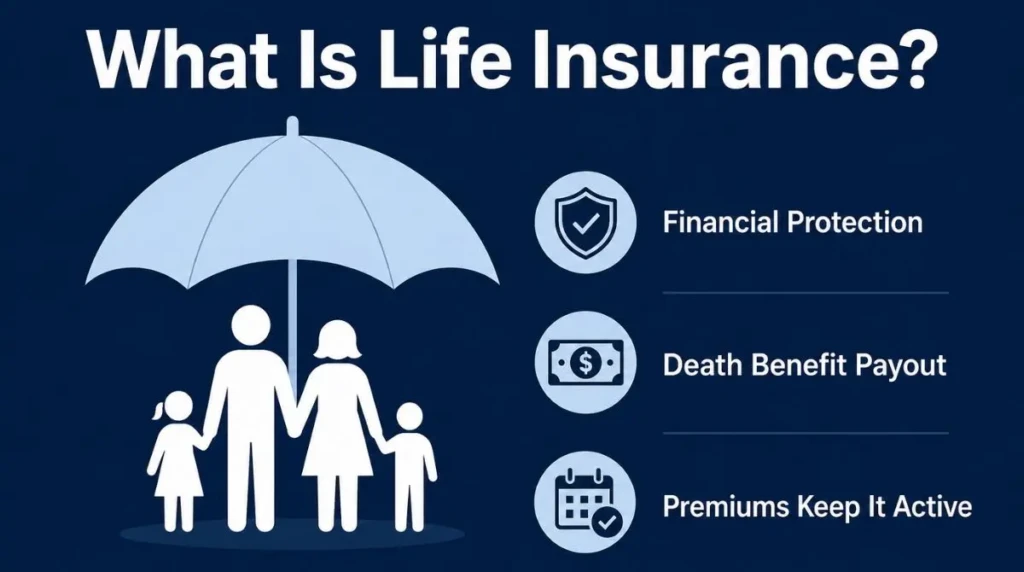

Life insurance is a contract that pays money to your chosen beneficiaries when you die. In exchange, you pay premiums to the insurance company to keep the coverage active.

The main purpose is financial protection for people who depend on your income, caregiving, or shared assets. A well chosen policy can cover everyday living costs, debts and long term plans when you are no longer there.

What is Life Insurance?

Life insurance transfers a large financial risk from your family to an insurer. You pay a predictable premium and the insurer promises a death benefit if the policy is in force when you die.

Coverage can last for a set period or for your lifetime, depending on the policy type. Some policies focus only on protection, while others also include a cash value component.

How Life Insurance Works?

When you apply, the insurer evaluates your health and risk profile to set eligibility and pricing. After approval, you pay premiums and the policy remains active as long as you keep up with required payments and terms.

If you die while coverage is active, the insurer pays the death benefit to the beneficiaries you named. Claims are typically paid as a lump sum, though some policies allow other payout options.

