Term life insurance is designed to replace lost income for a set period, usually while other people rely on your earnings. The right amount should cover essentials without forcing you into premiums that strain your budget.

Choosing too little can leave survivors juggling rent, loans and education costs. Choosing too much can mean paying for protection you do not need, which can crowd out other priorities like emergency savings.

What Term Life Insurance is Built to Cover?

Term coverage works best when it matches financial responsibilities that have a clear time horizon. That often includes income replacement during working years, debts that must be repaid and major family goals.

It can also act as a safety net for household services that would otherwise require paid help. Childcare, transportation and caregiving costs can rise quickly when a parent or partner is no longer there.

- Income replacement: Helps maintain housing, food, utilities and day to day spending.

- Debt payoff: Reduces the risk of surviving family members needing to sell assets to cover loans.

- Education funding: Supports school, training, or college plans that are important to the household.

- Final expenses: Covers funeral costs and related medical or legal bills.

- Caregiving and services: Helps pay for childcare, elder care, or home support.

Once you know what you want the policy to do, you can translate those goals into a dollar amount with fewer surprises.

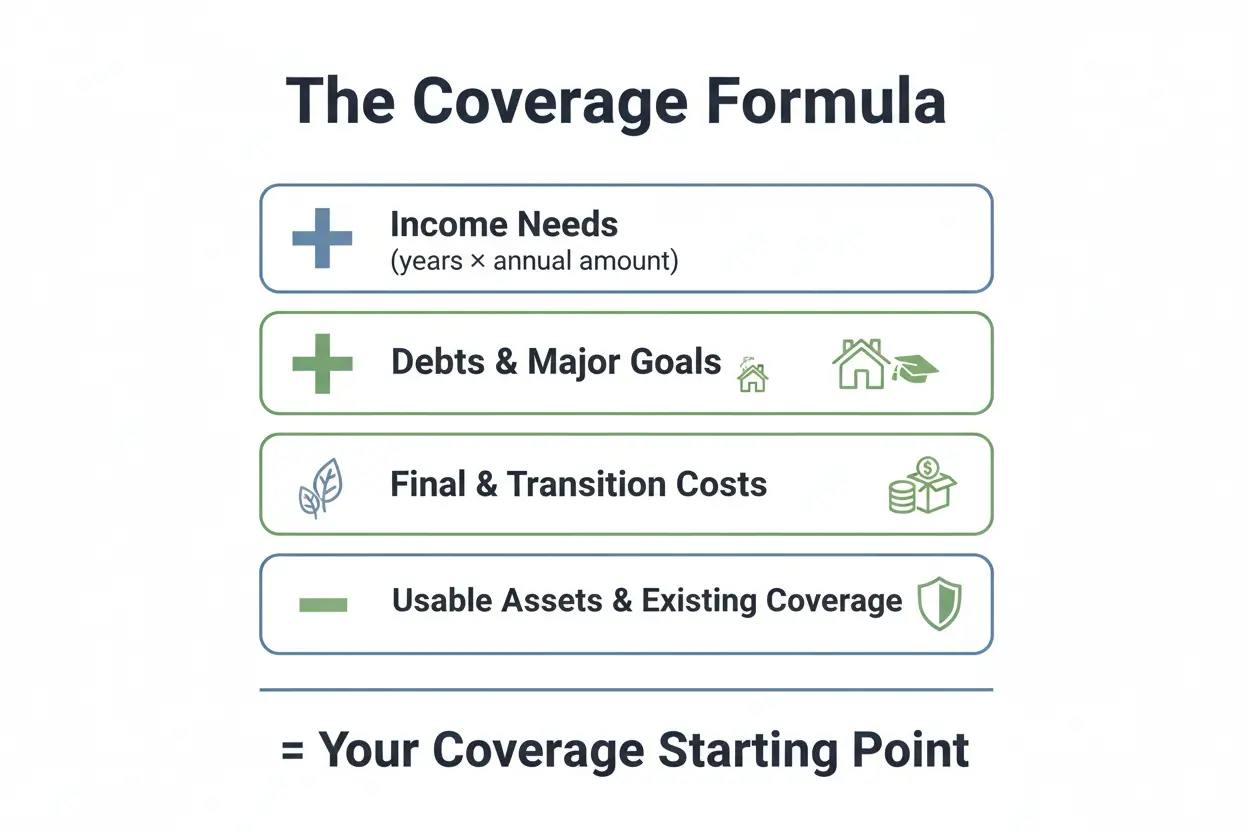

Start With a Simple Coverage Formula

A practical way to estimate a term life insurance amount is to add major costs and subtract liquid assets that are meant to support survivors. This approach keeps the focus on what your family would actually need.

