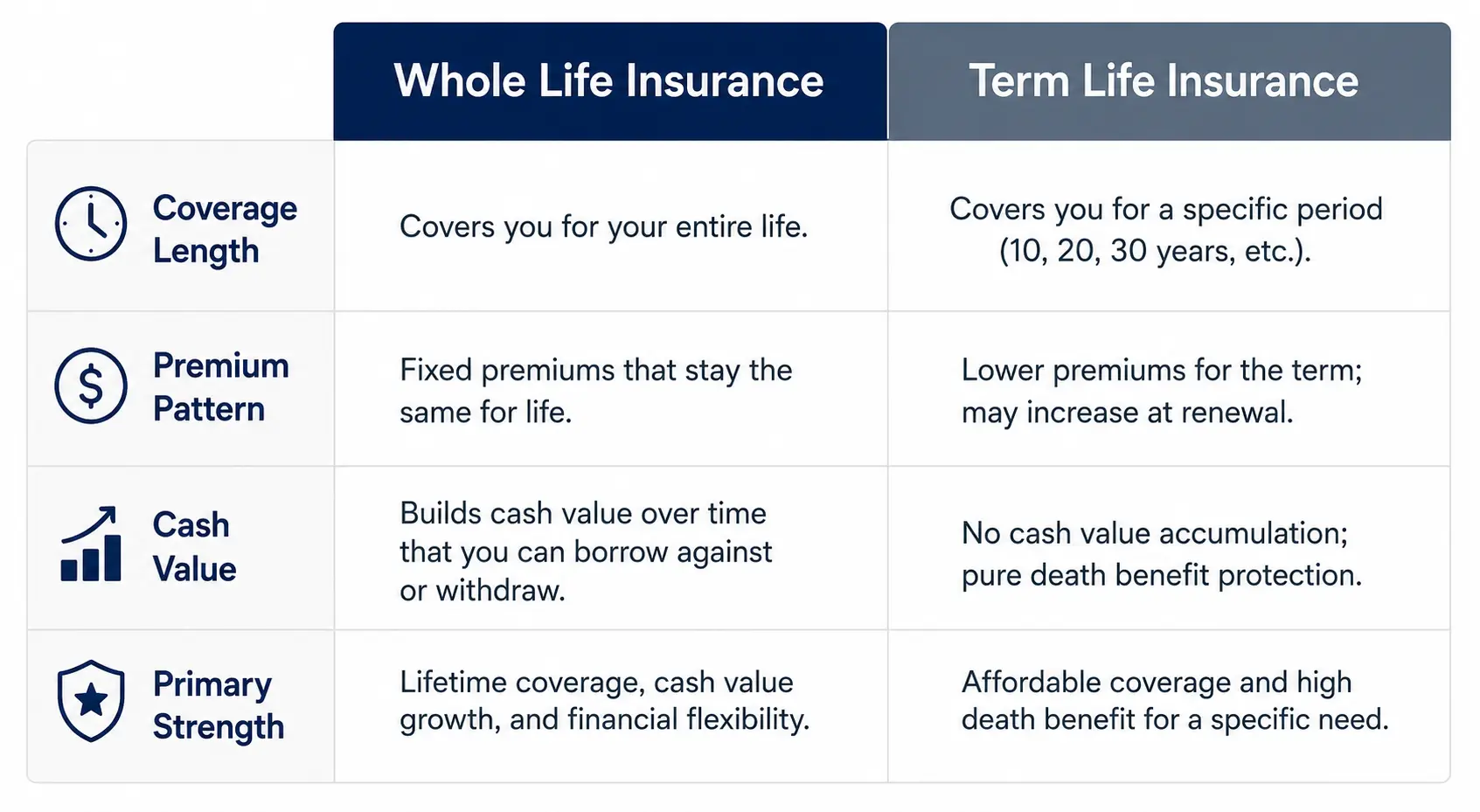

Whole Life Insurance Vs Term Life Insurance

Term life insurance is designed for a set period and generally offers the lowest cost for a given death benefit. Whole life is designed for lifelong coverage and includes cash value, so it usually costs more but offers guarantees and permanence.