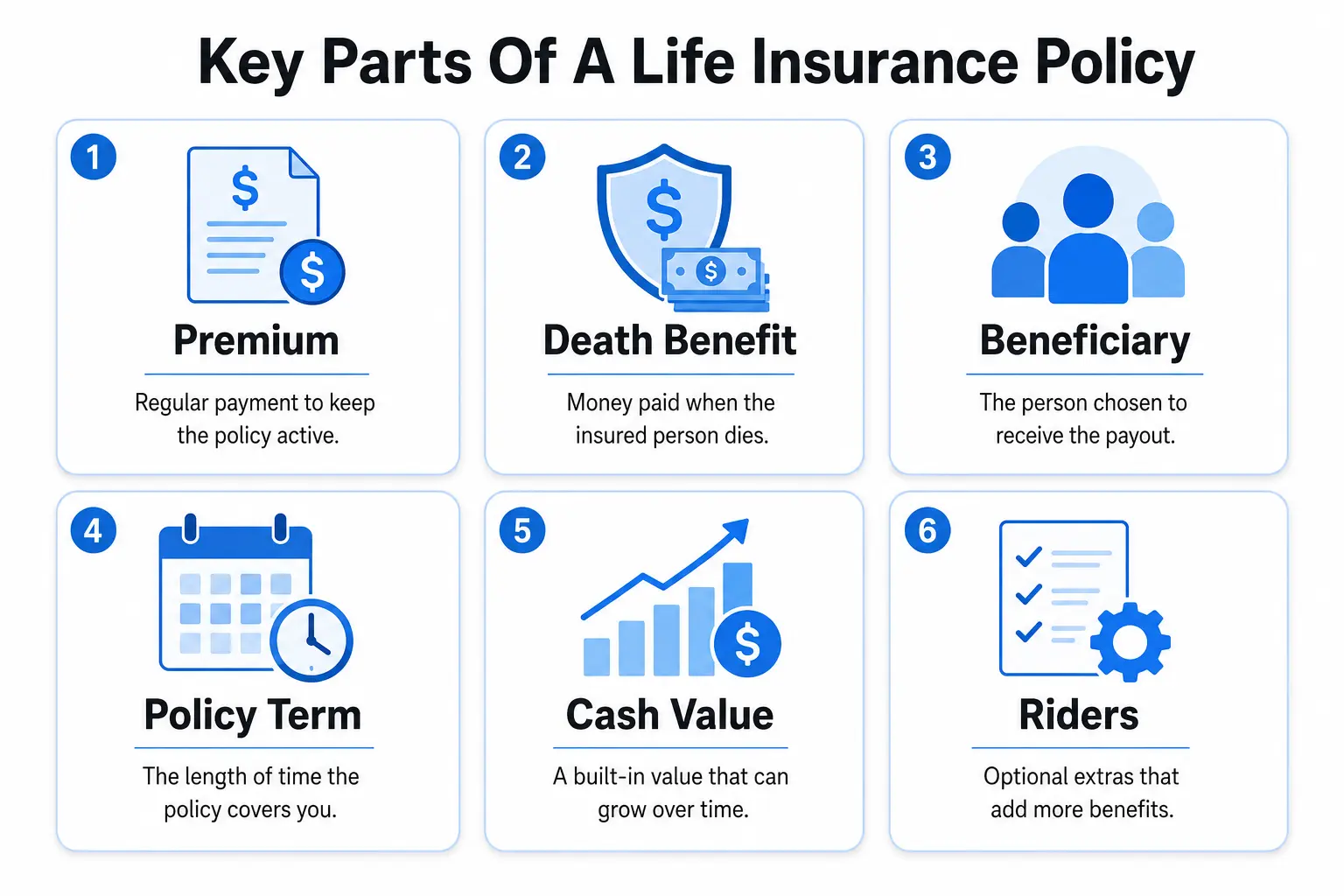

Key Parts Of A Policy

Life insurance policies use a small set of core elements. Understanding them makes it easier to compare quotes and avoid surprises later.

- Premium: The amount you pay to keep coverage in force, usually monthly or annually.

- Death Benefit: The amount paid to beneficiaries if you die while the policy is active.

- Beneficiary: The person or entity you choose to receive the payout.

- Policy Term: The length of time the coverage lasts for term policies.

- Cash Value: A savings-like balance in permanent policies that can grow over time.

- Riders: Optional add-ons that adjust coverage, benefits, or flexibility.

Once these building blocks are clear, the differences between policy types become much easier to evaluate.