Use a calculator mindset rather than a guess. The goal is a coverage range you can refine after looking at your budget and health rating.

- Add income needs. Estimate how much annual income your household would need and how many years it should last.

- Add debts and big goals. Include mortgage balance, student loans, car loans, credit cards and education targets.

- Add final and transition costs. Include funeral expenses, medical bills and a buffer for legal or moving costs.

- Subtract usable assets. Count savings, brokerage funds and existing life coverage that would be available to beneficiaries.

This produces a starting number that is grounded in your real obligations and resources.

Income Replacement Without Overbuying

Income replacement is usually the largest part of a term life insurance need. A clean method is to focus on the portion of income that your household would truly miss, not every dollar of gross pay.

Consider taxes, work expenses and savings you would no longer contribute if you were not working. Many families aim to replace enough to cover core bills and maintain stability, then revisit as goals change.

Also consider whether the surviving partner would return to work or increase hours and how quickly that could happen. A short runway of cash can matter more than a large long term number if job transitions are likely.

Debts and Major Goals That Often Drive the Total

Debts can create pressure at the worst possible time. Clearing them with a death benefit can allow survivors to keep the home and avoid high interest balances.

Not all debts need to be covered the same way. Prioritize liabilities that threaten housing or carry high interest, then decide whether you want to pay off the rest or simply reduce them.

- Mortgage and rent stability: Paying down a mortgage can reduce required income replacement.

- Student loans: Some private loans may not be discharged at death, so check the terms.

- Credit cards: These can grow fast and are often a smart target for payoff.

- Childcare and schooling: These expenses can last for years and may rise with inflation.

Once you list these items, it becomes easier to decide whether you need a larger policy or a longer term length.

Assets and Existing Coverage to Count Carefully

Subtracting assets is where many estimates go wrong. Only subtract money that is likely to be available and intended to support survivors, not funds earmarked for retirement or a business.

Review employer provided life insurance, group policies and any individual coverage you already have. Confirm beneficiary designations, because outdated beneficiaries can undermine your plan.

Liquid assets are the most useful to survivors, but long term accounts can help too if the timeline fits. If assets are volatile, consider using a conservative portion rather than the full current market value.

Term Length Should Match Your Longest Obligation

Coverage amount and term length work together. A 10 year policy might fit a near term debt payoff plan, while a 20 or 30 year term may better match a mortgage schedule or the years until children are financially independent.

Longer terms usually cost more, but they also reduce the risk of needing a new policy later when health could change. Shorter terms can work well when your income is likely to rise and debts are expected to fall quickly.

