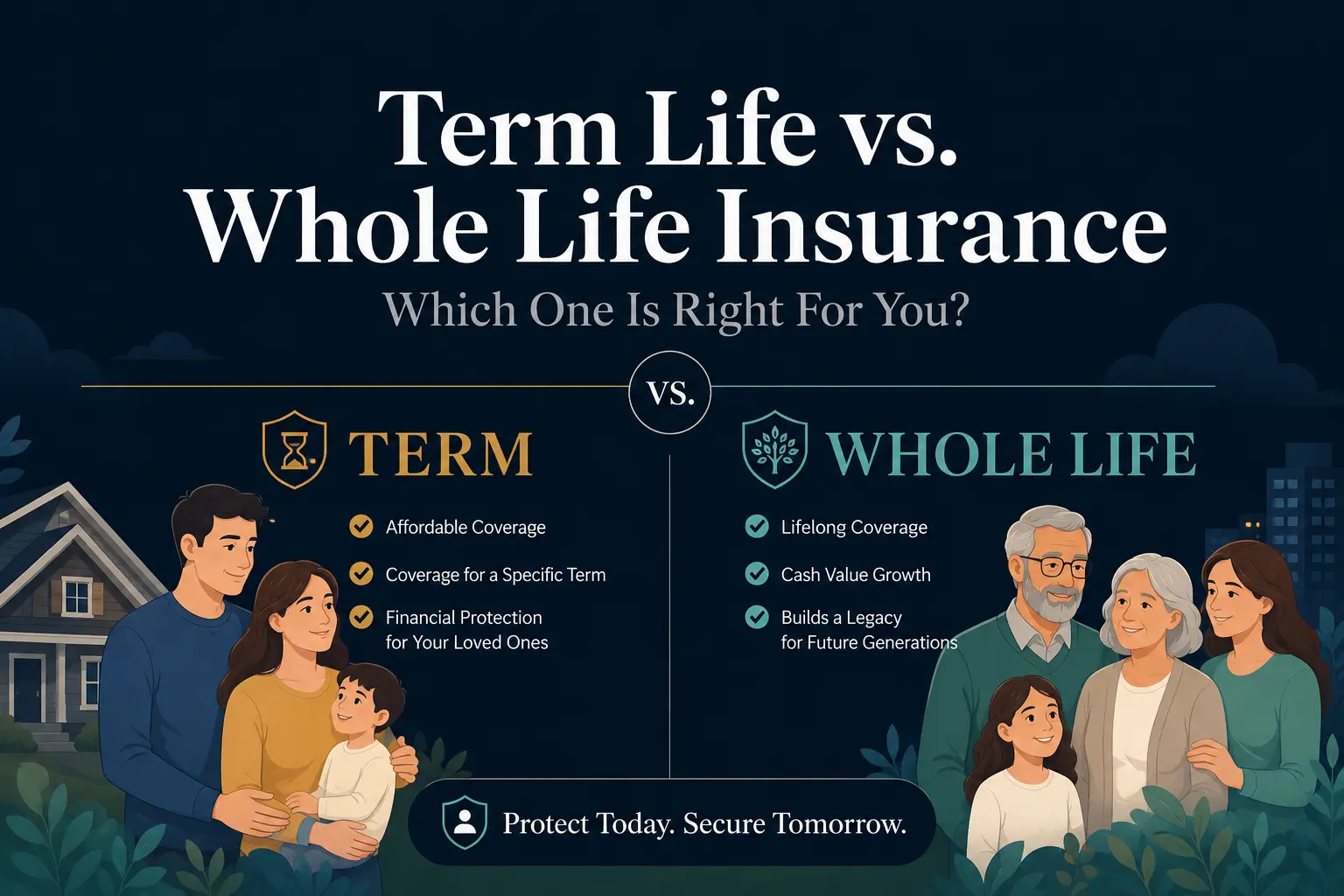

Choosing life insurance comes down to matching protection with real needs, cash flow and time horizon. The two main options are term life insurance and permanent life insurance and each works best in different situations.