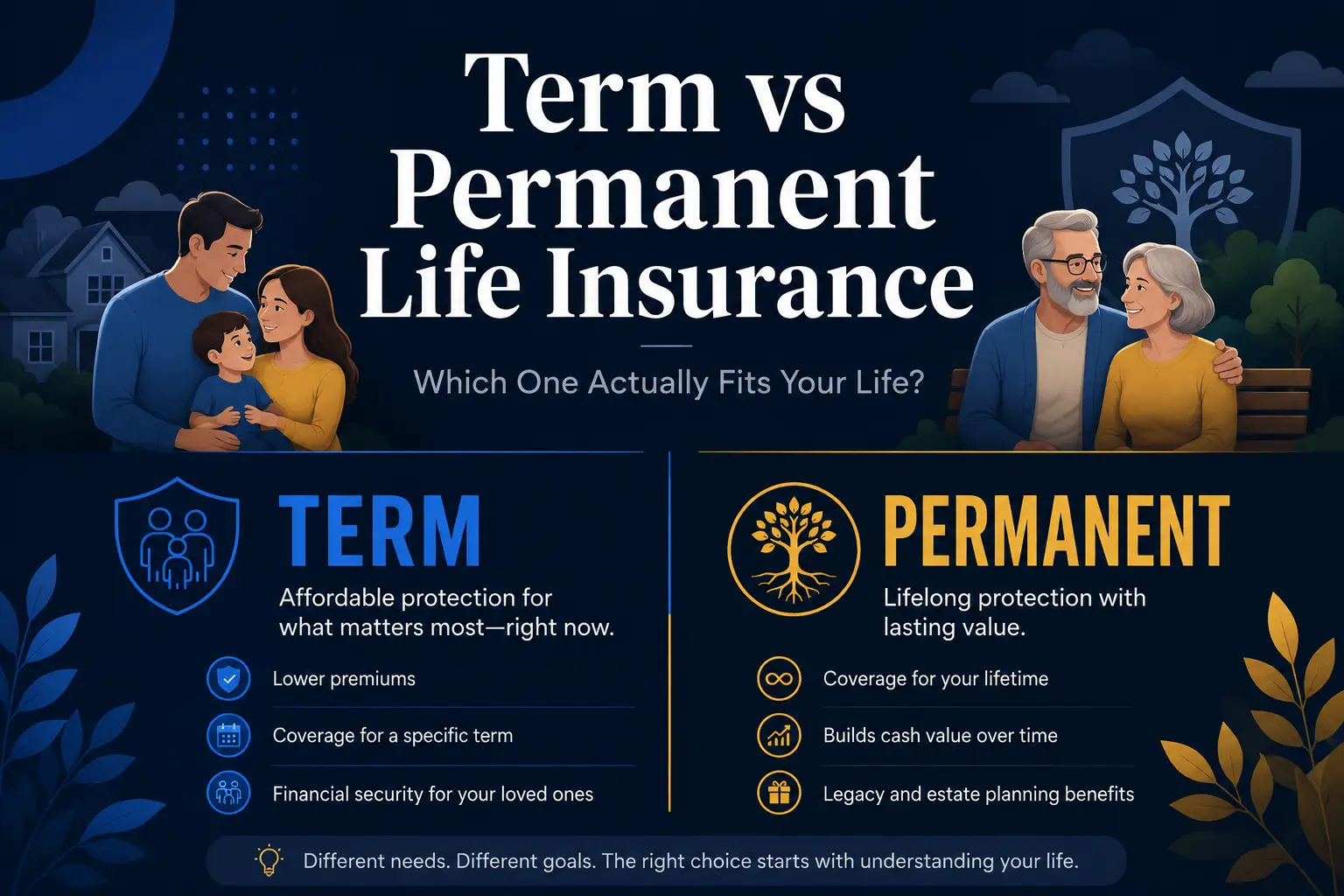

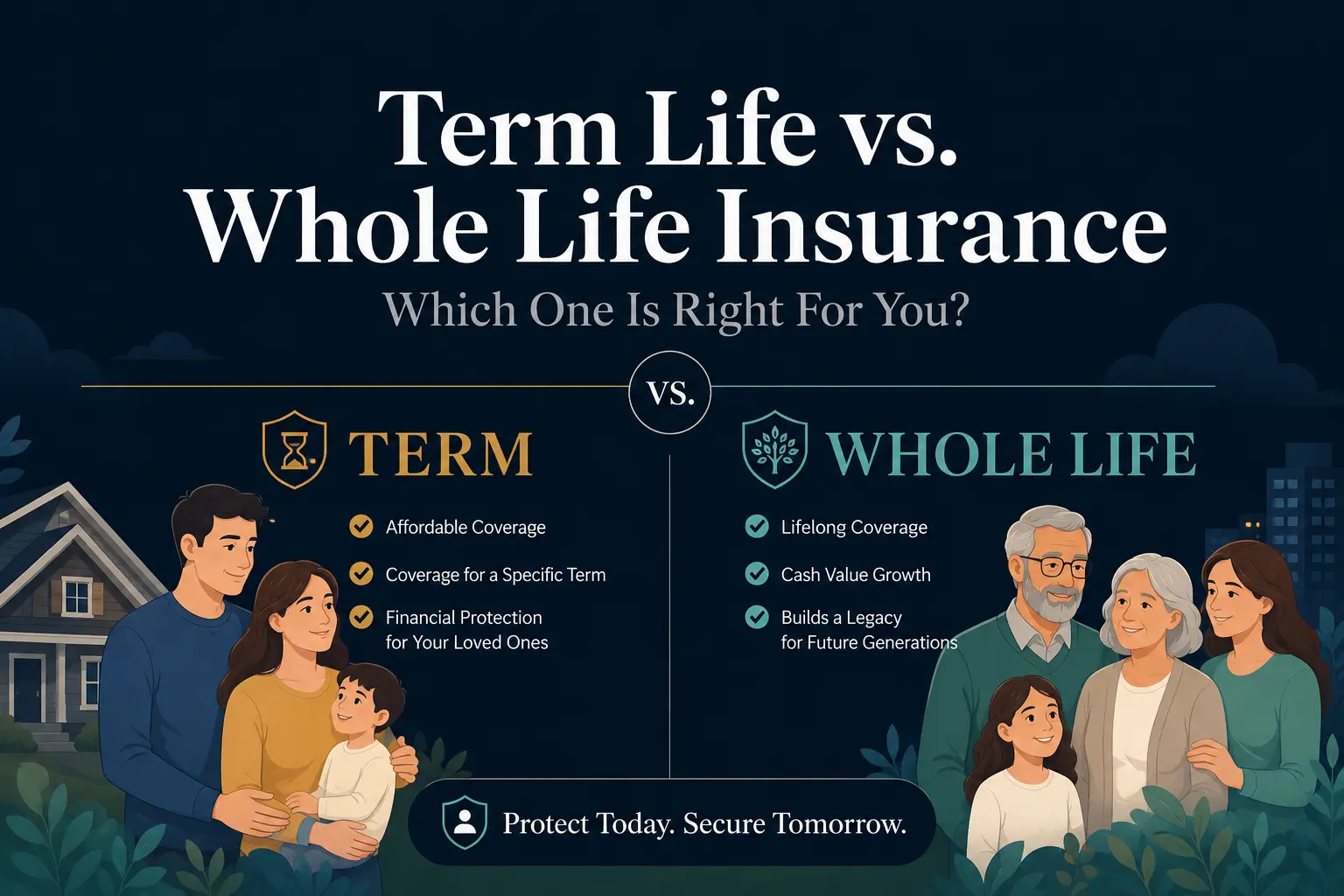

Types Of Life Insurance

The two broad categories are term life and permanent life insurance. Each is designed for different time horizons, budgets and planning goals.

Choosing between them is less about finding a perfect product and more about matching coverage length and cost to your responsibilities.