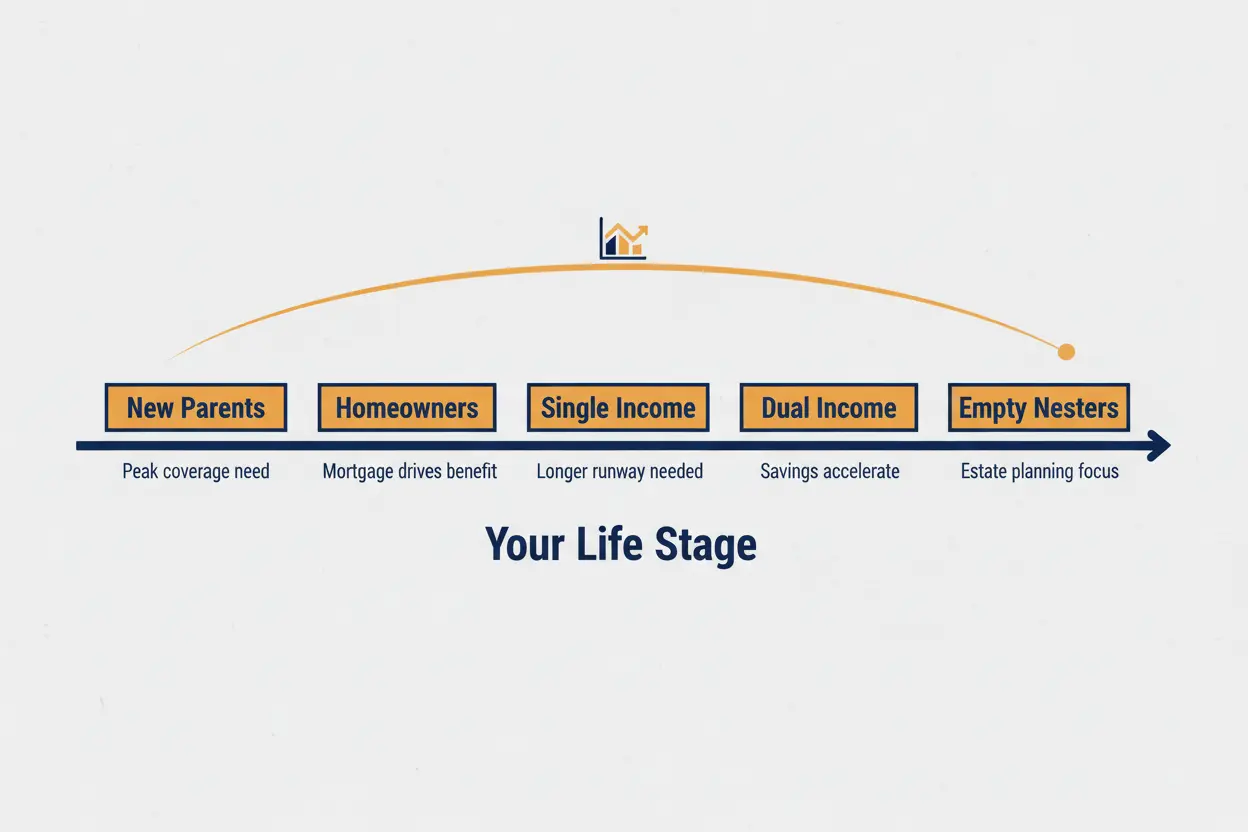

How Life Stage Changes the Target Amount?

Your term life insurance need is not static. It tends to peak when children are young, debts are high and savings are still building.

As you approach major milestones, you may be able to lower coverage or shorten the remaining years you need protection. Reviewing your estimate after major changes can keep your plan aligned with reality.

- New parents: Often need more income replacement and childcare coverage.

- Homeowners: Mortgage balance and property costs can drive the benefit size.

- Single income households: Usually need a longer runway because there is less flexibility.

- Dual income households: Still need protection, especially for childcare and debt servicing.

- Empty nesters: Coverage may shift toward final expenses and partner support.

This is also a good moment to think about whether both partners should be insured, not only the primary earner.

Stay at Home Parent Coverage is Still Real Coverage

A stay at home parent often provides childcare, scheduling, transportation and household management that would be expensive to replace. Term life insurance can fund paid support, allowing the working partner to keep earning.

Coverage is commonly based on the cost of replacement services and the time children need care. This approach keeps the estimate tied to real household operations rather than income alone.

Use a Coverage Range and Stress Test Your Budget

After you estimate a number, create a low and high range rather than choosing a single perfect figure. Your final choice should reflect premium affordability and the tradeoffs you are willing to accept.

Stress test the household budget with the premium included. A policy that lapses due to missed payments can leave your family with no protection at all.

| Cost Category | What To Include | How It Affects Coverage |

|---|---|---|

| Income Support | Core monthly bills and essentials | Drives the largest share of the benefit |

| Debt Payoff | Mortgage, loans, credit cards | Can reduce the years of income needed |

| Family Goals | Education and caregiving costs | Adds targeted dollars beyond basic living |

| Assets Offset | Savings and existing life insurance | Lowers the coverage if funds are usable |

With these categories written out, you can adjust the benefit with purpose rather than guessing.

Common Mistakes That Lead to The Wrong Number

Many people underestimate the length of time dependents will need support. Others overestimate available assets or forget that benefits should account for rising costs over time.

Another issue is relying on employer coverage alone. Group life insurance can be limited, may not follow you if you change jobs and may not be enough for a household with dependents.

- Ignoring childcare and caregiving: Replacement services can be a major hidden cost.

- Subtracting retirement money too aggressively: Those funds may not be accessible without penalties or may be needed for later years.

- Assuming debts vanish: Not all loans are discharged and survivors may still face payments.

- Buying a term that is too short: Reapplying later can be expensive if health changes.

A careful review of these pitfalls often improves your estimate more than chasing a complicated formula.

When to Recalculate Your Term Life Insurance Need?

Recalculate after major life events that change responsibilities or resources. This keeps the benefit aligned with the people and goals you are protecting.

It is also wise to review beneficiaries and ownership when you update coverage. Small paperwork issues can cause big problems later.

- Marriage or divorce: Changes who depends on your income and who should receive the benefit.

- Birth or adoption: Adds years of dependency and new education goals.

- Home purchase or refinance: Shifts the debt and the time horizon.

- Job change: Can change employer coverage, income and benefits.

- Major health change: May affect future insurability and pricing.

Regular check ins help you avoid being underinsured during your highest responsibility years.

Conclusion

The right term life insurance amount comes from matching coverage to real obligations like income needs, debts and family goals, then subtracting usable assets. A simple add and subtract method is often enough to create a clear coverage range.

Choose a term length that lines up with your longest responsibility and confirm the premium fits your budget for the long haul. When life changes, recalculate so your protection stays practical and meaningful.