This guide breaks down how they function, what they cost and how to decide without relying on hype or oversimplified rules.

What Term Life Insurance Covers?

Term life insurance provides a death benefit for a specific time period, often 10, 20, or 30 years. If the insured person dies during the term, the policy pays the benefit to the beneficiaries.

If the term ends and the policy is not renewed or converted, coverage stops. Term is built for pure protection rather than long-term accumulation.

Why People Choose Term Coverage?

Term life is designed to cover financial responsibilities that are temporary but significant. It is commonly used to protect income during working years and to cover debts that decline over time.

Many buyers prioritize term because it usually delivers the most death benefit per premium dollar, especially at younger ages and for strong health profiles.

What Permanent Life Insurance Covers?

Permanent life insurance is designed to last for life as long as premiums are paid according to the contract. It pays a death benefit whenever death occurs, not only within a limited term.

Most permanent policies also include a cash value component that can grow over time. The growth approach depends on the type of permanent policy selected.

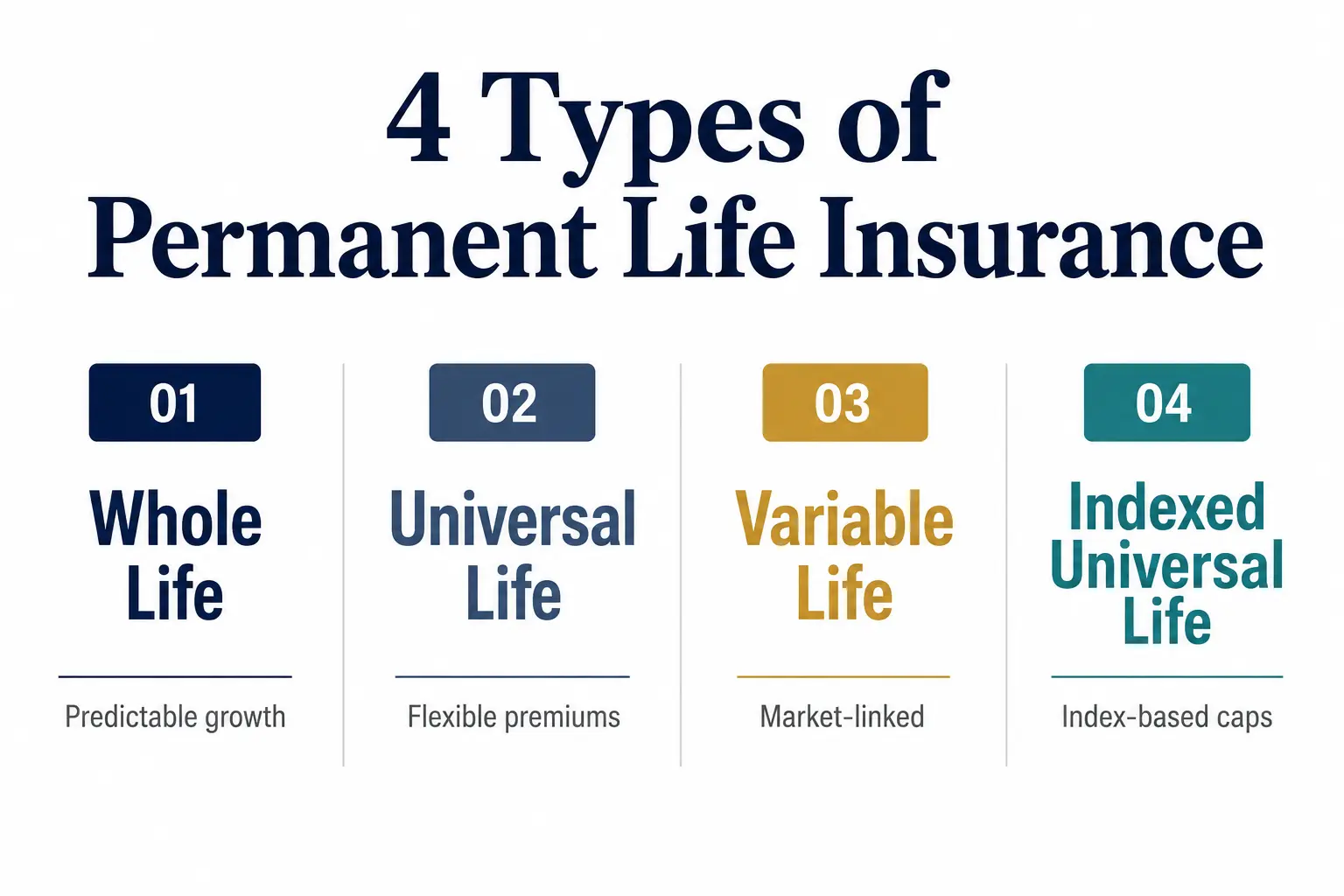

Common Types of Permanent Policies

Permanent life insurance is not a single product. It includes several structures with different cost patterns, flexibility and cash value behavior.

- Whole life insurance. Level premiums are typical and cash value growth is usually more predictable than other permanent designs.

- Universal life insurance. Offers more flexibility in premiums and death benefit structure, with cash value tied to credited interest and policy charges.

- Variable life insurance. Cash value can be invested in subaccounts, which adds market risk and potential for higher volatility.

- Indexed universal life insurance. Cash value growth is linked to an index formula with caps and participation rates, not direct market ownership.

Understanding the policy type matters because long-term performance can differ widely, even when the death benefit looks similar at purchase.

Premium Costs and Long Term Value

Term life insurance generally has lower premiums at the start because it covers a defined period and has no built-in lifetime guarantee. Premiums may rise at renewal and new medical underwriting can apply depending on the contract.

