Life insurance gets labeled a scam when the sales pitch promises certainty, simplicity, or big gains without discussing limits. Confusion is common because policies can be complex and the buyer often cannot verify value until years later.

Another reason is mismatched expectations. If someone buys coverage that does not fit their budget, timeline, or goals, the disappointment feels like deception even when the contract is valid.

Scams also exist around the edges of the industry. Bad actors imitate insurers, pressure people into fake policies, or twist details to trigger buyer remorse.

What Life Insurance Actually is?

Life insurance is a contract where an insurer pays a benefit to beneficiaries after the insured person dies, as long as the policy terms are met. The buyer pays premiums and the insurer prices the policy using risk factors like age, health and coverage amount.

Most frustration comes from not separating insurance protection from investment claims. Protection products aim to transfer financial risk, not to deliver market-like returns.

It also helps to remember that policy language matters more than marketing. If the contract says coverage can lapse for nonpayment or has exclusions, those are enforceable terms.

Term Life Insurance Basics

Term life insurance is coverage for a set period, such as 10, 20, or 30 years. If death occurs during the term, the insurer pays the death benefit and if the term ends, coverage expires unless renewed or converted.

Term is often viewed as straightforward because the premium generally buys protection only. That simplicity is why many people find it easier to evaluate.

Term can still feel like a scam if the policy is allowed to lapse or if the buyer expects money back. Term premiums usually do not build cash value.

Whole Life and Permanent Life Insurance Basics

Whole life and other permanent policies are designed to last longer than a term period, often for life, if premiums are paid. These policies may include a cash value component that grows under policy rules.

Permanent insurance is where most confusion and accusations arise. Costs, commissions and internal charges can be hard to see and illustrations can be misunderstood as guaranteed performance.

Permanent coverage can be legitimate when it matches a long time horizon and stable cash flow. It can be a poor fit when someone needs low-cost protection or flexibility.

Common Red Flags That Make it Feel Like a Scam

Most problems come from how the policy is sold, not from the concept of insurance itself. Certain behaviors and promises should trigger caution.

- High-pressure urgency. Rushing decisions reduces the chance you will read exclusions, lapsing rules and fee disclosures.

- Guaranteed returns language. If a policy is positioned like a high-yield investment, ask where the guarantee appears in the contract.

- Vague cost explanations. If the agent cannot explain premium structure, surrender charges and ongoing policy expenses in plain language, pause.

- Replacing an existing policy quickly. Frequent replacements can reset costs and surrender periods, even when the new policy is not better.

- Missing carrier details. Legitimate coverage should clearly identify the insurer, policy number and state-specific forms.

These signals do not prove fraud, but they do raise the odds of a bad purchase. Slowing down usually improves outcomes.

Fees, Commissions and Surrender Charges

Insurance is distributed through agents and brokers and many policies pay commissions. This does not automatically make life insurance a scam, but it does create incentives that buyers should understand.

Permanent policies may include surrender charges if you cancel early. Those charges are often highest in the first years, which is why early cancellations can feel punitive.

Administrative fees, cost of insurance charges and policy riders can also affect value. Knowing where the money goes helps you compare options honestly.

What The Fine Print Usually Covers?

The contract spells out when benefits are paid and when they are not. Many disputes come from not reading provisions that are standard across the industry.

Common provisions include a contestability period, a suicide exclusion window and exclusions tied to fraud or material misrepresentation. Policies also define what counts as nonpayment and how reinstatement works.

Riders add benefits, but they also add cost and extra conditions. If a rider is included, confirm whether it is optional, how long it lasts and how claims are evaluated.

How To Evaluate Whether a Policy is Legitimate?

You can reduce risk by treating the purchase like any other major contract. Clarity matters more than sales confidence.

- Verify The Insurer. Confirm the carrier name, licensing and contact information and call the insurer to confirm the application was received.

- Match Coverage To A Real Need. Identify the financial risk you are trying to cover, such as income replacement or debt payoff.

- Request Plain-English Explanations. Ask how premiums change, what can cause lapse and what exclusions apply in your situation.

- Review All Policy Documents. Read the full policy, not only an illustration or summary and keep copies of every signed form.

- Compare Like With Like. Compare the same death benefit, term length and rider set across quotes to avoid misleading price comparisons.

This process helps separate a poor fit from true deception. It also makes it easier to spot inconsistencies before money is committed.