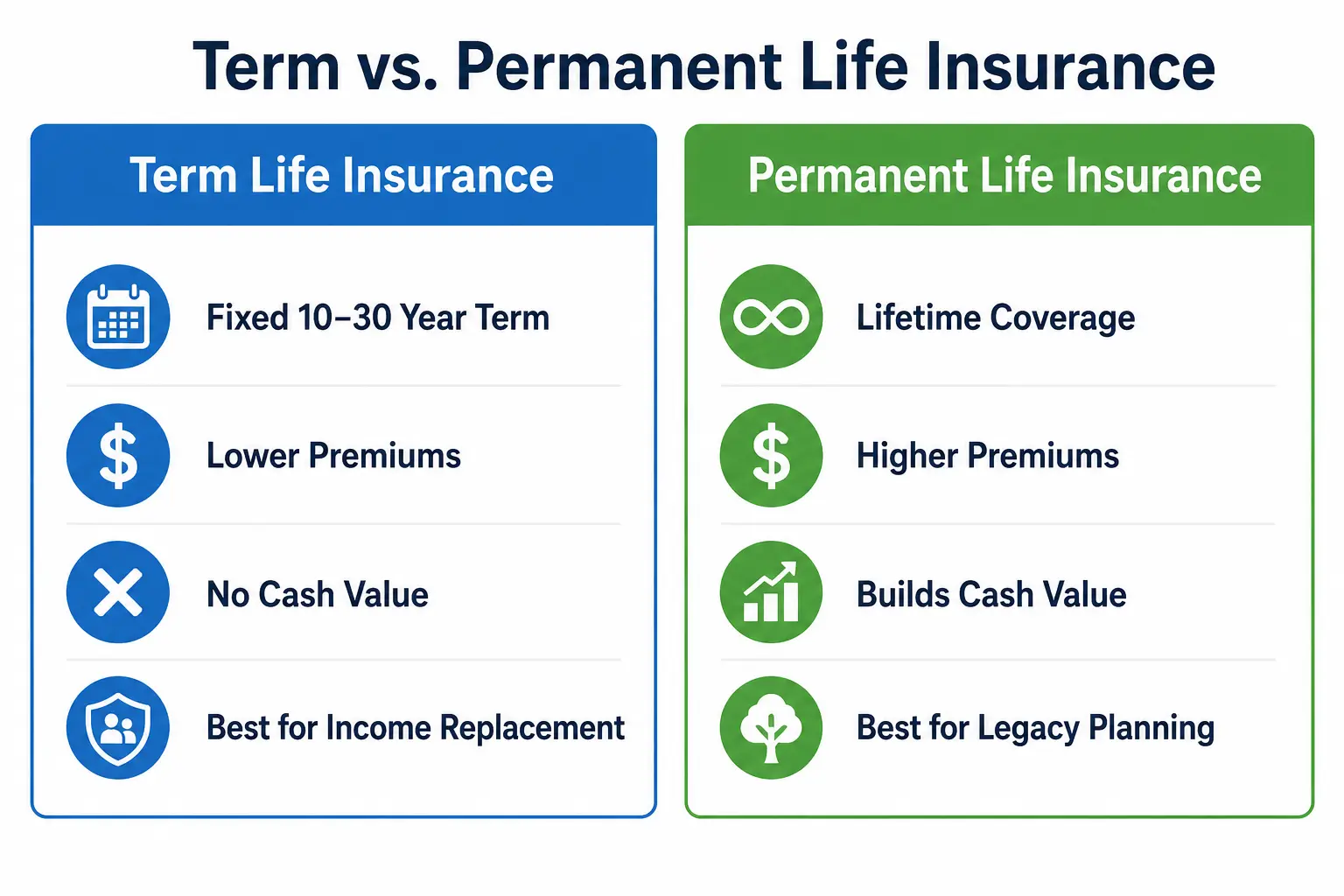

Term Life Insurance

Term life insurance provides coverage for a specific number of years, such as 10, 20, or 30. If you die during the term, the death benefit is paid and if the term ends while you are alive, coverage typically ends unless you renew or convert.

Term is often the most affordable way to buy a high death benefit. Premiums are usually level for the chosen term, then can rise if you renew.

Permanent Life Insurance

Permanent life insurance is designed to last for your lifetime as long as premiums are paid and policy conditions are met. It includes a death benefit and may build cash value over time.

Common permanent types include whole life and universal life. They can support legacy goals, estate planning needs, or long term coverage that does not expire at a set age.