Permanent life insurance typically costs more because it combines lifelong coverage with cash value mechanics and internal fees. The higher premium can support long-term goals, but only when the policy is structured correctly and funded consistently.

How Pricing Usually Works?

Both term and permanent pricing rely heavily on age, health and the amount of coverage. Lifestyle, medical history and hobbies can also influence rates.

Policy riders, payment schedule and underwriting class can further change cost. With permanent coverage, the funding pattern and policy charges become even more important over time.

Cash Value and Policy Loans

Term life insurance does not build cash value. Your premium primarily pays for the death benefit protection and insurer expenses.

Permanent life insurance may build cash value that can be accessed through withdrawals or policy loans, subject to contract rules. Loans reduce the net death benefit if not repaid and can trigger tax issues if the policy lapses with an outstanding balance.

Cash Value is Not The Same as a Bank Account

Cash value growth can be slowed by policy charges, especially in the early years. Some products show attractive projections, but actual results depend on credited rates, investment performance and funding discipline.

Access rules vary by policy and taking money out can change long-term outcomes. Reviewing loan rates, repayment expectations and lapse risk is essential before using cash value for liquidity.

Coverage Length and Renewal Considerations

Term coverage is temporary by design. Some policies allow renewal after the initial term, but premiums commonly increase sharply with age.

Permanent coverage aims to remove renewal risk by keeping protection in force for life. That stability can be valuable for long-term obligations, estate goals, or when insurability might change later.

Conversion Options Can Add Flexibility

Many term policies offer a conversion feature that allows switching to permanent coverage without new medical underwriting, if done within a set timeframe. This can help if health changes or long-term needs become clearer.

Conversion rules are contract-specific, including deadlines and which permanent products are eligible. Confirming these details before purchase prevents surprises.

Suitability for Financial Goals

The right choice depends on what the coverage must accomplish. Some goals are time-limited, while others are permanent or tied to legacy planning.