The right choice depends on your time horizon, need for permanent protection, tolerance for higher premiums and whether you value the cash value feature. Comparing policies side by side helps clarify the tradeoffs.

| Feature | Whole Life Insurance | Term Life Insurance |

|---|---|---|

| Coverage Length | Lifetime with required premiums | Fixed term length |

| Premium Pattern | Typically level and higher | Typically level then ends or renews higher |

| Cash Value | Builds cash value over time | No cash value |

| Primary Strength | Permanent protection and guarantees | High death benefit per dollar of premium |

This comparison highlights the big differences, but the fine print matters, especially around renewability, conversion options and policy fees.

Riders and Options That Change How it Works?

Riders are optional features that modify coverage, costs, or flexibility. They can add value when aligned with a specific need, but they also increase complexity and may raise the premium.

Common rider themes include adding more coverage, protecting the policy if you become disabled, or accelerating access to benefits. Rider availability varies by insurer, state and underwriting results.

- Waiver of premium: The insurer may pay premiums if you meet the disability definition in the rider.

- Accelerated death benefit: May allow early access to part of the death benefit for qualifying serious illness.

- Paid-up additions: May increase cash value and death benefit, often tied to dividend options in participating policies.

Review each rider’s eligibility, cost and triggers, since these details determine whether the rider delivers meaningful protection.