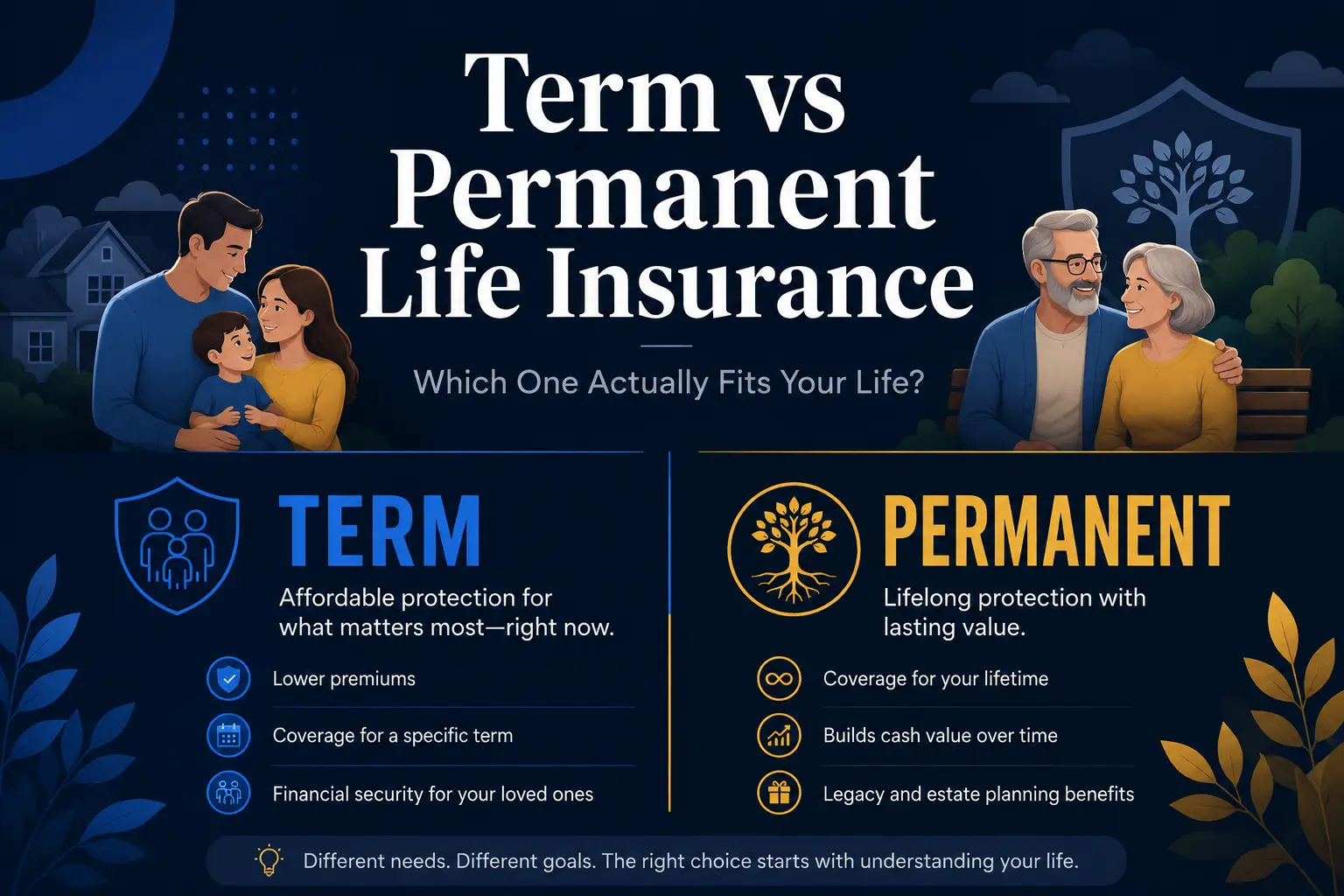

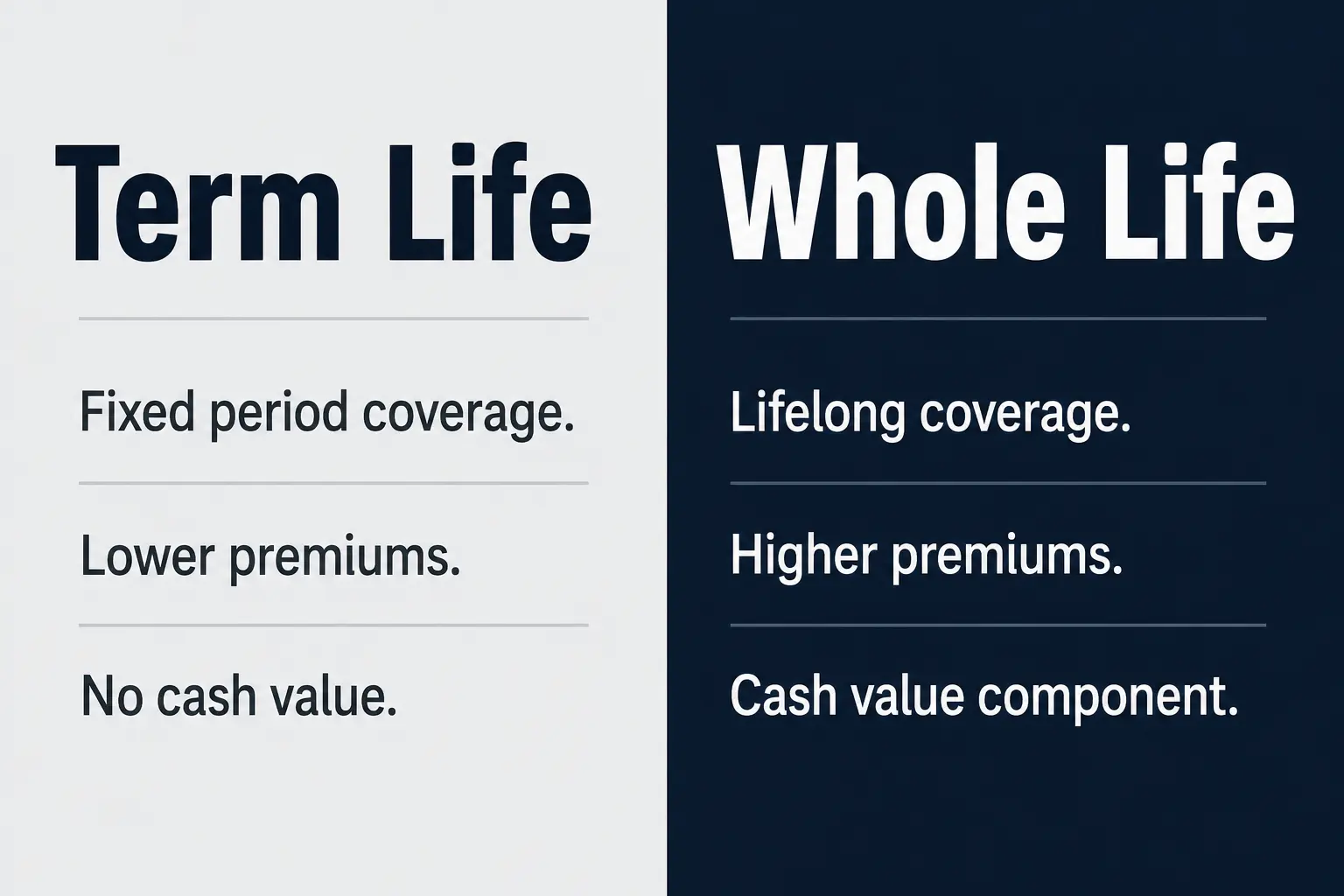

Term Vs Whole Life Quick Comparison

A simple comparison can clarify why opinions differ so sharply. People often judge the product based on a goal it was never meant to satisfy.

| Feature | Term Life Insurance | Whole Life Insurance |

|---|---|---|

| Primary Purpose | Low-cost protection for a set period | Lifelong coverage with cash value component |

| Typical Cost Pattern | Lower starting premiums | Higher premiums with internal policy charges |

| Cash Value | None in most policies | Yes, grows under policy terms |

| Early Cancellation Impact | Coverage ends, usually no payout | Possible surrender charges and reduced value |

Once you know which side of the table matches your objective, the decision becomes less emotional. The key is aligning the policy design with the job you need it to do.