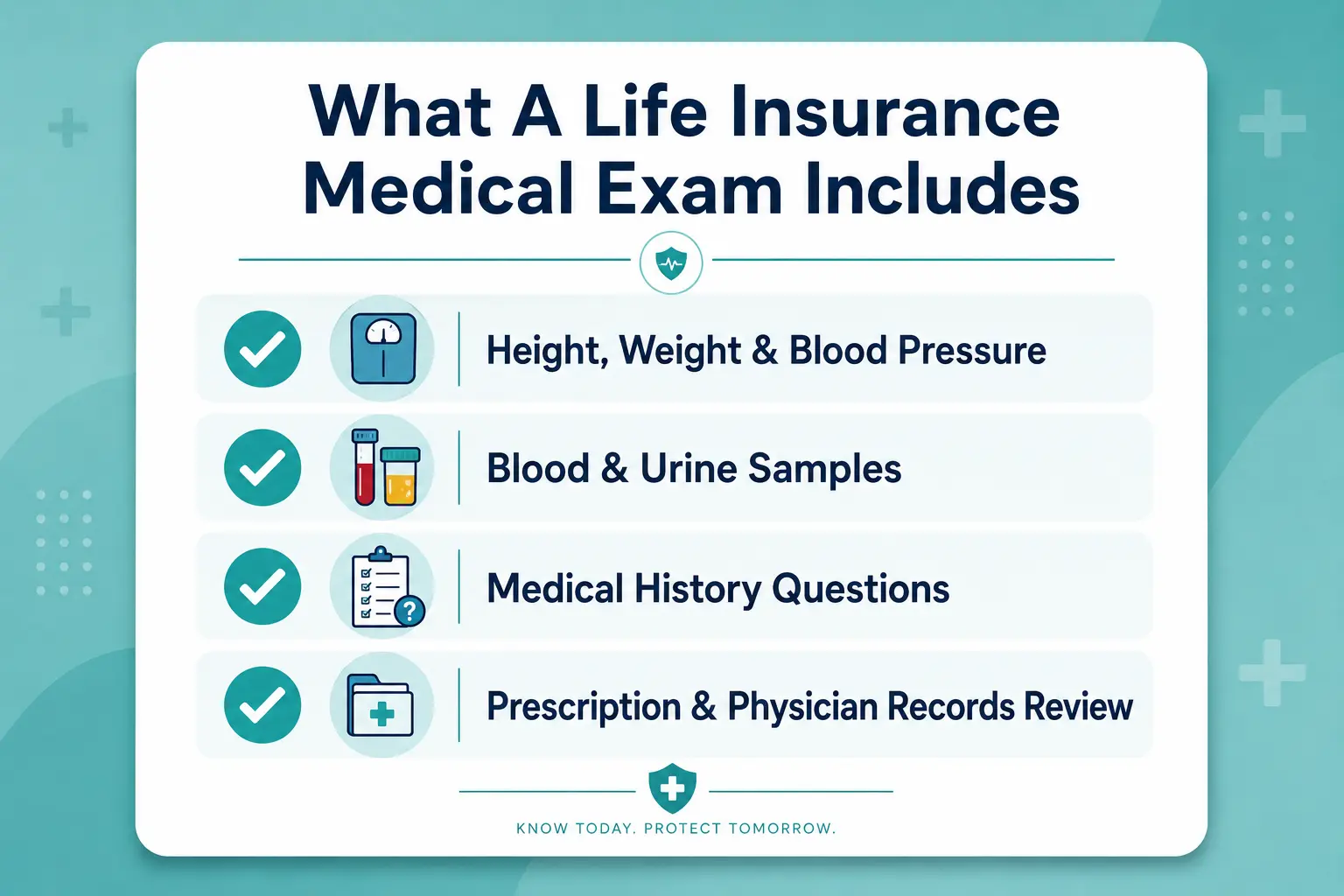

Life Insurance Underwriting And Eligibility

Underwriting is how insurers set your price based on risk. It often considers age, health history, medications, lifestyle, occupation and driving record.

Some policies require a medical exam, while others use health questions and data sources to make a decision. A more complete evaluation can lead to better pricing for lower risk applicants.

What A Medical Exam May Include?

A medical exam is usually quick and done at your home or a clinic arranged by the insurer. It helps confirm basic health indicators used in pricing.

- Height, weight and blood pressure

- Blood and urine samples

- Basic medical history questions

- Review of prescriptions and physician records when needed

Knowing what is reviewed can help you avoid delays and keep the application process smoother.

Premiums and What Affects Cost?

Life insurance premiums are based on the likelihood of a claim during the coverage period and the size of the death benefit. Insurers price policies to cover expected claims, operating costs and required reserves.

Age and health tend to be the biggest drivers, but policy type and term length matter too. Riders, tobacco use and certain hobbies can also raise the cost.

Common Pricing Factors

It helps to know what insurers weigh most heavily before you shop. This makes it easier to compare quotes on equal terms.

- Age at application and sex

- Overall health and family medical history

- Tobacco or nicotine use

- Coverage amount and policy duration

- Term life versus permanent life features

- Occupation risk and certain avocations

When you understand the cost levers, you can balance coverage needs with a premium you can sustain long term.

Choosing The Right Coverage Amount

The goal is to cover financial obligations that would be hard for your household to handle without you. That can include income replacement, debt payoff and future expenses such as education.