Matching the product to the goal reduces the risk of overpaying or buying coverage that expires before it is needed.

Goals Often Served Well by Term Life Insurance

- Income replacement during peak earning years. Protects dependents until savings and career stability reduce the need.

- Mortgage or major debt protection. Aligns coverage with a payoff timeline.

- Budget-first protection. Prioritizes a high death benefit when cash flow is tight.

These are typically needs that decline over time as assets grow and obligations shrink.

Goals Often Served Well by Permanent Life Insurance

- Lifelong dependent care. Supports a beneficiary who may need ongoing financial help.

- Estate liquidity planning. Helps cover taxes, equalize inheritances, or fund bequests.

- Long horizon wealth planning. Uses stable coverage and cash value features when the policy design supports the plan.

These goals are less sensitive to a specific end date and more focused on certainty and long-term structure.

Medical Underwriting and Eligibility

Most fully underwritten policies require a health questionnaire and may include labs or an exam. Better health and younger age usually improve pricing for both term and permanent options.

Some buyers choose simplified issue or guaranteed issue coverage, but those tend to have higher costs and lower coverage limits. Reading exclusions and graded benefit provisions helps set accurate expectations.

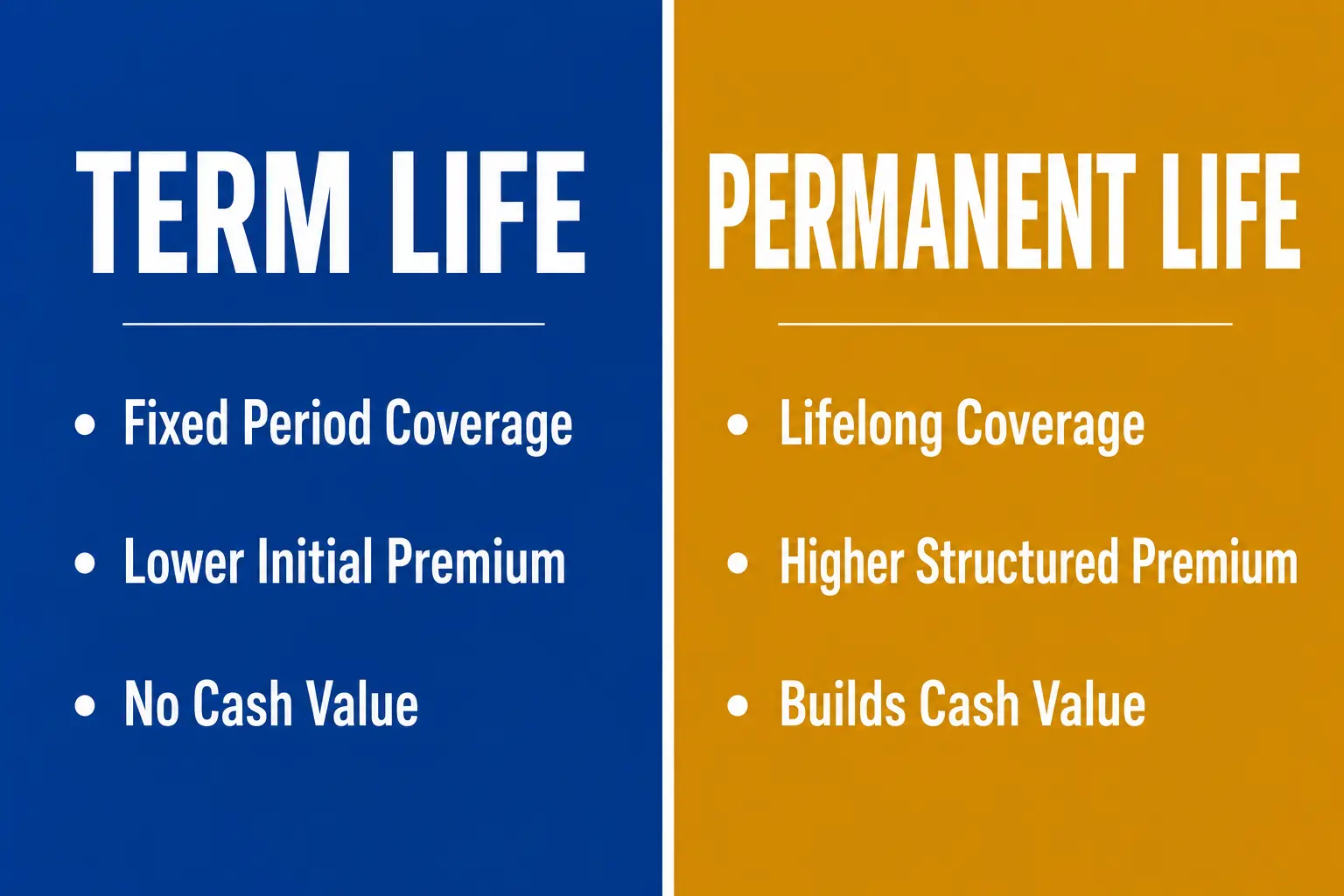

Key Differences at a Glance

A side-by-side comparison helps clarify what you are buying and what you are not buying. Use this table to anchor the decision, then evaluate details like riders and conversion rules.

| Feature | Term Life Insurance | Permanent Life Insurance |

|---|---|---|

| Coverage Length | Set period such as 10 to 30 years | Lifelong when premiums are maintained |

| Primary Purpose | Death benefit protection only | Death benefit plus potential cash value |

| Typical Premium Level | Lower initially, may rise at renewal | Higher, structured for long-term funding |

| Cash Value | No | Yes in most permanent designs |

This comparison highlights the structural differences. The best fit depends on how long the need lasts and how much certainty the plan requires.

How To Choose Between Term and Permanent?

Good decisions come from defining the purpose of coverage before shopping for a product. A clear need statement also makes quotes easier to compare across insurers.