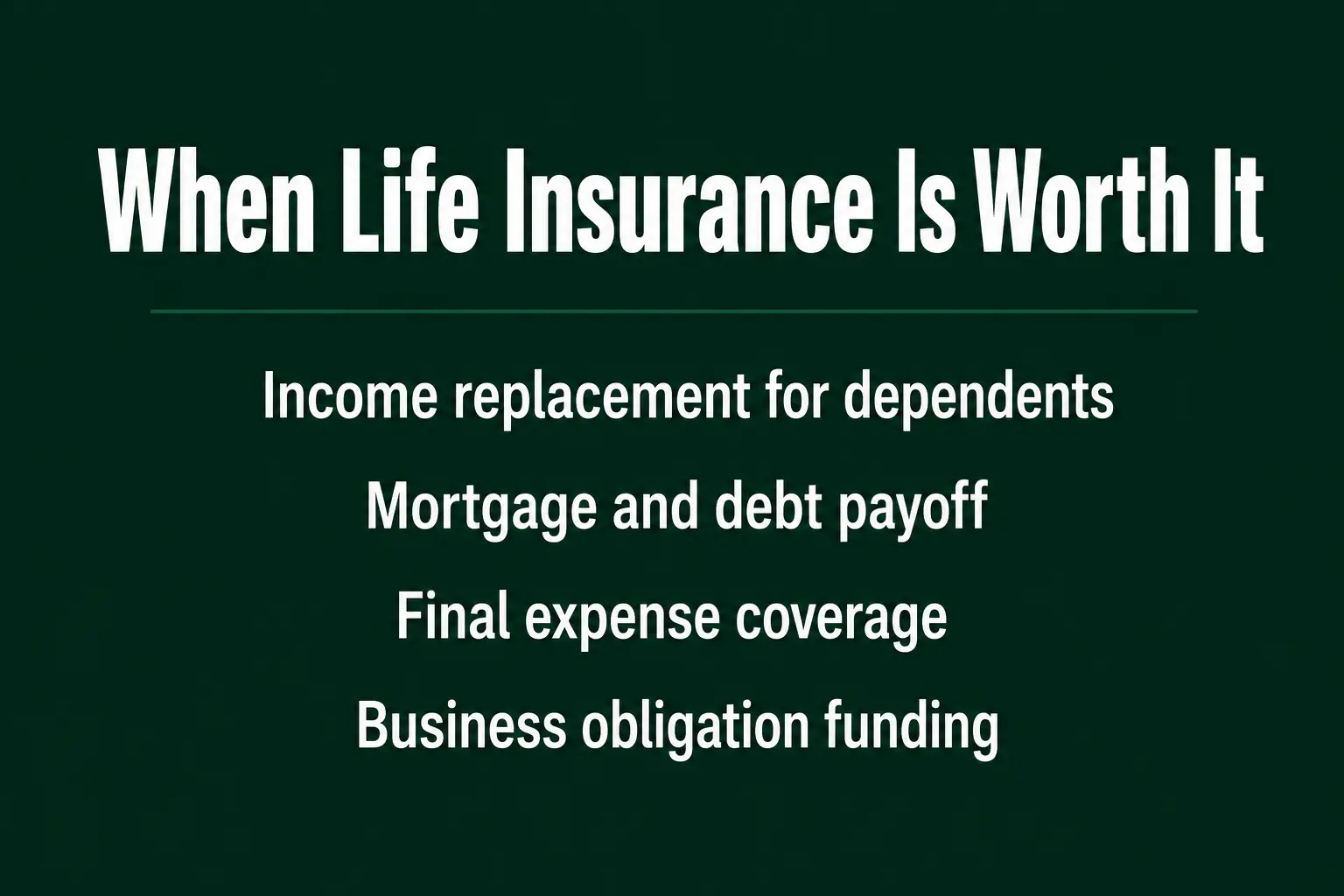

When Life Insurance Can Be Worth It?

Life insurance is most defensible when a death would create a real financial burden for others. It can also support specific planning goals that require guaranteed liquidity.

Common use cases include replacing income for dependents, paying a mortgage or other debts, covering final expenses and funding certain business obligations. These are protection problems and protection tools can be efficient when sized properly.

Permanent policies may also be used for legacy planning, special-needs support, or situations where coverage needs do not decline over time. The more stable the need and cash flow, the better the fit tends to be.

When Life Insurance Often Becomes a Bad Deal

A policy can be legitimate and still be a bad deal for a specific buyer. The most common cause is buying more complexity than the situation requires.

Permanent insurance can backfire when premiums strain the budget, causing lapse or surrender during the high-charge period. A policy that cannot be kept long term is rarely efficient.

Another issue is treating cash value projections as certain. If the buyer expects flexible access, high growth, or quick break-even, disappointment is likely unless the contract explicitly supports those expectations.

How To Buy Life Insurance Without Regret?

Buying well is mostly about clarity, patience and documentation. You do not need advanced finance knowledge to avoid the biggest traps.

- Start with the amount and term. Decide what financial obligations must be covered and for how long.

- Keep underwriting honest. Disclose medical and lifestyle details accurately to reduce claim disputes later.

- Limit riders to real value. Add-ons should solve a defined problem, not just enhance the pitch.

- Ask about lapse scenarios. Understand what happens if you miss payments or need to reduce premiums.

- Store beneficiary details carefully. Keep names and updates current to avoid delays during a claim.

These habits make the policy easier to manage across life changes. They also increase trust by putting the contract ahead of the sales narrative.

Conclusion

Life insurance is not automatically a scam, but it can feel like one when it is sold with hype, hidden tradeoffs, or the wrong expectations. The contract is real, yet the value depends on fit, time horizon and the ability to keep premiums paid.

Focus on plain terms, verified insurer details and a clear protection goal. When the policy matches a genuine need and the costs are understood upfront, life insurance can be a practical tool rather than a trap.