Also consider ongoing costs like housing, utilities, food, childcare and health insurance. A reasonable target is one that supports your dependents without overpaying for unnecessary coverage.

Needs That Policies Commonly Cover

Life insurance is often used to solve practical, time sensitive needs. A structured view of obligations helps you choose a benefit amount with fewer gaps.

- Mortgage or rent stability

- Consumer debt and loan balances

- Childcare and caregiving costs

- Education funding goals

- Final expenses and medical bills

- Business continuity for partners or key staff

After outlining needs, the next step is matching them to a policy type and duration.

Comparing Term And Permanent Policies

Term life is usually best for covering large responsibilities that decline over time, such as raising children or paying down a mortgage. Permanent life can make sense when you want coverage that does not expire and you are comfortable paying more for that feature set.

Both can be useful and some people blend them by using term for most protection and permanent for long term needs. The right choice depends on budget, timeline and whether cash value fits your plan.

| Policy Type | Coverage Length | Typical Fit |

|---|---|---|

| Term Life | Fixed term such as 10 to 30 years | Income replacement and debt coverage on a budget |

| Whole Life | Lifetime if premiums are paid | Stable coverage with predictable premiums and cash value |

| Universal Life | Lifetime with flexibility | Adjustable premiums and death benefit within policy rules |

| Final Expense | Typically lifetime with smaller benefit | Burial costs and small debts when simplified underwriting is preferred |

This overview helps narrow options, but the best fit still depends on how long your obligations last and how predictable you want payments to be.

Beneficiaries and Payout Options

Your beneficiary choices control who receives the death benefit and how quickly money can be accessed. Most policies let you name primary and contingent beneficiaries, which can reduce confusion if the primary beneficiary dies first.

Payouts are often made as a lump sum, but insurers may offer alternatives such as installments or retained asset accounts. Beneficiary designations should be reviewed after major life changes like marriage, divorce, or a new child.

Common Beneficiary Mistakes to Avoid

Beneficiary choices can override a will, so accuracy matters. Small oversights can cause delays, disputes, or unintended distributions.

- Forgetting to name a contingent beneficiary

- Not updating beneficiaries after a life event

- Naming minors directly without planning for legal control

- Using unclear labels instead of full legal names

With beneficiary details in order, it becomes easier to keep the policy aligned with your broader financial plan.

What Life Insurance Usually Covers and Excludes?

Life insurance is designed to pay for most causes of death once the policy is in force, including illness and accidents. Coverage is subject to the contract terms and some exclusions apply.

Policies commonly include a contestability period early on, where misstatements can lead to claim denial or adjustment. Suicide clauses may also apply during a limited early period, depending on the contract and local regulations.

How Claims and Payment Work?

To file a claim, beneficiaries contact the insurer and submit required documents, typically a claim form and death certificate. The insurer reviews the policy status, verifies details and then issues payment according to the chosen settlement option.

Delays are often related to missing paperwork, beneficiary disputes, or questions during the contestability window. Keeping policy documents organized and beneficiary information current can reduce friction.