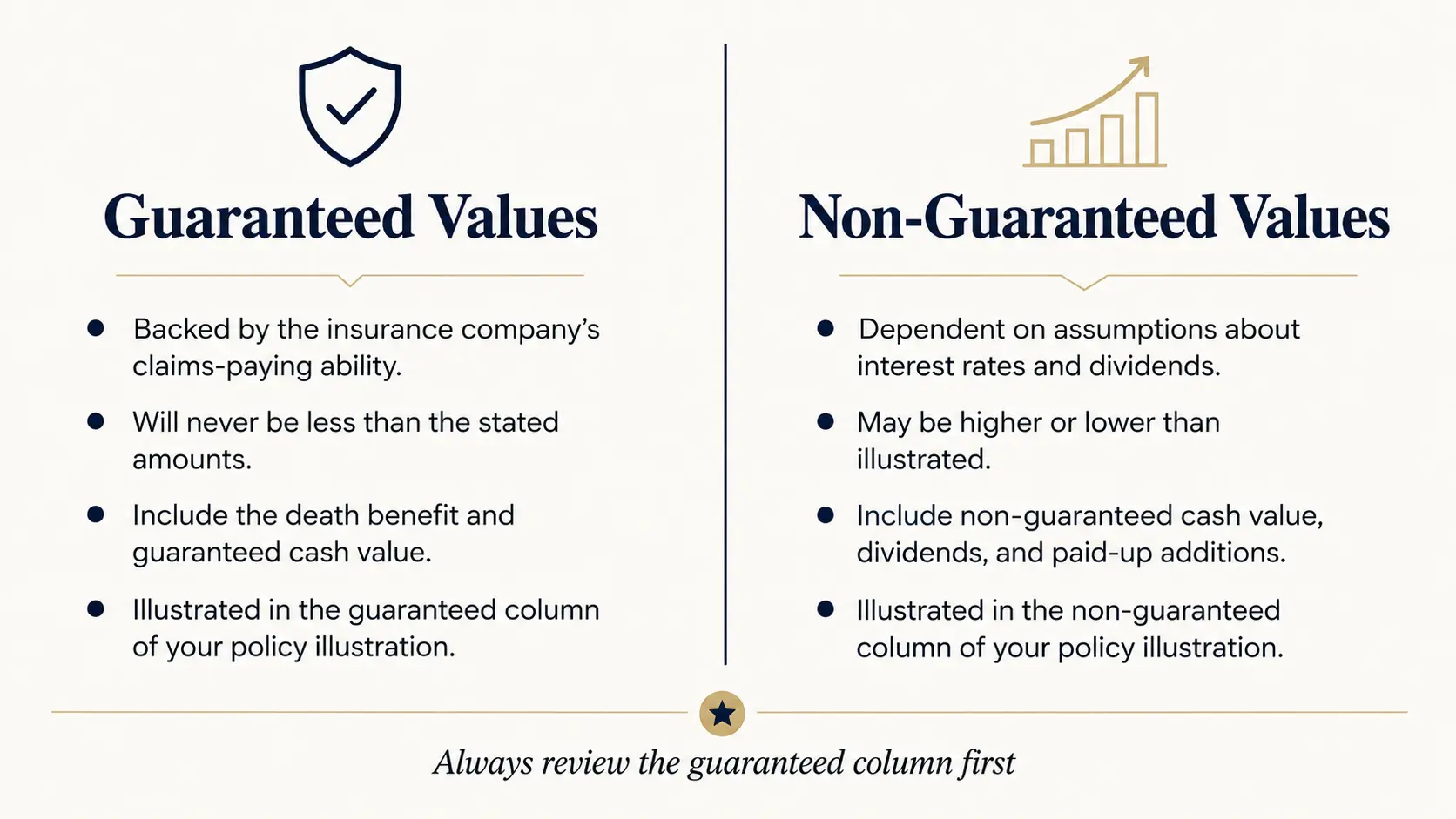

What a Policy Illustration Can and Cannot Tell You?

A policy illustration summarizes projected values over time, such as premiums, guaranteed cash value, non-guaranteed values and projected death benefit. It can be helpful for comparisons, but it is not a promise of future performance beyond the guaranteed elements.

Look closely at guaranteed versus non-guaranteed columns, dividend assumptions and how long it takes for cash value to exceed total premiums paid. It also helps to confirm how dividends are treated, how loans are modeled and whether riders are included in the projection.

- Guaranteed values: Typically based on minimum crediting and contract guarantees.

- Non-guaranteed values: Often assume a dividend scale or interest crediting that can change.

- Funding pattern: Shows whether planned extra payments are required to reach targets.

When comparing policies, use consistent assumptions and focus on what is contractually guaranteed, not just the best-case projection.

Costs and Fees to Understand

Whole life insurance has costs that can include mortality charges, administrative fees and commissions built into pricing. These costs are part of why cash value accumulation is usually modest in the early years.

Surrender charges may apply if you cancel the policy during the early period, which reduces the amount you receive. It is also important to understand how loans are priced and whether loan interest is fixed or variable.

- Surrender charges: Often highest in early years and decline over time.

- Loan interest: Impacts net cost of borrowing and long-term policy stability.

- Opportunity cost: Higher premiums can limit other savings or debt payoff priorities.

Knowing these cost drivers helps set realistic expectations and reduces the chance of buying a policy that does not match your cash flow.

Who Whole Life Insurance May Fit Best?

Whole life insurance is often considered when someone needs permanent coverage, values guarantees and can comfortably afford the premium long term. It may also be used for legacy planning, estate liquidity, or funding needs that benefit from predictable death benefit protection.

It may be less suitable when the budget is tight, the need is temporary, or the goal is maximizing short-term cash accumulation. A strong fit usually involves a long time horizon and a clear reason to keep the policy for decades.

- Lifelong dependents: Ongoing support needs can call for permanent protection.

- Estate planning goals: Liquidity for taxes or equalizing inheritances can be a driver.

- Stability preference: Some people prioritize guaranteed premiums and guaranteed death benefit.

Matching the policy design to the specific goal is more important than picking the largest death benefit possible.

How to Evaluate a Whole Life Policy Before Buying?

A good evaluation focuses on insurer strength, guarantees, costs and your ability to keep paying premiums. It also requires clarity about whether you want participating whole life with dividends or a non-participating structure with different guarantees.

- Define the primary purpose. Decide whether the priority is permanent protection, cash value access, or predictable legacy planning.

- Confirm affordability under stress. Ensure the premium remains manageable even if income changes or expenses rise.

- Review guaranteed values first. Look at guaranteed cash value and guaranteed death benefit before considering non-guaranteed projections.

- Compare loan and surrender terms. Understand how loans work, what they cost and how surrender charges affect early exits.

- Assess insurer financial strength. Strong capitalization and consistent policyholder treatment can matter over decades.

Once those checkpoints are clear, it becomes easier to compare policy designs and decide whether optional riders add real value.

Conclusion

Whole life insurance works by combining lifelong coverage with a cash value feature that grows inside the policy under defined rules. The tradeoff is higher premiums in exchange for permanence, guarantees and potential flexibility through loans and dividends.

The best decisions come from understanding guaranteed values, ongoing costs and the long-term commitment required. When the purpose is clear and the policy is affordable for the long haul, whole life can be a stable foundation for protection planning.