It helps to consider coverage amount, duration and how premium payments interact with other priorities like retirement savings and emergency funds.

- Define the time horizon. Align coverage length with obligations such as dependents, debt payoff, or lifelong responsibilities.

- Estimate the death benefit need. Consider income replacement, debts, final expenses and any planned legacy or charitable giving.

- Stress test the premium. Choose a premium you can maintain through job changes, rising expenses and shifting priorities.

- Compare contract features. Review conversion options, renewal terms, riders, exclusions and how permanent policy charges work.

- Validate the long-term plan. If cash value is a goal, confirm funding level, illustrated assumptions and the impact of loans or withdrawals.

Once these inputs are clear, the product choice often becomes more obvious and less emotional.

Mistakes to Avoid When Buying Life Insurance

Life insurance can fail to deliver when the product does not match the need or when the policy design is misunderstood. Avoiding common pitfalls protects both affordability and long-term coverage.

Small details in the contract can create big differences later, especially for permanent insurance.

- Buying based on premium alone. Low cost is helpful, but weak features or short duration can leave gaps.

- Overestimating cash value growth. Permanent illustrations are not guarantees and policy charges can be significant early on.

- Ignoring conversion deadlines. Term conversion can be valuable, but only if used within the allowed window.

- Letting a permanent policy lapse. Lapse can erase coverage and can create tax complications if loans are outstanding.

A careful review up front is easier than trying to fix coverage after health changes or budgets tighten.

Conclusion

Term life insurance focuses on affordable, time-limited protection, while permanent life insurance provides lifelong coverage with potential cash value. The best choice depends on how long the need lasts, how stable premium payments will be and whether long-term guarantees matter.

Clarify the goal, compare contract details and choose coverage you can sustain. When the policy fits the purpose, life insurance becomes a straightforward tool rather than a recurring financial stress.