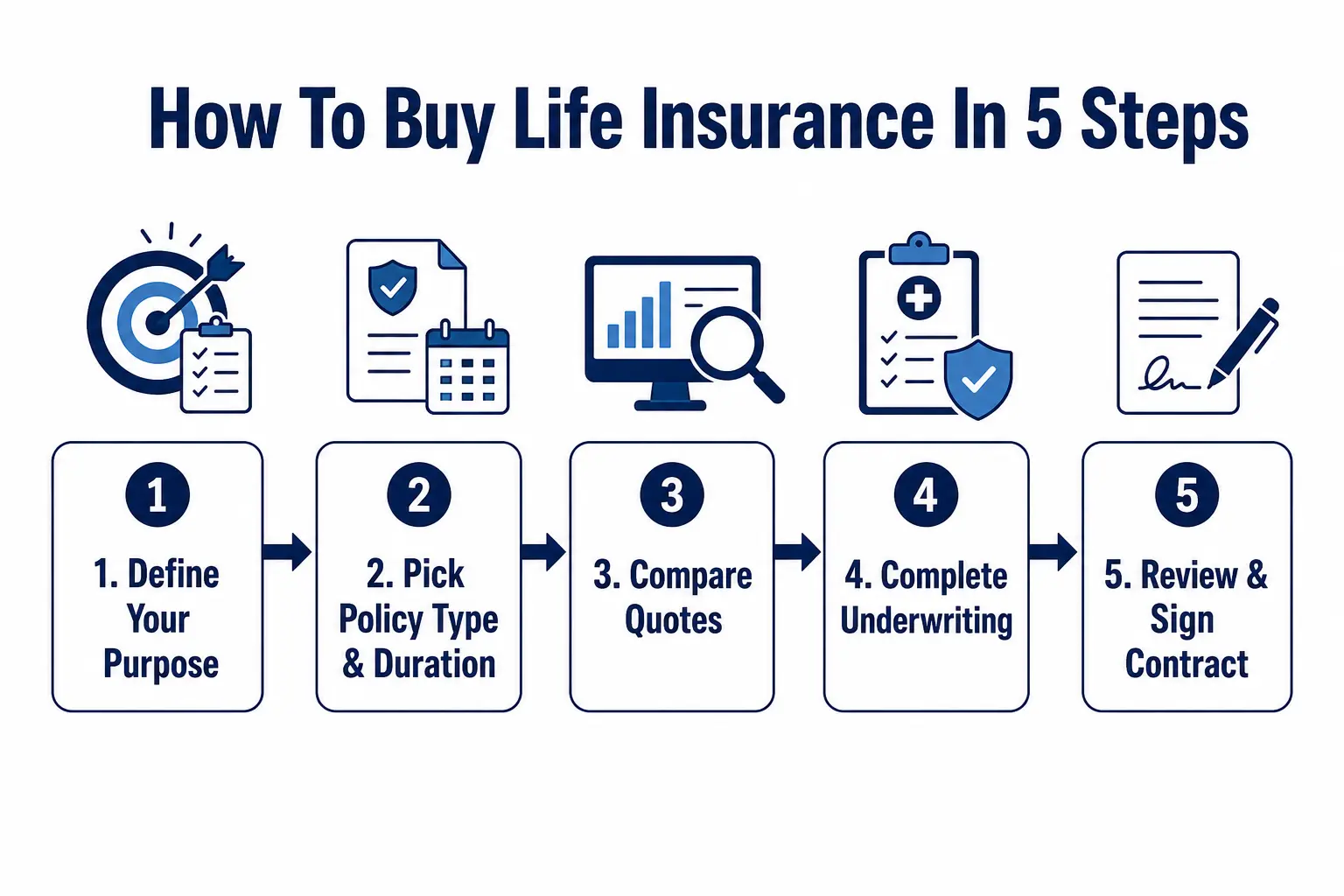

How to Buy Life Insurance?

Buying life insurance is easier when you treat it as a comparison process rather than a one time purchase. The aim is to get a policy you can keep in force without strain.

- Define the purpose. Identify what expenses and income the death benefit needs to replace or protect.

- Pick a policy type and duration. Match term length to responsibilities, or choose permanent coverage for lifelong needs.

- Compare quotes on equal terms. Keep the same death benefit, term and riders so pricing is meaningful.

- Complete underwriting accurately. Provide full health and lifestyle information to prevent claim issues later.

- Review the contract details. Confirm premium schedule, exclusions, conversion options and beneficiary designations.

After purchase, a simple maintenance routine helps ensure the policy performs as intended.

Keeping Your Policy Working Over Time

Life changes can make an older policy less effective, even if it remains active. Regular check ins help you confirm the death benefit still matches your obligations and the premium still fits your budget.

For permanent policies, monitoring cash value performance and costs is important because it can affect long term sustainability. Keep your insurer informed of address changes and store documents where beneficiaries can find them.

Conclusion

Life insurance works by exchanging steady premiums for a guaranteed financial payout to your beneficiaries if you die while the policy is active. Term life focuses on affordable protection for a set period, while permanent life insurance adds lifelong coverage and may build cash value.

The best results come from matching coverage amount and duration to real obligations, naming beneficiaries carefully and choosing premiums you can maintain. When set up well, life insurance provides clear, dependable support when it is needed most.